Saturday, May 3, 2025

Years ago, I sat down with Charlie Munger for a private lunch in Omaha; it was a priceless experience, and we’ll never forget it. It was a special day with a legend, all laid out in our latest book, When Markets Speak.

Today, our trusted Bear Traps Report associate, Chris Davis, is there.

NY Times Best Selling Author, Larry McDonald

Live From Omaha, Nebraska.

Today, HVP’s Marino Patrk and Christopher Davis attended the Berkshire-Hathaway Annual Meeting in Omaha, NE, and have been in town since Thursday. They attended conferences held by Gabelli Asset Management and Columbia Business School’s Heilbrunn Center for Graham & Dodd Investing and visited the over 20,000-square-foot exhibition of products and services that bring the sprawling conglomerate to life.

Throughout the meeting, Mr. Buffett returned to the phrase “turn every page” as an investor on the hunt for ideas and knowledge. It was not until the very last page, however, that Mr. Buffett made his big announcement—that he would advise the Board of Directors to have Mr. Greg Abel succeed him as CEO at the conclusion of this year.

At nearly 95 years of age, Buffett’s record as the greatest investor of all time stands firm. His recall of both current events and those 60-70 years ago was incredibly strong throughout the over 4 hours of question and answer. Buffett’s commonsense approach to investing, policy, and living has been a timeless draw for shareholders from all over the world. It was the late Charlie Munger who let slip a few years ago in a meeting that “Greg would preserve the culture,” and in subsequent meetings, it became more and more apparent that the leadership transition had happened without fanfare and under our noses. Buffett’s comments today also affirmed his support of Abel in that he plans to keep every share he has in the business. He qualified that it was an economic decision, “because I think the prospects of Berkshire will be better under Greg’s management than mine.” A truly breathtaking statement from the man who turned a failing New England textile mill into a trillion-dollar business, hitting all-time highs in price with Friday’s close.

Berkshire-Hathaway is a cornerstone holding across all strategies and portfolios at Hudson Value Partners. Mr. Buffett’s 60 years of stewardship have been nothing short of exceptional. Like him, we have confidence in Mr. Abel and all of Berkshire’s managers to navigate the challenges and opportunities of the decades ahead with the same discipline, ingenuity, and integrity that have benefited Berkshire-Hathaway shareholders for 6 decades.

Below we will share the top 5 ideas that came up in our conversations as a firm, at conferences, and with investors from around the world from the past few days in Omaha:

1) Berkshire may ultimately repurchase Mr. Buffett’s shares after his estate donates them to charity

- Christopher Davis first shared this idea in his post-meeting letter in May 2024. Sitting in the stands, it struck him at last year’s meeting how many times Buffett returned to how hard it is buyback large blocks of Berkshire stock and how much he likes seeing the wealth that Berkshire has created being given back to society. We believe HVP was the first (or among the first) to go public with this idea in an interview live from the NYSE on Schwab Network on September 30, 2024 (video).

- The “big buyback” is an idea now a part of the conversation and calculus for many shareholders.

2) A needle moving acquisition for Berkshire might have to be done with stock, not cash!

- While the firm has over $340 billion in cash, sellers of truly large, needle-moving businesses may not want the tax impact of selling the business for cash.

- Berkshire might be able to solve future liquidity needs for some of the largest family-owned businesses in the world like S.C. Johnson, Koch Industries, or Cargill.

- Berkshire has used stock for large acquisitions in the past like Burlington Northern Santa Fe Railroad in 2009 or the General Re acquisition in 1998.

- Stock acquisitions are more attractive if Berkshire management sees the shares as close to or above their estimate of intrinsic value.

3) Investments in the 5 Japanese Trading Houses

- Berkshire’s investments in the 5 Japanese “trading houses” Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo began in 2020.

- It was revealed in the meeting that although Buffett was the one who identified the opportunity – “turning the pages” looking at Japanese stocks – it has since been Mr. Abel leading the ongoing dialogues with the firms, and visiting with them several times a year.

