Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

A special thanks. Our latest book “When Markets Speak“ has been in the top #10 on Amazon over the last several weeks across most non-fiction, finance categories. We appreciate your support.

It’s that time again. In this blog, we will discuss the setup for the 2024 US elections, what the key states are to win for the candidates, and what the probabilities and polls tell us. We discuss specific stocks to play for a Trump or a Kamala win, and why the outcome of the Congressional elections is critical for your positioning in both equity styles, currencies, and fixed income. In sum, a sweep on either side, whereby the candidate also wins both chambers of Congress, would be bearish for bonds, as it means higher GDP growth and more spending. This would be bullish for cyclicals and small caps (IWM) and Emerging Markets (less tariff risk) in Trump’s case. In Kamala’s case, the market may get spooked by prospects of higher corporate taxes. Some income groups might sell stocks ahead of higher capital gains taxes as well. Equities could see a correction, which means defensives outperform.

*Special thanks to our long-time associates at ACG Analytics in Washinton, we highly recommend their fine team on the policy consulting side of the business.

Regional Banks, Pricing in De-Regulation

Our friend Stan Druckenmiller is NO Trump fan. He has NOT endorsed the former President, but he made an important point last week. When you look at a) the polls, b) the betting sites, and c) the Trump trades combined, they all are moving, quite sharply in the same direction over the last 12-14 days. Observe the Regional Banks – up +34% since mid-June vs. just +12% for the S&P 500. This sector is pricing in a significant De-regulatory regime. As you can see above, this week the KRE pierced its upper Bollinger band, which doesn’t happen very often and is a sign of real FOMO, fear of missing out.

Our friend Stan Druckenmiller is NO Trump fan. He has NOT endorsed the former President, but he made an important point last week. When you look at a) the polls, b) the betting sites, and c) the Trump trades combined, they all are moving, quite sharply in the same direction over the last 12-14 days. Observe the Regional Banks – up +34% since mid-June vs. just +12% for the S&P 500. This sector is pricing in a significant De-regulatory regime. As you can see above, this week the KRE pierced its upper Bollinger band, which doesn’t happen very often and is a sign of real FOMO, fear of missing out.

Regional Bank Strength, Lessons from the 2016 Election

Regional banks love deregulation, look at the – vertical – price action of Texas Capital Bank in 2016 around the Trump victory, and now look at TCBI’s daily relative strength, near the highest levels in a decade.

Regional banks love deregulation, look at the – vertical – price action of Texas Capital Bank in 2016 around the Trump victory, and now look at TCBI’s daily relative strength, near the highest levels in a decade.

Private Prisons

We host a conversation on the Bloomberg terminal with institutional investors. There are several portfolio managers we respect – all making the same point. “GEO ($15.20 Friday’s close) is up 100% from here in a Trump victory scenario. Our analyst says $45.” Trump has promised to be a “law and order” President. GEO equity is 30% off the Democratic National Convention lows. Markets are speaking here.

We host a conversation on the Bloomberg terminal with institutional investors. There are several portfolio managers we respect – all making the same point. “GEO ($15.20 Friday’s close) is up 100% from here in a Trump victory scenario. Our analyst says $45.” Trump has promised to be a “law and order” President. GEO equity is 30% off the Democratic National Convention lows. Markets are speaking here.

*The GEO Group, Inc. operates private correctional facilities located mostly in the United States, and other countries. The GEO Group specializes in the ownership, leasing, and management of secure facilities, processing centers, and reentry facilities and the provision of community-based services. Its worldwide operations include some 110 maximum-, medium-, and minimum-security correctional, detention (including immigrant detention), with roughly 80,000 beds. It also conducts community supervision of offenders and pretrial defendants.

“A Trump/Vance/RNC victory would clearly be more favorable for sector revenues and investment potential–but take exception to viewpoints that a Harris/Walz/DNC outcome would be nothing short of “catastrophic.” Rather, we present a framework for an asymmetric risk/reward opportunity for the group (and GEO in particular) with potential upside returns (under Trump) far in excess of probable downside risk (Harris win). ” Jones Research.

“Larry, I can say two things with certainty, 1) I don’t like Trump and have NEVER voted for him, but 2) if the race was for a fact “tight”, GEO equity would NOT be moving higher 4 out of every five days this month.“ CIO LA.

A Divided Government, Implications?

