Christine Daley was a beautiful person, a unique and rare talent. She will be missed by so many, on and off Wall St. Through the years, there are those moments when someone touches you in a profound and special way, changes your life forever. That’s what Christine meant to me. Nearly everything I know about distressed investing came out of those long, passion-filled discussions with Christine. I am crushed but so grateful for all the good times, the inspiration, and to have been blessed with such an amazing friend. – LGM

Excerpt from the New York Times bestseller, “A Colossal Failure of Common Sense” – Now published in 12 languages.

My opening day was spent meeting and spending time with our most important research analysts with whom I would be in constant touch. The first was Christine Daley, who was in her thirties at the time and head of distressed-debt research. Christine was a vulture’s vulture and Lehman’s finest. They say she could tell you to the penny what General Motors was worth at any given moment in the week, even in the auto giant’s darkest days—particularly in the auto giant’s darkest days. Christine was a beautiful, slim, immaculately dressed Italian-American. She was watchful and very skillfully set out to find out precisely what I knew. It was crystal clear, her trust would NOT come easily, it would have to be earned in the months and years to come. And she had a towering reputation as a researcher who could slice and dice any big corporation and swiftly come up with an eye-watering correct valuation. A true Hall-of-Famer in the U.S. distressed investing universe. From hedge fund to hedge fund, asset manager to asset manager, everyone had the highest respect for Christine, she was that special. Unsurprisingly, she had graduated magna cum laude from the College of New Rochelle with departmental honors in all semesters. At New York University Stern School of Business, she graduated number one in her class, which was doubtless no shock to anyone.

Especially Christine Daley, for it was she who administered my first serious test of character and knowledge in the first week of my employment at Lehman. The subject was one of the largest energy producers in the United States, the wholesale electricity giant Calpine, out of San Jose, California. At their peak, they owned almost a hundred gas turbines and power plants in twenty-one states, with natural gas fields and pipelines in the Sacramento Valley and 22,000 megawatts of capacity. Calpine ranked among the world’s top ten electricity producers, with assets worth billions and billions. They did, however, have one serious problem. Christine Daley, our iron-souled Lehman researcher, thought they would almost certainly go bust, and she was recommending we take a massive short position in this company. That took a lot of guts, because Calpine’s creed of clean energy—the cleanest possible energy, turbines off which you could eat your lunch, emissions from which spring flowers would sprout, electricity so pure and spotless it would safely caress a newborn child—made it beloved among investors. “Bullshit,” said Christine inelegantly. “They’re going down. That CFO of theirs could dance through raindrops without getting wet.” (Calpine would file Chapter 11, bankruptcy protection a year later).

Serial Convertible Bond Issuers

SunEdison*

Chesapeake Energy*

Molycorp*

Lehman*

iStar Financial*

Calpine*

Fannie Freddie*

Enron*

Tyco*

Adelphia*

Six Flags*

eToys*

Avaya*

Worldcom*

SunEdison*

Tesla

*Filed Chapter 11

Bloomberg data

Anyhow, to return to my first major meeting, we sat together, and in the first five seconds, I understood why I was there. She knew all about my background in convertible bonds. She knew about the sale of ConvertBond.com to Morgan Stanley, a game-changer for my career (Steve Seefeld and I founded the company in 1997). Calpine had loads of convertible debt and Christine understood the capital structure better than anyone on the planet. Instantly, her skepticism toward this darling of the investment world was loud and clear. “What do you know about them?” she asked. “And what do you think about Bob Kelly, the CFO?” I told her I knew two major facts. They had one hell of a debt load, a lot of it was convertible. They were a serial issuer of this flavored bond, a classic warning sign indeed. Over the last 30 years, companies issuing more than one convertible bond in a three year period – filed bankruptcy protection in over 85% of the time, our research showed. I’d never been entirely convinced about Calpine, and in turn, she questioned me about who would get paid, and when, upon the bonds’ maturity. She wanted to know if Calpine could settle their convertible preferred shares for cash, or whether they could just box their way out and issue more shares. We spoke of the convertible preferred stockholders—the guys who stand one-tier higher than equity in the corporate capital structure.