- Notably, the scale of these public market investments overseen by Mr. Abel at over $23b is likely more than either Berkshire equity portfolio managers, Mr. Combs or Mr. Wechsler, currently manage individually.

- In the meeting, Mr. Abel spoke about the cultural similarities between Berkshire and the trading houses and the potential for these investments to be a springboard for joint ventures and deals around the world with each of the firms.

- They reiterated their intention for these to be investments for the next 50 years.

4) GEICO is back on track

- Mr. Combs who was originally brought on as an equity portfolio manager, has also been the CEO of GEICO since January of 2020.

- GEICO had been losing share to Progressive and others and was behind in telematics (devices that track driving behavior) and pricing.

- Today it was revealed that a revamped GEICO now has a combined ratio in the 80-90% range, which is incredible. This means that their underwriting profits are over 10%, when very good insurance operation may only have a 5% profit.

- Combs also overhauled the technology of the firm and Mr. Jain believes they are leaders or peers in the industry with the best of telematics and pricing.

- Surprisingly, Mr. Jain reported “tens of thousands” of jobs were cut at GEICO in the overhaul.

- That could very well be a taste of the changes to come within broader Berkshire as they seek continuous improvement under the leadership of a new generation.

5) Utilities are tougher places to be

- Just like Mr. Buffett confessed the sin of that one time they paid a 10-cent dividend in 1967 in this year’s letter, he also admitted the biggest mistake in the PacifiCorp acquisition was not to break up the west coast utility into companies divided by state to ring fence the liabilities.

- They admit the legal and governmental environment in some states is trying to make utilities the “insurer of last resort” in the case of wildfires has lowered the value of these businesses substantially.

- They do, however, still believe that Berkshire-Hathaway Energy will be able to deploy meaningful amounts of capital to earn regulated rates of return, especially with greater power demand needs and an aging grid.

- Mr. Buffett made a plea for more federal coordination of electric grid policy and planning amid the patchwork of 50 states of regulations, plans, and differing environmental targets.

- This reaffirms our view at HVP that utilities (beyond those owned inside our Berkshire holdings) are best viewed through our special situations framework.

Stay tuned for our takes from the Markel Shareholders Brunch on May 4th and we will also be sharing our list of the best 2025 meeting quotes from Mr. Buffett and Mr. Abel in the coming days as well.

Prior to the meeting, InvestmentNews’ Gregg Greenberg checked in with HVP for our thoughts. You can read the comments in that article here.

Important Disclosure Information

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Hudson Value Partners, LLC (“HVP”), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from HVP. Neither HVP’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if HVP is engaged, or continues to be engaged, to provide investment advisory services. HVP is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the HVP’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at https://adviserinfo.sec.gov/ .

Please Remember: If you are a HVP client, please contact HVP, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your HVP account holdings correspond directly to any comparative indices or categories.

Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your HVP accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Spending for 2025 is expected to exceed $2Tr by the time Biden leaves DC on January 20th.

Spending for 2025 is expected to exceed $2Tr by the time Biden leaves DC on January 20th. Ever since the Fed cut rates in September, U.S. 10-year bond yields are about 1% higher, and mortgage rates are following in lockstep. Hedge funds are selling short, betting on lower bond prices into colossal incoming bond sales from the U.S. Treasury. This is a highly unusual activity and has the fingerprints of the bond vigilantes everywhere; a revolt is in the works.

Ever since the Fed cut rates in September, U.S. 10-year bond yields are about 1% higher, and mortgage rates are following in lockstep. Hedge funds are selling short, betting on lower bond prices into colossal incoming bond sales from the U.S. Treasury. This is a highly unusual activity and has the fingerprints of the bond vigilantes everywhere; a revolt is in the works. Since September, US Yields have surged over 20% on Biden’s sugar high, while Canadian and German yields are down since then, Chinese yields have collapsed, and UK yields are only modestly above the September level.