Remember, a divided government means FAR FAR, we mean FAR LESS fiscal stimulus and in Trump’s case imminent trade frictions. In Q1 this year the CBO stated the projected annual deficit would be $1.6T, now we are close to $2T. A large fiscal cliff would appear in a divided government. Over $1T of spending cuts could be forced onto the scene. The current debt ceiling EXPIRES in Q1 2025, buckle up. Over time this would be bullish for growth stocks, which tend to outperform when GDP growth is muted, and bearish for Chinese exporters. But initially, the shock of less government spending supporting the U.S. economy would likely crash the stock market. For bonds, this is a preferred scenario because it means less room to increase spending. When yields go down due to a change in domestic conditions, the dollar tends to decline as well, so gridlock is dollar-bearish.

Trump vs Kamala

Trump’s odds surpassed Kamala’s odds late last week as polling numbers tighten, and the race comes down to Michigan.

Trump’s odds surpassed Kamala’s odds late last week as polling numbers tighten, and the race comes down to Michigan.

Electoral College Map – No Tossup

The Presidential election is won in the Electoral College, and not via the popular vote. Any candidate that wins 270 or more Electoral College votes wins the election, and these votes are distributed among each of the 50 states based on the population of each state. This year, the road for both candidates to the White House seems to go through Michigan. The map here shows each state and how they will vote based on the current polling aggregate of that state. The only one that is still too close to call is Michigan, so the battle will always be in the swing states but this year primarily Michigan. Note that Trump visited Michigan last week and will be back in Michigan this weekend.

The Presidential election is won in the Electoral College, and not via the popular vote. Any candidate that wins 270 or more Electoral College votes wins the election, and these votes are distributed among each of the 50 states based on the population of each state. This year, the road for both candidates to the White House seems to go through Michigan. The map here shows each state and how they will vote based on the current polling aggregate of that state. The only one that is still too close to call is Michigan, so the battle will always be in the swing states but this year primarily Michigan. Note that Trump visited Michigan last week and will be back in Michigan this weekend.

Trump and the Curve Steepener

We must listen when markets are speaking. When Trump won the 2016 election, the spread in bond yield between the two-year and 10-year U.S. Treasury widened, or what we call “curve steepening” (see top left above). Now look at the last 3 months above, the curve is steepening again into the 2024 election. Everyone knows Trump wants to cut taxes with a $35T national debt, we believe this will frighten many global investors and push up long bond yields in the coming months if Trump wins. More treacherous, in recent years, U.S. Treasury Secretary Janet Yellen issued close to $4T of T-Bills. In our view, much of Uncle Sam’s borrowing is front-end loaded and MUST be termed out next year.

We must listen when markets are speaking. When Trump won the 2016 election, the spread in bond yield between the two-year and 10-year U.S. Treasury widened, or what we call “curve steepening” (see top left above). Now look at the last 3 months above, the curve is steepening again into the 2024 election. Everyone knows Trump wants to cut taxes with a $35T national debt, we believe this will frighten many global investors and push up long bond yields in the coming months if Trump wins. More treacherous, in recent years, U.S. Treasury Secretary Janet Yellen issued close to $4T of T-Bills. In our view, much of Uncle Sam’s borrowing is front-end loaded and MUST be termed out next year.

A Colossal Wall of Debt

From 2024-2026, close to $15.5T of U.S. debt is rolling over. In the 2024 election year Janet Yellen wanted stocks higher and markets as calm as possible. What did she do? The U.S. Treasury recklessly sold an absurd amount of T-Bills in recent years. Longer-dated bonds move FAR FAR, we mean FAR more in price than T-Bills maturing less than one year. By issuing a crazy amount of T-Bills, team Yellen was able to suck a lot of bond volatility out of the market in an election year. Anything to help Joe and Kamala. The next Treasury secretary must term out some of this debt and sell longer-dated bonds into the market. We believe this will create some HIGH drama in the first half of next year. As you can see above, the average weighted coupon on the U.S. debt load touched 2.3% this year. It’s now close to 2.6%, BUT a ton of debt is coming due and front-end rates are still very high.

From 2024-2026, close to $15.5T of U.S. debt is rolling over. In the 2024 election year Janet Yellen wanted stocks higher and markets as calm as possible. What did she do? The U.S. Treasury recklessly sold an absurd amount of T-Bills in recent years. Longer-dated bonds move FAR FAR, we mean FAR more in price than T-Bills maturing less than one year. By issuing a crazy amount of T-Bills, team Yellen was able to suck a lot of bond volatility out of the market in an election year. Anything to help Joe and Kamala. The next Treasury secretary must term out some of this debt and sell longer-dated bonds into the market. We believe this will create some HIGH drama in the first half of next year. As you can see above, the average weighted coupon on the U.S. debt load touched 2.3% this year. It’s now close to 2.6%, BUT a ton of debt is coming due and front-end rates are still very high.