Trying my hardest to impress this high Queen of U.S. distressed investing, I utilized the finest Wall Street jargon, stressing that each one of the convertible preferreds had a different delta and a different gamma. I will not easily forget the speed with which she cut me off in midsentence. “Never mind that ConvertBond.com mumbo jumbo,” she snapped. “I am concerned with what the company can do to defer paying the dividends and defer their obligations to repay these preferred shareholders because I can see a big fight developing right here.” “What kind of fight?” I asked, a bit lamely. “The kind that starts when the preferred shareholders are senior to about $19 billion worth of debt, some secured, some unsecured,” she replied. “That kind.” “Because the convertible preferred stock matures well before the debt, right? Kind of seniority by maturity,” I said. “Exactly,” she agreed. “But I think the bank debtors will organize, hire some hotshot lawyer, and stage a battle in a courtroom, try to force Bob Kelly’s hand, force him to cram down the preferred stockholders, while the bankers grab what there is of Calpine’s assets.”

“That would be a dividend roadblock, stopping all payments to the preferreds that mature in the next two years.” Correct I thought. They’d all lose out to the banks. Christine Daley was as sure of her ground as anyone I’d ever met. She was convinced the cash flow of Calpine was nothing like good enough to support the gigantic debt the corporation carried. She knew there were bonds all over the place, many of them in different parts of the capital structure. There were first-lien and second-lien bank debt, senior secured notes, and a ton of unsecured straight debts. The last in line for repayment were three different convertible preferred debts.

In Christine Daley’s opinion, Calpine was constantly robbing Peter to pay Paul, and constantly pushing the legal envelope, ducking and diving around the covenants that governed the financial structure of their debt. The entire corporation was structured to confuse the life out of the analysts as the company moved money from place to place, trying to stay solvent. Our equity department at Lehman had fallen in love with the company, they were long millions of shares and it was now my job to get them OUT of this colossal piece of risk. In each meeting, their excitement, bullish posture grew. Christine did not buy it. The distressed (debt) and high yield fixed income departments despised Calpine, while it was a darling of the equity desk. What a mess. I could see she cared passionately, “we MUST convince those guys to sell, and sell quickly,” she said. (Within a few months everyone was on the same page, short, thanks to Christine).

The look in her eyes was one of pure defiance, and it was backed by a laser beam of logic from which she could not be deviated from. Christine was determined to persuade Lehman Brothers to take a huge short position. I thought of the massed ranks of lawyers and smart-ass execs who must be lined up against her, this one voice of profound certainty that stood alone against them.“ Calpine cannot last a year,” she said as I was leaving. “And we are going to make millions of dollars watching them go bankrupt. It’s just a hall of mirrors. Trust me, they’re already broke.” “I’m with you all the way,” I told her. “I always thought they were suspect. Which is why I never traded their bonds on the long side, just short.” But she needed no encouragement. I never heard anyone express a corporation’s forthcoming woes better than Christine. You don’t often meet a soothsayer with an AK-47. As I walked away from her desk, back to my own space on the trading desk, I pondered that Calpine scenario. It was, of course, the oldest trick in the corporate playbook, building a vast network of separate components, corporations with different identities, and moving cash between them.

One (power) plant needs a few million, so you get it from another, pay it out, then pay it back from somewhere else. It’s a process that can go on for years, removing the money and making big transfers all over the place, until no one knows where the money is, where it came from, where it went, or even whether it’s real. All the while firms like Calpine would keep coming to Wall Street and issuing more debt, the bankers loved them. Christine knew “real” when she saw it. And among all of that vast sea of numbers that made up Calpine’s introverted/extroverted, hot/cold, now-you-see-it-now-you-don’t balance sheet, only two mattered to her: her own year-end prediction of $650 million of Calpine EBITDA (earnings before interest, taxes, depreciation, and amortization) versus a truly daunting debt load of $18.5 billion.“ They have only one real chance,” she had told me. “They’ll have to trip at least one of those bond covenants. They don’t have any choice.”It should be remembered that the end of 2004 was a very rosy time for the fixed-income markets. And for Christine Daley to come out and predict a major bankruptcy in a healthy market and economy was, I thought, an act of supreme daring and high confidence. Also, she was vocal in her views. Her faith and resolve knew no bounds. She knew, of course, that Calpine was continually coming to the convertible market with bond after bond, 6 percent converts—the Last Chance Saloon for an outfit trying to get their hands on heavy capital.

