Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Lawrence McDonald is the New York Times Bestselling Author of “A Colossal Failure of Common Sense” – The Lehman Brothers Inside Story – one of the best-selling business books in the world, now published in 12 languages – ranked a top 20 all-time at the CFA Institute.

Bear Traps Report – Opening – August 28, 2022

Italian Yields – Energy Prices Driving Political Risk

Most are focused on the U.S. Federal Reserve as the interest rate driver – global yields – gas prices – are setting up Lehman-like credit risk.

Most are focused on the U.S. Federal Reserve as the interest rate driver – global yields – gas prices – are setting up Lehman-like credit risk.

ITALY AUG INFLATION RATE RISES TO 9%; HIGHEST ON RECORD – Hundreds of billions (EUR) of energy cost liabilities are rolling up from consumers – corporations – and utilities — to sovereign credit risk across Europe.

One never forgets that smell of an Amtrak coach car at 5 am – rumbling into Manhattan. At the wise old age of 18, the bags were packed for a long journey with most of my worldly possessions in tow. Coming into New York for the first time with no parents – no siblings, was a very big day indeed. When the train stopped at Penn Station, I could hardly wait to get off. It was a feeling of heart-pounding excitement, dancing on every step. With dreams, goals, and opportunities everywhere, the only thing missing was the free lollipops and candy canes. The next thing I knew, this nice gentleman with a blue sport coat, gold cufflinks, and even a pressed handkerchief in his top right pocket approached me. “Let me help you with all that luggage, young man. If you´re hungry, the best 24-7 diner in this part of town is right over there.” Famished, I glanced over toward the restaurant. Now turned around – in a full 360, I looked down and all my bags were gone – running away with that man into a mob of humanity. Robbed right out of a scene from Trading Places, welcome to the big city. On Friday afternoon, nearly every human being on earth with capital to invest had their eyes on the Fed. It was a “look here”, “NOT over there” kind of day. Steve Jobs always said – “´it´s the scar tissue from mistakes that keeps us focused on all the pieces across the chess board – NOT just one or two.” Surprise, the biggest news by far out of “Jackson Hole” was coming out of the ECB NOT the Fed – who would have guessed? As the day moved on Friday, it was clear Don McLean´s “American Pie” was a touch longer than Jay Powell´s torpedo of a speech. Then – more and more clients we respect across our live chat on the Bloomberg terminal kept saying the same thing. The institutional – buy-side investors were all pointing to Europe as the driver of U.S. equity volatility. For most of the last 10 days, even with the much talked up “China economic slowdown” and a surge in recession certainty in Europe – global bond yields kept moving higher. In just a few weeks, Italian 10s marched from 296 to 370bps. Since Q4 2020, negative yielding bonds on the planet have plunged from $18T to almost $2T, and much of those are in Japan. Sovereign credit risk is on the rise in Europe – we have the ECB on September 8, the Fed on the 21st, and the all-important Italian elections on the 25th.

ECB Meeting September 8th into this Mess

Credit risk in Europe is near 2020 Covid Panic levels – central banks were cutting rates and handing out checks back then.

Credit risk in Europe is near 2020 Covid Panic levels – central banks were cutting rates and handing out checks back then.

The ECB has yet to pick its poison – 1) a plunge in the Euro is fueling runaway inflation in the periphery – this risk could place a right-leaning coalition in control of Italy for the first time in decades. Putin would be all smiles – from Moscow to Vladivostok – with that outcome. 2) aggressive rate hikes force more price discovery in Europe and put colossal pressure on a banking system – stuffed to the gills with sour loans. The tell – Jamie Dimon doesn´t suspend stock buybacks every day, he´s playing defense. Apple and Tesla are nearly 10% of the S&P (SPY) and 20% of the QQQs – have roughly $100B in sales coming out of the EU. On August 11th – we distributed our largest – take down risk – “high conviction” trade alert sell since February of 2020, eleven positions with new shorts on the Nasdaq. U.S. equities have been priced for an American economy on Mars or Venus, NOT Earth. Into this mess – we have a Fed that is expected to do $1T of QT over the next 12 months, NO way. Bullish hard assets > Financial assets.

Here is one of our most recent Turning Point reports – it´s a recap of our live institutional buy-side conversation on Bloomberg – an important take.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Lawrence McDonald is the New York Times Bestselling Author of “A Colossal Failure of Common Sense” – The Lehman Brothers Inside Story – one of the best-selling business books in the world, now published in 12 languages – ranked a top 20 all-time at the CFA Institute.