The Curve — U.S. Treasuries

3-Month: 4.62%

6-Month: 4.43%

12-Month: 4.18%

2-Year: 3.94%

5-Year: 3.87%

10-Year: 4.08%

30-Year: 4.40%

*Bloomberg data, yields on U.S. Treasuries. As U.S. Treasuries mature, they will be re-sold to investors at MUCH higher bond yields. Interest on the U.S. debt load is already at $1.1T vs. $4.9T of tax receipts. HIGH ALERT — We are in a dangerous zone, interest payments as a % of tax receipts are approaching 24%. For most AAA-rated countries globally, this number is closer to 4-8%.

Gold and Silver – Reckless Deficts are the Driver

In recent client trade alerts, and well documented in our latest bestselling book – “When Markets Speak” – we have been pounding the table silver bulls. Protectionist policies coming out of both the Harris and Trump campaigns are a game changer – a whole new sustained inflation regime is upon us. It’s been more than 75 years since we had a U.S. election in which both candidates supported the aggressive use of tariffs. We have entered a whole new world. Likewise, Trump tax cuts and $2T annual deficits coming from Biden – Harris are driving capital into hard assets and Bitcoin. The 2010-2020 portfolio is history, you need a 1968-1981 portfolio construction, reach out to tatiana@thebeartrapsreport.com for more information.

In recent client trade alerts, and well documented in our latest bestselling book – “When Markets Speak” – we have been pounding the table silver bulls. Protectionist policies coming out of both the Harris and Trump campaigns are a game changer – a whole new sustained inflation regime is upon us. It’s been more than 75 years since we had a U.S. election in which both candidates supported the aggressive use of tariffs. We have entered a whole new world. Likewise, Trump tax cuts and $2T annual deficits coming from Biden – Harris are driving capital into hard assets and Bitcoin. The 2010-2020 portfolio is history, you need a 1968-1981 portfolio construction, reach out to tatiana@thebeartrapsreport.com for more information.

**We have been long silver in our high-conviction portfolio for more than three years. We normally buy and sell 1/3 of the position to take advantage of volatility, but have always stayed long silver since 2020.

Early Innings

This chart measures the relationship between the SLV Silver ETF and its 200-day moving average. We can get a feel for the state of play, how much momentum is on the field today is the question. As you can see above, the SLV is only 21% above its 200-day moving average. Past bull markets for silver reached 75%, 65%, and 33%, we are still in the early innings. We believe both Harris and Trump are silver bullish, Neither has a plan for reducing the U.S. debt trajectory. Likewise, the Fed has likely softened the path forward for political reasons. They just cut rates 50bps while their own Atlanta fed GDP now data is up at 3.4%! Throw in a fresh China stimulus plan and $2T annual deficit in Washington, and the probability of another inflation surge is high. Bullish silver.

This chart measures the relationship between the SLV Silver ETF and its 200-day moving average. We can get a feel for the state of play, how much momentum is on the field today is the question. As you can see above, the SLV is only 21% above its 200-day moving average. Past bull markets for silver reached 75%, 65%, and 33%, we are still in the early innings. We believe both Harris and Trump are silver bullish, Neither has a plan for reducing the U.S. debt trajectory. Likewise, the Fed has likely softened the path forward for political reasons. They just cut rates 50bps while their own Atlanta fed GDP now data is up at 3.4%! Throw in a fresh China stimulus plan and $2T annual deficit in Washington, and the probability of another inflation surge is high. Bullish silver.

Russell 2000, IWM and the 2016 Election

IWM shares ripped 54% higher in the months after the 2016 election. This week, the Russell 2000 reached 11% off its September 2024 lows vs. 8% for the S&P 500.

IWM shares ripped 54% higher in the months after the 2016 election. This week, the Russell 2000 reached 11% off its September 2024 lows vs. 8% for the S&P 500.

A Look at the Important States

To make things more complicated, Michigan is one of the few states whose ballot has all the candidates that are running in this election. This includes Chase Oliver (Libertarian), Randall Terry (U.S. Taxpayers), Jill Stein (Green), Robert F. Kennedy Jr. (dropped out but still on the ballot there), Joseph Kishore (Independent—Socialist Equality Party) and Cornell West. These candidates will draw votes away from the main candidates, and the question is by how much. Some say Hillary Clinton lost Michigan in 2016 because of Jill Stein.

Michigan Polls

Polling data in Michigan show a very close race, but Trump is ticking ahead of Kamala in recent polls.

