Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Lawrence McDonald is the New York Times Bestselling Author of “A Colossal Failure of Common Sense” – The Lehman Brothers Inside Story – one of the best-selling business books in the world, now published in 12 languages – ranked a top 20 all-time at the CFA Institute.

Economic Signposts

Classic economic bellwether – UNP is close to 9% lower in two days – this is an extremely important leading indicator.

“US railroad workers prepare for a strike as rail companies see record profits – As Biden’s recommendations fall flat, negotiations between management and unions are at an impasse – and workers are prepared to walk.” The Guardian

September 15 Update – File Under NOT Deflationary – Freight – Rail Labor “Deal” includes – a 24% wage increase over 5 years, including a 14.1% effective immediately, as well as five annual bonus payments – National Carriers Conference Committee.

*Inflation is juicing labor bargaining power, and demands.

Secular Trends – Headwinds for Equities

![]() A large bear reversal in the classic economic bellwether, UNP – major technical fail. Some would say labor threatened national strike risk is high, which is true and obvious, but the larger picture is the power of labor, back to 1960s era strength. Many equities are NOT priced for a secular change in the power of labor, indeed. This week, street research is picking up on macro crosswinds, a pending reset in the rails and trucking market, and stubbornly high labor inflation juices the risk of top-line growth and margin expansion into 2023.

A large bear reversal in the classic economic bellwether, UNP – major technical fail. Some would say labor threatened national strike risk is high, which is true and obvious, but the larger picture is the power of labor, back to 1960s era strength. Many equities are NOT priced for a secular change in the power of labor, indeed. This week, street research is picking up on macro crosswinds, a pending reset in the rails and trucking market, and stubbornly high labor inflation juices the risk of top-line growth and margin expansion into 2023.

“What makes inflation sustainable? Inflation has a traditional pattern: an exogenous shock (war, pandemic, an oil embargo, what have you); followed by the rise of the power of labor in the form of wage inflation; followed by the government mucking things up. An example of the latter, to pick one among many, is that not only are there not enough trucks and truckers but there are not enough parking spaces for the truckers to park their vehicles. Why? Because of restrictions on how close trucks can park to highways (where, naturally, there is plenty of space for them to park!).” Bear Traps Report, January 2022.

Labor Power vs. Profit Margins

Bernstein notes – “labor cost inflation for agreement workers will at best be the worst we have seen since de-regulation.” The Street is still looking for $244 (down from $258) in S&P 500 eps next year. The SPX is at 3950 ish, that´s a PE of 16.2x — a very pollyannish 2023 earnings outlook. Sure nominal earnings are helped by inflation but, real bottom line earnings get hammered in an inflation-enhanced “power of labor” world.

Bernstein notes – “labor cost inflation for agreement workers will at best be the worst we have seen since de-regulation.” The Street is still looking for $244 (down from $258) in S&P 500 eps next year. The SPX is at 3950 ish, that´s a PE of 16.2x — a very pollyannish 2023 earnings outlook. Sure nominal earnings are helped by inflation but, real bottom line earnings get hammered in an inflation-enhanced “power of labor” world.

A Look Back at Labor

While Covid is nowhere near as bad as the Black Death of the mid-14th century, precisely because the latter was more extreme, its ramifications are easier to see and learn from. In 1348 the plague crossed into England and wiped out half the population. With fewer peasants and serfs, labor was in scant supply and the peasants, and those serfs that could escape the manorial estate or had fulfilled their obligations to their lord, charged much more for their labor. Landowners’ profits plummeted. This in turn destroyed commerce in the towns, with dire financial consequences. Chaos ensued. Various laws were enacted in an attempt to hold wages to pre-plague levels. Never before had the royal government allied itself with the landowners against the workers in such an obvious and heavy handed way. This proved extremely unpopular. Nonetheless, wages continued to rise and many peasants were able to join guilds from which they had priorly been barred and learn trades, moving up the socio-economic ladder.

The off-again-on-again Hundred Years War against France heated up again and taxes were raised in 1379 and again in early 1380. The taxes were innovative, extensive, and unpopular because they were poll taxes, levied on every eligible individual regardless of rank or income. A third poll tax was instituted at the end of 1380, the most unpopular of all. Poll tax collectors interefered with life in every town and London seethed in unrest. Furthermore, political partisanship was extreme and the ruling class divided.

Finally, when investigations into failure to pay the poll tax in villages in Essex occurred at the end of May 1381, outright revolt ensued and spread like fire across the country, an uprising historians now call The Peasants’ revolt. Eventually the Tower of London was sacked and many royal officials murdered. The revolt was finally suppressed. 1,500 people were killed in the process. The population had not revovered from the plague and is estimated at 1.8 million at the time. It would be like over 300,000 US citizens being killed today.

In any event, there was a clear relationship between the plague and the ensuing power of labor and wage inflation. Furthermore, while the poll tax was thorough-going, our inflation today is more so. Geopolitical risks abound and if war ensues, inflation will take another leg up. We’ve had revolts in our own history, not to mention civil war. So a risk for civil strife exists now and over the near term. We may see more riots, and more violent ones, in the coming years.

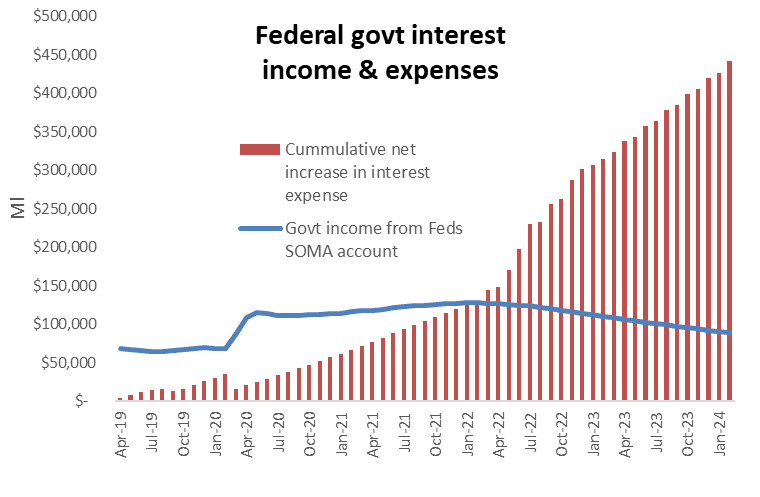

In the chart, we show how this works. The blue line shows the income from the Fed’s QE portfolio and compares it to the cumulative increase in interest expenses, from both higher interest on the government’s debt and the Fed’s payments of interest on excess reserves (IOER). This shows the $400bl negative swing next year in government income due to the deterioration in net interest income.

In the chart, we show how this works. The blue line shows the income from the Fed’s QE portfolio and compares it to the cumulative increase in interest expenses, from both higher interest on the government’s debt and the Fed’s payments of interest on excess reserves (IOER). This shows the $400bl negative swing next year in government income due to the deterioration in net interest income. We have a Federal Reserve promising to take their overnight rate to 4.5% (in March, just six months ago – the lending rate was 0.25%) and reduce this balance sheet by $1 trillion over 12 months – we were born at night, just NOT last night.

We have a Federal Reserve promising to take their overnight rate to 4.5% (in March, just six months ago – the lending rate was 0.25%) and reduce this balance sheet by $1 trillion over 12 months – we were born at night, just NOT last night.