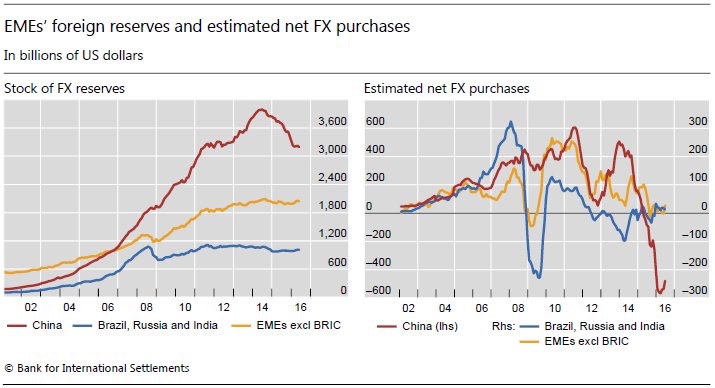

“The seventeen year river of currency reserve buildup is no longer flowing.”

David Tepper

“Economists are still expecting 4-5 hikes in 2016 and the street (futures market) is pricing in 2-3 over the next year. We believe volatility and global credit risk will force the Federal Reserve to be on hold for a rate hike in March and for that matter the rest of the year. Credit risk will veto the Fed’s desired policy path, take the steering wheel out of their hands. When the market realizes this, the dollar will fall and commodities will surge”.

Bear Traps Report, January 5, 2016

Breaking News: One of our Lehman Risk Indicators is Flashing Bight RED

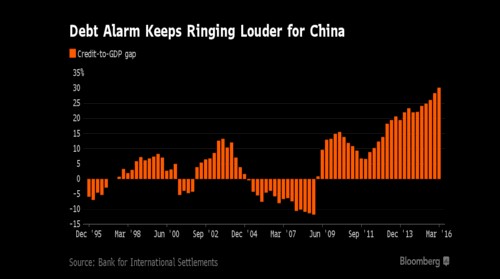

Credit Stress in China’s Banking System Reaches an All Time High

Credit-to-GDP ‘gap’ exceeds all other nations, says BIS study

This weekend, the Bank of International Settlements announced a warning indicator for banking stress rose to a record in China in the first quarter, underscoring risks to the nation and the world from a rapid build-up of Chinese corporate debt.

In Q1, credit stress in China surged to a fresh record. As we covered in our Bear Traps reports last year, a nearly 20% spike in the U.S. dollar has the credit impact of a global wrecking ball. We made the argument the dollar’s accent has had the impact of 3-4 Federal Reserve rate hikes. Today, it’s rewarding to find much of Wall St’s analysts are finally waking up to this reality.

China is using debt to generate economic activity at its highest rate EVER. Unfortunately, they’re getting substantially less return on leverage today then ever before. Eight years of aggressively accommodative monetary policy from the U.S. federal reserve has consistently shifted capital into places it JUST SHOULDN’T BE. As the Fed tries to EXIT the zero lower bound, the global credit contraction implications are mind blowing powerful.

China 2006-2016

Credit Growth: 1100%

GDP Growth: 500%

Hayman Capital data

After the Fed made their attempt at one rate hike, the dollar’s surge resulted in a sharp contraction in the total stock of dollar denominated credit to emerging markets. This is a key measure of global liquidity, it was down at $3.2T at the end of March, off $137B year over year, BIS data.

Credit risk has surged globally, the Fed has this mess on it’s hands.

China’s credit-to-gross domestic product “gap” stood at 30.1 percent, the highest for the nation in data stretching back to 1995, according to the Basel-based Bank for International Settlements. Readings above 10 percent signal elevated risks of banking strains, according to the BIS, which released the latest data on Sunday, Bloomberg reported.

The gap is the difference between the credit-to-GDP ratio and its long-term trend. A blow-out in the number can signal that credit growth is excessive and a financial bust may be looming.

Thirty-year government bonds capped their biggest weekly slump since April 2013 after the BOJ refrained from purchasing the securities at its regular market operation on Sept. 2nd.

Thirty-year government bonds capped their biggest weekly slump since April 2013 after the BOJ refrained from purchasing the securities at its regular market operation on Sept. 2nd.

Creating temporary short squeezes has become a national summer past time in some oil producing nations. Over the years in oil markets one thing has become very reliable. When you see “plans” with few ambitious announcements, there’s typically a lack of decisive follow-up action.

Creating temporary short squeezes has become a national summer past time in some oil producing nations. Over the years in oil markets one thing has become very reliable. When you see “plans” with few ambitious announcements, there’s typically a lack of decisive follow-up action.

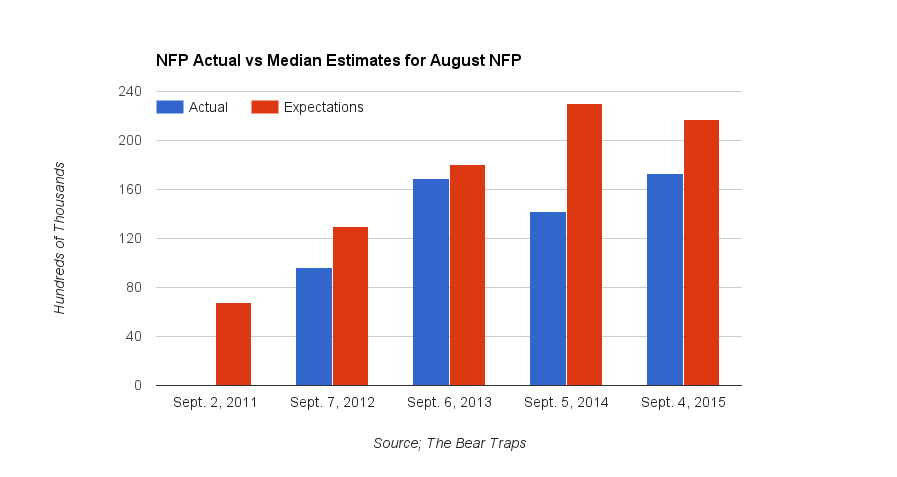

August has been light in recent years, so the market was ready for weakness.

August has been light in recent years, so the market was ready for weakness.