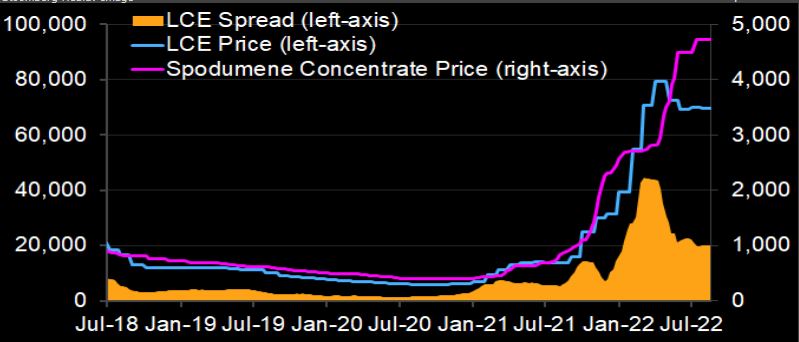

The lithium-refining spread — the price of lithium carbonate (LCE) or hydroxide minus that of spodumene concentrate — may surge through end-August. Bloomberg Intelligence notes the volume loss in lithium carbonate/hydroxide due to Sichuan’s drought-induced power crunch could amount to 12% of China’s monthly output, that´s after factoring in electricity rationing until Aug. 25. This would further tighten the market, already in severe shortage. Downstream demand among iron-phosphate and nickel-cobalt-manganese cathode makers has also been hit by power cuts, but the impact is smaller than for lithium refining. Sichuan’s lithium-hydroxide and lithium-carbonate production capacities are about 40% and 15% of China’s total. This winter, brine-based producers in West China may have to halt output as lakes freeze, adding to upward pressure on prices.

The lithium-refining spread — the price of lithium carbonate (LCE) or hydroxide minus that of spodumene concentrate — may surge through end-August. Bloomberg Intelligence notes the volume loss in lithium carbonate/hydroxide due to Sichuan’s drought-induced power crunch could amount to 12% of China’s monthly output, that´s after factoring in electricity rationing until Aug. 25. This would further tighten the market, already in severe shortage. Downstream demand among iron-phosphate and nickel-cobalt-manganese cathode makers has also been hit by power cuts, but the impact is smaller than for lithium refining. Sichuan’s lithium-hydroxide and lithium-carbonate production capacities are about 40% and 15% of China’s total. This winter, brine-based producers in West China may have to halt output as lakes freeze, adding to upward pressure on prices. We are lectured weekly – Electric vehicle sales could reach 33% globally by 2028 and 54% by 2035. Really? Mining needs to grow 30X by 2040 to meet CO2 reduction goals using solar, wind, & batteries. Lithium production needs to increase by 40X. – Oklo data.

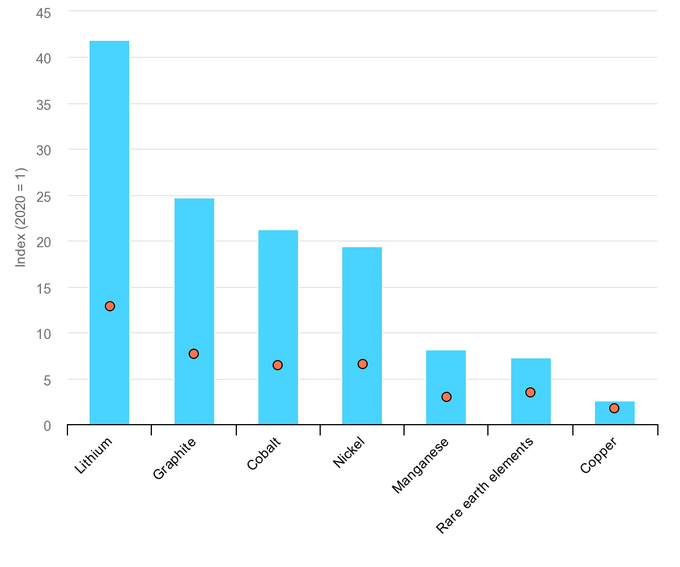

We are lectured weekly – Electric vehicle sales could reach 33% globally by 2028 and 54% by 2035. Really? Mining needs to grow 30X by 2040 to meet CO2 reduction goals using solar, wind, & batteries. Lithium production needs to increase by 40X. – Oklo data.