They were always trying to convince one of their largest bondholders, the gutsy Ed Perks of Franklin Mutual Funds, to lend them even more money through those convertible bonds. That probably the soundest way out when you have mounting operating costs, a debt mountain with rising interest expenses, and falling earnings. Meanwhile, out on the Street, there was no letup in the lovefest for Calpine stocks and bonds. For cynics like Christine and me, it seemed nothing short of a cult following, with wide-eyed investors eager to play their part in the world’s cleanest industrial energy program. We could see them rushing to the colors of the green flag with missionary, idealistic zeal. Oh, to be a part of the least-polluting, the newest fleet of gas turbine plants in the world. Oh, to repair that shuddering hole in the ozone layer, re-ice the Arctic, stem the warming tides, save the stranded polar bears, replant the rainforest … Mayday! Mayday! Save our planet! Of course, Christine Daley and I knew it should have been save our ship, not save our planet because the green ship Calpine was holed below the waterline.

For mayday read payday—for the Calpine directors, that is. Not for the preferred stockholders, who were about to get crunched by the banks. As were the holders of Calpine equities. The only interested party likely to come out of this laughing was Lehman Brothers because they had Christine Daley and they were listening to her. Go sport, baby, go short, in the biggest possible way. Of course, back in Calpine’s headquarters in San Jose the name Christine Daley was not universally loved. Wall Street has one of the most sensitive radar systems in the world. The network is a 24/7 communications sprawl into which every single member of the finance industry is, on some level, tuned. Christine, conducting her traditional scorched-earth policy while researching critical information, spoke to many, many important people. I am sure they asked her advice, I am equally sure people asked her about any new bond that had just been issued by Calpine. And these people were often clients of Lehman brothers. Christine was honor-bound to provide them with an honest assessment. I am sure that for many months she turned people off Calpine, shared with them her fears that this giant archipelago of power plants carried too much debt to be considered a buy, either shares or bonds. In sunlit San Jose, I have no doubt she was regarded as the Princess of darkness. They did not, I hasten to add, believe she was treating them unfairly because they knew the score as well as she did. Christine was the Wall Streetsleuth who had them nailed. After that first meeting with her, I wondered just how many people around there knew as much as she did.

Lehman Brothers’ distressed and convertible securities departments would end up making over $190 million dollars short Calpine debt and equity, all thanks to the conviction and passion of Christine Daley.

Dollar bulls have run for the hills at the second most fierce pace in the last seven years.

Dollar bulls have run for the hills at the second most fierce pace in the last seven years.  In the US, fiscal stimulus was supposed to struggle to cap the revenue drop caused by the unprecedented nature of this crisis. To an extent, it has, but what this narrative missed in a distributional sense is, the policy response to deflationary shocks has changed. The government sends out money and the central bank does open-ended QE. Does this mean future growth is promised, no, but it does change the recession landscape in terms of size and duration? Long-drawn out deflationary episodes have to be repriced as we seem to have a better recipe for dealing with them as opposed to 2008.

In the US, fiscal stimulus was supposed to struggle to cap the revenue drop caused by the unprecedented nature of this crisis. To an extent, it has, but what this narrative missed in a distributional sense is, the policy response to deflationary shocks has changed. The government sends out money and the central bank does open-ended QE. Does this mean future growth is promised, no, but it does change the recession landscape in terms of size and duration? Long-drawn out deflationary episodes have to be repriced as we seem to have a better recipe for dealing with them as opposed to 2008. A clear down parallelogram was formed as a result of March high into the June low. Subsequently, it broke through the bottom line of the parallelogram, which sets up an early resolution, i.e. it sets up an early test of the apex price point. If that fails, it is in free fall.