Since September, US Yields have surged over 20% on Biden’s sugar high, while Canadian and German yields are down since then, Chinese yields have collapsed, and UK yields are only modestly above the September level. Private sector job growth has lagged government job growth significantly in the last year as the government keeps hiring people.

Private sector job growth has lagged government job growth significantly in the last year as the government keeps hiring people.

Our friend Stan Druckenmiller is NO Trump fan. He

Our friend Stan Druckenmiller is NO Trump fan. He  Regional banks love deregulation, look at the – vertical – price action of Texas Capital Bank in 2016 around the Trump victory, and now look at TCBI’s daily relative strength,

Regional banks love deregulation, look at the – vertical – price action of Texas Capital Bank in 2016 around the Trump victory, and now look at TCBI’s daily relative strength,  We host a conversation on the Bloomberg terminal with institutional investors. There are several portfolio managers we respect – all making the same point. “GEO ($15.20 Friday’s close) is up 100% from here in a Trump victory scenario. Our analyst says $45.” Trump has promised to be a “law and order” President. GEO equity is 30% off the Democratic National Convention lows.

We host a conversation on the Bloomberg terminal with institutional investors. There are several portfolio managers we respect – all making the same point. “GEO ($15.20 Friday’s close) is up 100% from here in a Trump victory scenario. Our analyst says $45.” Trump has promised to be a “law and order” President. GEO equity is 30% off the Democratic National Convention lows.  Trump’s odds surpassed Kamala’s odds late last week as polling numbers tighten, and the race comes down to Michigan.

Trump’s odds surpassed Kamala’s odds late last week as polling numbers tighten, and the race comes down to Michigan. The Presidential election is won in the Electoral College, and not via the popular vote. Any candidate that wins 270 or more Electoral College votes wins the election, and these votes are distributed among each of the 50 states based on the population of each state. This year, the road for both candidates to the White House seems to go through Michigan. The map here shows each state and how they will vote based on the current polling aggregate of that state.

The Presidential election is won in the Electoral College, and not via the popular vote. Any candidate that wins 270 or more Electoral College votes wins the election, and these votes are distributed among each of the 50 states based on the population of each state. This year, the road for both candidates to the White House seems to go through Michigan. The map here shows each state and how they will vote based on the current polling aggregate of that state.  We must listen when markets are speaking. When Trump won the 2016 election, the spread in bond yield between the two-year and 10-year U.S. Treasury widened, or what we call “curve steepening” (see top left above). Now look at the last 3 months above, the curve is steepening again into the 2024 election. Everyone knows Trump wants to cut taxes with a $35T national debt, we believe this will frighten many global investors and push up long bond yields in the coming months if Trump wins. More treacherous, in recent years, U.S. Treasury Secretary Janet Yellen issued close to $4T of T-Bills. In our view, much of Uncle Sam’s borrowing is front-end loaded and MUST be termed out next year.

We must listen when markets are speaking. When Trump won the 2016 election, the spread in bond yield between the two-year and 10-year U.S. Treasury widened, or what we call “curve steepening” (see top left above). Now look at the last 3 months above, the curve is steepening again into the 2024 election. Everyone knows Trump wants to cut taxes with a $35T national debt, we believe this will frighten many global investors and push up long bond yields in the coming months if Trump wins. More treacherous, in recent years, U.S. Treasury Secretary Janet Yellen issued close to $4T of T-Bills. In our view, much of Uncle Sam’s borrowing is front-end loaded and MUST be termed out next year. From 2024-2026, close to $15.5T of U.S. debt is rolling over. In the 2024 election year Janet Yellen wanted stocks higher and markets as calm as possible. What did she do?

From 2024-2026, close to $15.5T of U.S. debt is rolling over. In the 2024 election year Janet Yellen wanted stocks higher and markets as calm as possible. What did she do?  In recent client trade alerts, and well documented in our latest bestselling book – “

In recent client trade alerts, and well documented in our latest bestselling book – “ This chart measures the relationship between the SLV Silver ETF and its 200-day moving average. We can get a feel for the state of play, how much momentum is on the field today is the question.