Polling data in Michigan show a very close race, but Trump is ticking ahead of Kamala in recent polls.

Trump’s Advantage in the Electoral College

In the multicandidate polling, which includes Jill Stein (Green party), Kennedy (dropped out), Oliver (Libertarian) and Cornel West (Independent) Kamala leads Trump by about 2pct points. All these candidates will be on the ticket in key states such as Michigan, N. Carolina, Wisconsin, and Arizona. So the most important polls are those that include all candidates, in stead of polls that answer the question, “if left with the choice between Trump and Harris, who’d you vote for?”

In the multicandidate polling, which includes Jill Stein (Green party), Kennedy (dropped out), Oliver (Libertarian) and Cornel West (Independent) Kamala leads Trump by about 2pct points. All these candidates will be on the ticket in key states such as Michigan, N. Carolina, Wisconsin, and Arizona. So the most important polls are those that include all candidates, in stead of polls that answer the question, “if left with the choice between Trump and Harris, who’d you vote for?”

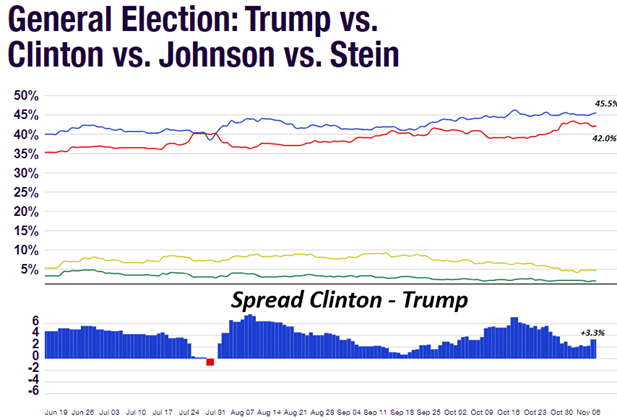

2016 Election Polls

In 2016 the final spread between Clinton and Trump was 3.3pct points. With about 136ml people voting, that 3.3pct points is 4.5ml voters, which is roughly by how much Clinton won the popular vote. It wasn’t enough for her to win the Electoral College, because most of those 4.5ml extra votes resided in New York State and California, which she has won regardless.

In 2016 the final spread between Clinton and Trump was 3.3pct points. With about 136ml people voting, that 3.3pct points is 4.5ml voters, which is roughly by how much Clinton won the popular vote. It wasn’t enough for her to win the Electoral College, because most of those 4.5ml extra votes resided in New York State and California, which she has won regardless.

2020 Election Polls

In 2020 the final spread between Biden and Trump was 7.2pct points. With 158ml voters, that translated into a lead of 11.3ml votes. Biden won the popular vote by a margin of 7ml votes, and we account the difference to polling errors. The polls here are two-way because Democrats were effective in litigating Green Party candidate Jill Stein off the ticket in most states.

In 2020 the final spread between Biden and Trump was 7.2pct points. With 158ml voters, that translated into a lead of 11.3ml votes. Biden won the popular vote by a margin of 7ml votes, and we account the difference to polling errors. The polls here are two-way because Democrats were effective in litigating Green Party candidate Jill Stein off the ticket in most states.

The point is that Bidens 7.2pct point lead in the polls was enough for him to overcome the disadvantage in the Electoral College, but for Clinton, her 3.3pct point lead was not enough. Kamala currently has a 2pct point lead over Trump in the polls, and if recent history is any guide this will not be enough for her to win the Electoral College and get into the White House. We will therefore have to follow polls and early voting data closely in the coming weeks to see if she can increase her lead enough to overcome the Electoral College disadvantage.

What are the Scenarios?

The first two scenarios are that either Trump or Harris wins with a sweep, meaning he or she wins both chambers of Congress by his or her coattails. The other two scenarios are that either one wins the presidency but with a divided Congress. The difference has significant consequences. If Kamala wins with a sweep, she will be able to raise corporate tax rates from 21% to 28% and raise the capital gains tax to 28% for the highest-income earners. She will do a partial extension of the TCJA (Tax Cuts and Jobs Act) for lower-income strata and give tax credits and subsidies for childcare, education and housing. Without a sweep, she will be unable to pass fiscal legislation through Congress, so she will stick to a partial extension of the TCJA and remove taxes on tips.