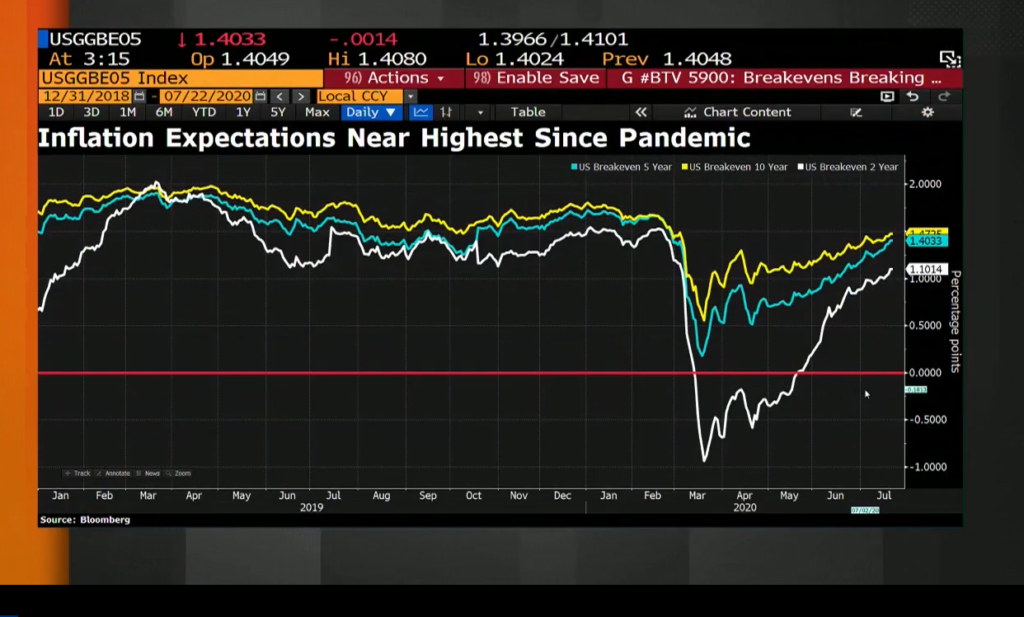

A clear down parallelogram was formed as a result of March high into the June low. Subsequently, it broke through the bottom line of the parallelogram, which sets up an early resolution, i.e. it sets up an early test of the apex price point. If that fails, it is in free fall. Has the Japanese yen become the world’s risk-off currency? Hard to process a $4 to $5 trillion federal deficit under a Republican Administration without concluding that either inflation is around the corner of the dollar is going to substantially weaken or most likely both. Some feel a blue-wave will lead to even more MMT experiments (modern monetary theory)?

Has the Japanese yen become the world’s risk-off currency? Hard to process a $4 to $5 trillion federal deficit under a Republican Administration without concluding that either inflation is around the corner of the dollar is going to substantially weaken or most likely both. Some feel a blue-wave will lead to even more MMT experiments (modern monetary theory)? Real bond yields are plunging. Say you’re a billionaire in the middle-east with loads of short-term treasuries. Your return on investment, after inflation expectations, is paltry. What can you do?

Real bond yields are plunging. Say you’re a billionaire in the middle-east with loads of short-term treasuries. Your return on investment, after inflation expectations, is paltry. What can you do?  The gold bugs have been lost for decades, precious metals have always been a game played on the fixed income field.

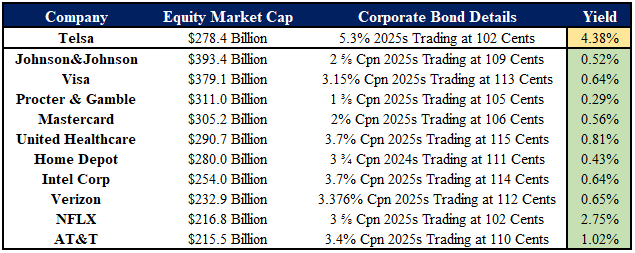

The gold bugs have been lost for decades, precious metals have always been a game played on the fixed income field.  This is remarkable data, Tesla’s five-year bonds are yielding nearly 400bps more than their possible market capitalization neighbors in the S&P 500.

This is remarkable data, Tesla’s five-year bonds are yielding nearly 400bps more than their possible market capitalization neighbors in the S&P 500. See

See  Microsoft, very quietly lost $100B this week. On Friday, MSFT equity closed

Microsoft, very quietly lost $100B this week. On Friday, MSFT equity closed  As passive flows surge, they flow into MSFT, not Berkshire*. Over the last 5 years, there’s an additional $2T that’s flowed into the passive bucket relative to active asset management.