This chart measures the relationship between the SLV Silver ETF and its 200-day moving average. We can get a feel for the state of play, how much momentum is on the field today is the question.  IWM shares ripped 54% higher in the months after the 2016 election. This week, the Russell 2000 reached 11% off its September 2024 lows vs. 8% for the S&P 500.

IWM shares ripped 54% higher in the months after the 2016 election. This week, the Russell 2000 reached 11% off its September 2024 lows vs. 8% for the S&P 500. Polling data in Michigan show a very close race, but Trump is ticking ahead of Kamala in recent polls.

Polling data in Michigan show a very close race, but Trump is ticking ahead of Kamala in recent polls. In the multicandidate polling, which includes Jill Stein (Green party), Kennedy (dropped out), Oliver (Libertarian) and Cornel West (Independent) Kamala leads Trump by about 2pct points. All these candidates will be on the ticket in key states such as Michigan, N. Carolina, Wisconsin, and Arizona. So the most important polls are those that include all candidates, in stead of polls that answer the question, “if left with the choice between Trump and Harris, who’d you vote for?”

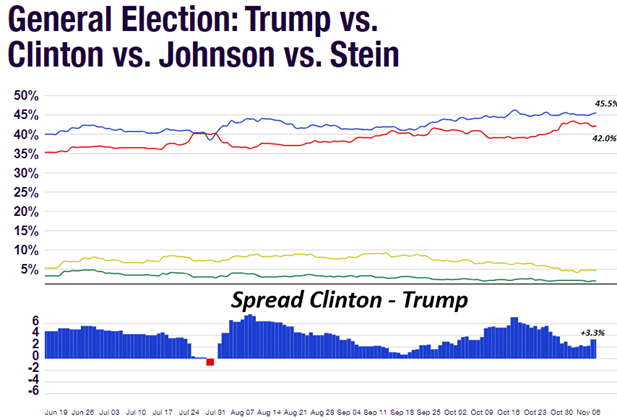

In the multicandidate polling, which includes Jill Stein (Green party), Kennedy (dropped out), Oliver (Libertarian) and Cornel West (Independent) Kamala leads Trump by about 2pct points. All these candidates will be on the ticket in key states such as Michigan, N. Carolina, Wisconsin, and Arizona. So the most important polls are those that include all candidates, in stead of polls that answer the question, “if left with the choice between Trump and Harris, who’d you vote for?” In 2016 the final spread between Clinton and Trump was 3.3pct points. With about 136ml people voting, that 3.3pct points is 4.5ml voters, which is roughly by how much Clinton won the popular vote. It wasn’t enough for her to win the Electoral College, because most of those 4.5ml extra votes resided in New York State and California, which she has won regardless.

In 2016 the final spread between Clinton and Trump was 3.3pct points. With about 136ml people voting, that 3.3pct points is 4.5ml voters, which is roughly by how much Clinton won the popular vote. It wasn’t enough for her to win the Electoral College, because most of those 4.5ml extra votes resided in New York State and California, which she has won regardless. In 2020 the final spread between Biden and Trump was 7.2pct points. With 158ml voters, that translated into a lead of 11.3ml votes. Biden won the popular vote by a margin of 7ml votes, and we account the difference to polling errors. The polls here are two-way because Democrats were effective in litigating Green Party candidate Jill Stein off the ticket in most states.

In 2020 the final spread between Biden and Trump was 7.2pct points. With 158ml voters, that translated into a lead of 11.3ml votes. Biden won the popular vote by a margin of 7ml votes, and we account the difference to polling errors. The polls here are two-way because Democrats were effective in litigating Green Party candidate Jill Stein off the ticket in most states.

The dollar tends to correlate with Trump’s probability of winning this year’s election.

The dollar tends to correlate with Trump’s probability of winning this year’s election.

The House of Representatives is currently controlled by the Republicans but with a very slim majority of 220 vs 212 seats. There are more Republican seats in Democratic territory, and we have seen some ratings shifts towards Democrats in the last month. This is why the odds that the Democrats win the House are still slightly above even money. We do note that it is not that common for a Party to win the Presidency but not keep the House in the same election.