The same applies to Trump without a sweep, but in this scenario, the consequences are larger. Without Congress, Trump is limited to trade policy, which can be done outside of Congress. That means Trump will (threaten to) slap 10-20% tariffs on all imports and 60% on China and other countries that are not trading in USD. This could be a negative for China, which underperformed when Trump started his trade war at the beginning of 2018. If Trump does win the Congressional majority, he will initially focus on tax relief, and he might leave trade policy for later. This means corporate tax rates get cut to 20% or even 15% for some sectors, and a full TCJA extension, with an increase in the child tax credit. Other stimulus might come from deregulation (banks/energy) and increased spending.

In other words, a sweep on either side would be bearish for bonds, as it means higher GDP growth (either through inflation, real growth or both) and more spending. This would be bullish for cyclicals and small caps (IWM) and Emerging Markets (less tariff risk) in Trump’s case. In Kamala’s case the market may get spooked by prospects of higher corporate taxes. Some income groups might sell stocks ahead of higher capital gains taxes as well. Equities could see a correction, which means defensives outperform.

On the other hand, a divided government means no fiscal stimulus and in Trump’s case imminent trade frictions. This would be bullish for growth stocks, which tend to outperform when GDP growth is muted, and bearish for Chinese exporters. For bonds, this is a preferred scenario because it means less room to increase spending. When yields go down due to a change in domestic conditions, the dollar tends to decline as well, so gridlock is dollar-bearish.

In case Kamala wins with a sweep, it’s unclear if the higher yields on US Treasuries drives up the dollar, or if it is offset by a reduction of US exposure by international asset managers as they fear higher corporate tax rates.

¹https://taxfoundation.org/research/all/federal/kamala-harris-tax-plan-2024/

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

The Dollar Loves Trump

Despite concerns about a Trump administration trying to push down the value of the dollar vis-à-vis other currencies, Scott Bessent, a big Trump donor and on the shortlist to become Trump’s Treasury secretary should he win, emphasized that a new Trump administration would support a strong dollar. He also noted that “The reserve currency can go up and down based on the market. I believe that if you have good economic policies, you’re naturally going to have a strong dollar,”. On tariffs, Bessent said that these are “maximalist” positions likely to be softened in negotiations. He asserted, “My general view is that at the end of the day, he’s a free trader.”

Dollar Tends to Follow Trump Odds

The dollar tends to correlate with Trump’s probability of winning this year’s election.

The dollar tends to correlate with Trump’s probability of winning this year’s election.

Stocks that Benefit from a Trump or Kamala Victory

S&P Performance Around Presidential Elections

Marlin_Capital tweets: “It is not typical to see the SPX rally into Election Day when the polls are this close.

Trading activity has been very low so far this October, suggesting many are in “wait and see mode” with Q3 earnings and the election on deck.”

Although not common, we have seen markets rally into Presidential elections, both in 2004 and 1996. In both cases, markets rallied most likely because Republicans were going to hold a majority in Congress no matter who won the presidency. Also, both Kerry and Dole, the contenders for the seat in 2004 and 1996, were no threat to the markets. Today, we see that the odds for a sweep on either side are rather low, which means investors have less to worry about with the outcome of the elections.

Betting Odds for Who Will Control the Government After 2024

Odds for a sweep on either side are very low, with the Democrats likely to win control of the House and the Republicans winning control over the Senate. Without a sweep, the President is limited in the legislation he can pass, which means little room for disruptive changes that market participants dislike.

Polling Data Show Republicans Will Control Senate

Since senators are elected for 6 years, not every senate seat is up for election every four years. So, the grey states have Senate seats that are not up for election. Of the seats that are up for election, the Republicans are likely to win 13 seats, with the Democrats winning 21. This would give the Republicans 51 seats in the Senate, enough to block any legislation they don’t like. What that means is that Harris’ proposed corporate tax increase or her tax hikes for the highest income earners¹ will be blocked by a Republican majority in the Senate. This removes a lot of uncertainty and investors hate uncertainty. The high chance of a divided Congress means less uncertainty, which gives investors more confidence.

House Seats in Play

The House of Representatives is currently controlled by the Republicans but with a very slim majority of 220 vs 212 seats. There are more Republican seats in Democratic territory, and we have seen some ratings shifts towards Democrats in the last month. This is why the odds that the Democrats win the House are still slightly above even money. We do note that it is not that common for a Party to win the Presidency but not keep the House in the same election.

The House of Representatives is currently controlled by the Republicans but with a very slim majority of 220 vs 212 seats. There are more Republican seats in Democratic territory, and we have seen some ratings shifts towards Democrats in the last month. This is why the odds that the Democrats win the House are still slightly above even money. We do note that it is not that common for a Party to win the Presidency but not keep the House in the same election.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here