As passive flows surge, they flow into MSFT, not Berkshire*. Over the last 5 years, there’s an additional $2T that’s flowed into the passive bucket relative to active asset management. In another disturbing turn of events, for only the second time since the March lows, MSFT closed

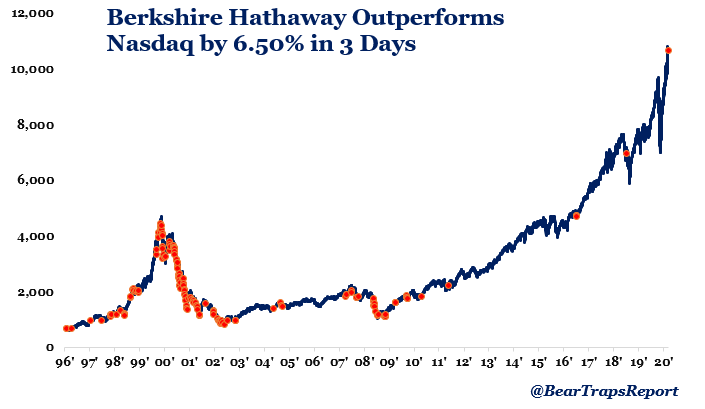

In another disturbing turn of events, for only the second time since the March lows, MSFT closed  The Russell 2000 Index ripped higher by nearly 4% on Wednesday while the Nasdaq was relatively flat. Looking over the past 2 decades, when the Nasdaq (growth stocks) experiences this severe an underperformance vs. the Russell 2000 (value) it has usually coincided with the peak and/or downtrend of a cycle. A similar dynamic has played out with Berkshire Hathaway which as of yesterday’s close, has outperformed the Nasdaq by over 6.5% in the past 3 days. This is only the 3rd time since 2012 where BRK outperformed the Nasdaq by this much.

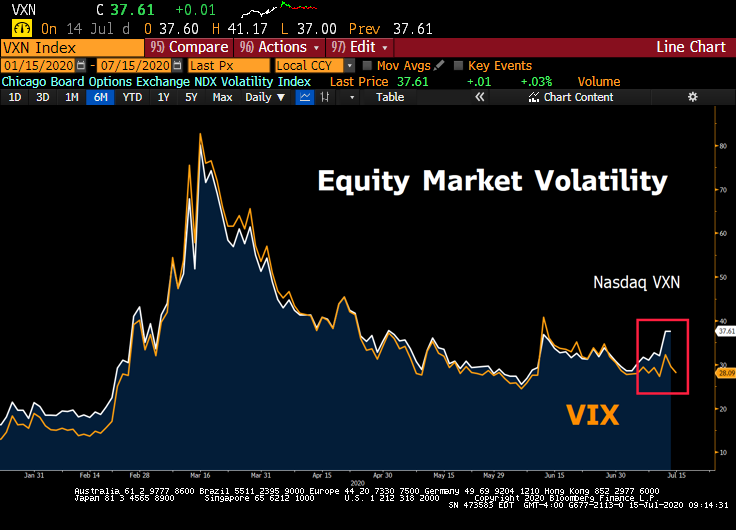

The Russell 2000 Index ripped higher by nearly 4% on Wednesday while the Nasdaq was relatively flat. Looking over the past 2 decades, when the Nasdaq (growth stocks) experiences this severe an underperformance vs. the Russell 2000 (value) it has usually coincided with the peak and/or downtrend of a cycle. A similar dynamic has played out with Berkshire Hathaway which as of yesterday’s close, has outperformed the Nasdaq by over 6.5% in the past 3 days. This is only the 3rd time since 2012 where BRK outperformed the Nasdaq by this much. The Chicago Board Options Exchange NDX Volatility Index rose to 38 on Tuesday, an 8+ points premium to the CBOE VIX Index. That’s the widest spread since 2004. The gap between volatility in large-cap high fliers and the broader index has run the gamut in a matter of months, going from negative to non-existent to a multi-year high. Investors are paying-up for downside protection on NASDAQ high flyers.

The Chicago Board Options Exchange NDX Volatility Index rose to 38 on Tuesday, an 8+ points premium to the CBOE VIX Index. That’s the widest spread since 2004. The gap between volatility in large-cap high fliers and the broader index has run the gamut in a matter of months, going from negative to non-existent to a multi-year high. Investors are paying-up for downside protection on NASDAQ high flyers.