The House of Representatives is currently controlled by the Republicans but with a very slim majority of 220 vs 212 seats. There are more Republican seats in Democratic territory, and we have seen some ratings shifts towards Democrats in the last month. This is why the odds that the Democrats win the House are still slightly above even money. We do note that it is not that common for a Party to win the Presidency but not keep the House in the same election. It’s been a tough week for cryptos so far. On-chain data by Glassnode reveals a huge dip in the number of Bitcoin held by OTC desks, showing that over 1,000 BTC (worth over $60 million) have left their addresses since Aug. 27 and moved to exchanges. The data accompanies reports of whales transferring some $141ml of Bitcoin to exchanges. Moves from OTC to exchanges suggests these big holders are selling the bitcoins they are transferring.

It’s been a tough week for cryptos so far. On-chain data by Glassnode reveals a huge dip in the number of Bitcoin held by OTC desks, showing that over 1,000 BTC (worth over $60 million) have left their addresses since Aug. 27 and moved to exchanges. The data accompanies reports of whales transferring some $141ml of Bitcoin to exchanges. Moves from OTC to exchanges suggests these big holders are selling the bitcoins they are transferring.

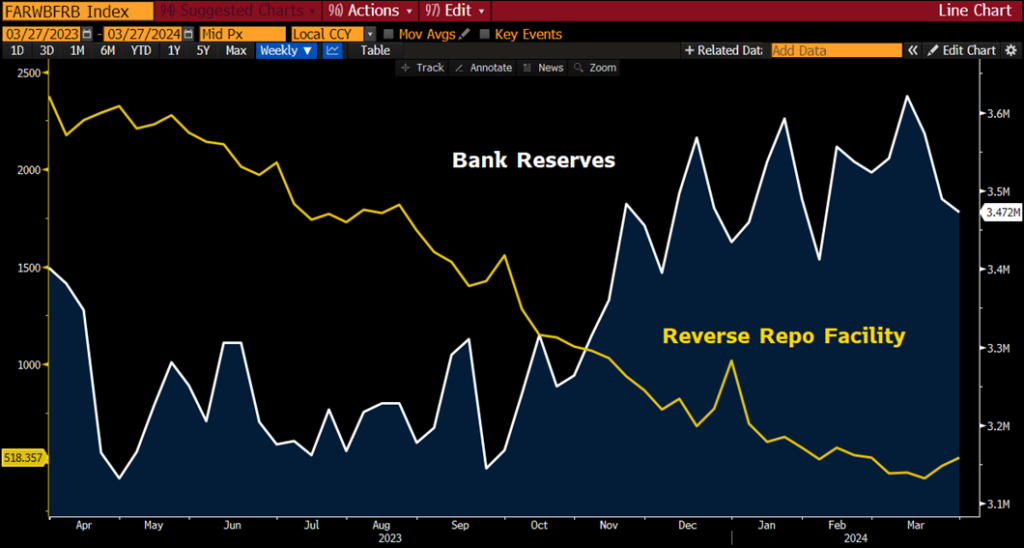

We continue to believe in the strong relationship between bitcoin and excess bank reserves. The recent price action suggests excess reserves have come down this week, which corroborates with the RRP, which has now reached $388bl, compared to $321bl last Wednesday. That means excess reserves went down by $60bl week over week, and probably more given the Fed QT. we know the exact figure tomorrow night when the Fed reports the weekly balance sheet. The RRP is filling up due to the customary month-end flows, but this should reverse once we enter September, and excess reserves are likely to recover a bit as a result.

We continue to believe in the strong relationship between bitcoin and excess bank reserves. The recent price action suggests excess reserves have come down this week, which corroborates with the RRP, which has now reached $388bl, compared to $321bl last Wednesday. That means excess reserves went down by $60bl week over week, and probably more given the Fed QT. we know the exact figure tomorrow night when the Fed reports the weekly balance sheet. The RRP is filling up due to the customary month-end flows, but this should reverse once we enter September, and excess reserves are likely to recover a bit as a result. Seasonality for crypto is often not that good in September, so that may weigh on the space as well. October should be better, because FTX administrators (remember, Sam Bankman-Fried) will begin awarding cash to creditors from the bankrupt crypto broker, estimated around $15bl. A lot of that cash will be used to buy crypto, so this will have the exact opposite effect of the payments-in-kind (meaning creditors received $9bl in bitcoin that was locked up by courts for 10 years!) that were made to Mt Gox creditors this summer. In other words, the FTX cash awards are more bullish bitcoin than the Mt Gox distribution was bearish bitcoin. Note that amidst the Mt Gox distribution pressure, bitcoin went from roughly $72K to $58K.

Seasonality for crypto is often not that good in September, so that may weigh on the space as well. October should be better, because FTX administrators (remember, Sam Bankman-Fried) will begin awarding cash to creditors from the bankrupt crypto broker, estimated around $15bl. A lot of that cash will be used to buy crypto, so this will have the exact opposite effect of the payments-in-kind (meaning creditors received $9bl in bitcoin that was locked up by courts for 10 years!) that were made to Mt Gox creditors this summer. In other words, the FTX cash awards are more bullish bitcoin than the Mt Gox distribution was bearish bitcoin. Note that amidst the Mt Gox distribution pressure, bitcoin went from roughly $72K to $58K. Its interesting that ethereum is outperforming bitcoin today. Normally it lags bitcoin, which suggests that this is indeed large holders (whales) selling bitcoin out of inventory, while other cryptos are going down in sympathy.

Its interesting that ethereum is outperforming bitcoin today. Normally it lags bitcoin, which suggests that this is indeed large holders (whales) selling bitcoin out of inventory, while other cryptos are going down in sympathy. The heart of “conditioning bias” comes down to one sentence. The longer something works, the more players get drawn into playing the game. We know the junkies are on every street corner these days buying call options when the

The heart of “conditioning bias” comes down to one sentence. The longer something works, the more players get drawn into playing the game. We know the junkies are on every street corner these days buying call options when the  As the market grinded higher – more and more capital came into the hands of algos and quants buying the 20-day moving average.

As the market grinded higher – more and more capital came into the hands of algos and quants buying the 20-day moving average.

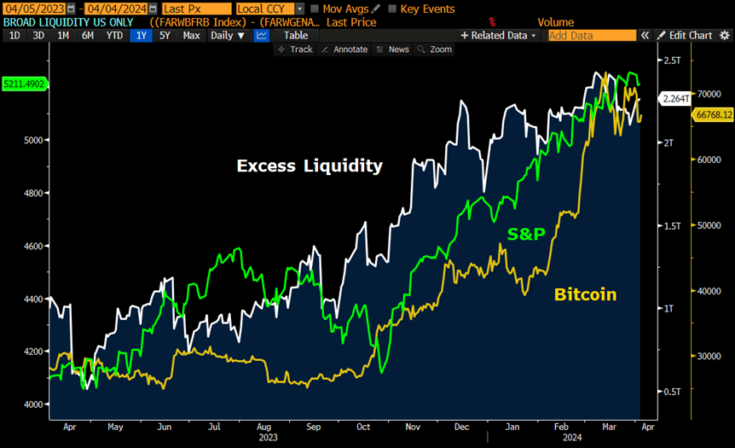

Excess liquidity have surged higher in the last year, which has pushed up risk assets, such as bitcoin and equities.

Excess liquidity have surged higher in the last year, which has pushed up risk assets, such as bitcoin and equities. As the Treasury pushed money out of the RRP, bank reserves held at the Fed have gone up simultaneously. This has been one of the biggest driver of stock market gains

As the Treasury pushed money out of the RRP, bank reserves held at the Fed have gone up simultaneously. This has been one of the biggest driver of stock market gains