Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Lawrence McDonald is the New York Times Bestselling Author of “A Colossal Failure of Common Sense” – The Lehman Brothers Inside Story – one of the best-selling business books in the world, now published in 12 languages – ranked a top 20 all-time at the CFA Institute.

Most Crowded Trade – All Time

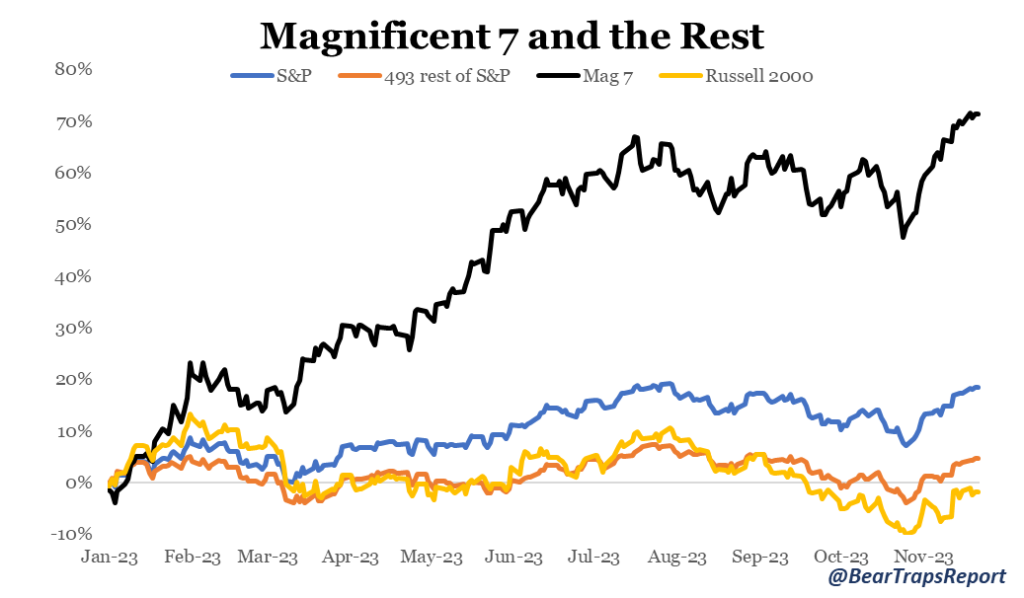

The S&P is on course to gain ~18%, but without the Magnificent 7 (+71% YTD), the S&P is only up 5% for the year. The Russell 2000 index of small caps is even down year to date. This dispersion in performance means that investors should have some large capital gains, but also some steep capital losses spread among a variety of the stocks in their portfolios. In years where we find significant divergence between winners and losers – the data shows that is where the opportunities are most attractive.

Winners vs. Losers – S&P 500

This brings us to the January effect. There are two forces that have a significant influence over markets between November and January: Window dressing by mutual fund managers and tax loss selling by individual investors. By year-end, they want ALL of the ugly names off the pad – at the same time they all love to show off the winners.

What is Window Dressing?

Mutual fund portfolio managers want to show as many of the year’s winners in their portfolios in their year-end statements. Their clients, the investors in their funds will receive those statements in early January and the more winners the portfolio has, the more impressed those investors are. As such, mutual fund managers tend to buy more of the best-performing stocks in the last two months and sell down their losers.

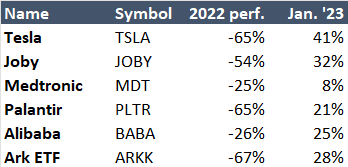

Q4 2022 Losers vs Winners

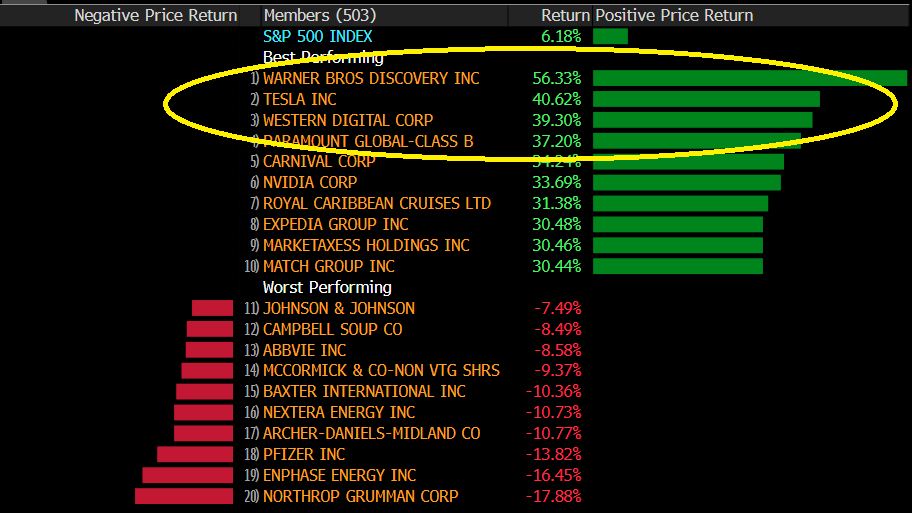

Many of the Q4 2022 losers became winners in early 2023.

Many of the Q4 2022 losers became winners in early 2023.

Early Winners in 2023

Q4 losers into Q1 winners.

Q4 losers into Q1 winners.

2023 Full Year

The year 2023 will go down as an epic haves vs. have nots.

The year 2023 will go down as an epic haves vs. have nots.

In addition, other classes of investors that incur capital gains taxes also sell some of their losers in the last weeks of the year to offset their capital gains. This effect is especially pronounced in years of strong market gains. As such, the year’s strongest stocks tend to rally further into year-end, while losers continue to see selling pressure as the year ends.

The table above shows that in years when the S&P has strong returns, January is often a relatively weak month as people wait to sell their winners until January. At the same time, some of last year’s losers tend to rebound strongly in January, as the selling pressure disappears. This is the January effect.

DJIA vs. QQQ

Tax Loss Basket 2022 – A year ago, there was a Q4 overdose into DJIA names, and out of the QQQs, but we are seeing the climax opposite with positive divergence favoring the DJIA in Q1 2024. The Dow Industrials are extremely cheap vs. the ridiculously crowded QQQs. There is close to $19T in the Nasdaq 100, up from $12.5T in January 2023.

This was the BearTraps’ Tax loss selling basket by the end of 2022

In 16 trade alerts, we positioned clients in beaten-down names in Q4 2022. NOT listed above was our CRM Salesforce position, CRM equity was up 70% in 1H 2023, see below.

In 16 trade alerts, we positioned clients in beaten-down names in Q4 2022. NOT listed above was our CRM Salesforce position, CRM equity was up 70% in 1H 2023, see below.

CRM Trade Alerts

Our 7-Factor Capitulation model delivered a strong buy. We were aggressive buyers of CRM equity in Q4 2022.

Our 7-Factor Capitulation model delivered a strong buy. We were aggressive buyers of CRM equity in Q4 2022.

Please reach out to tatiana@thebeartrapsreport.com to get on our CLIENT trade alerts.

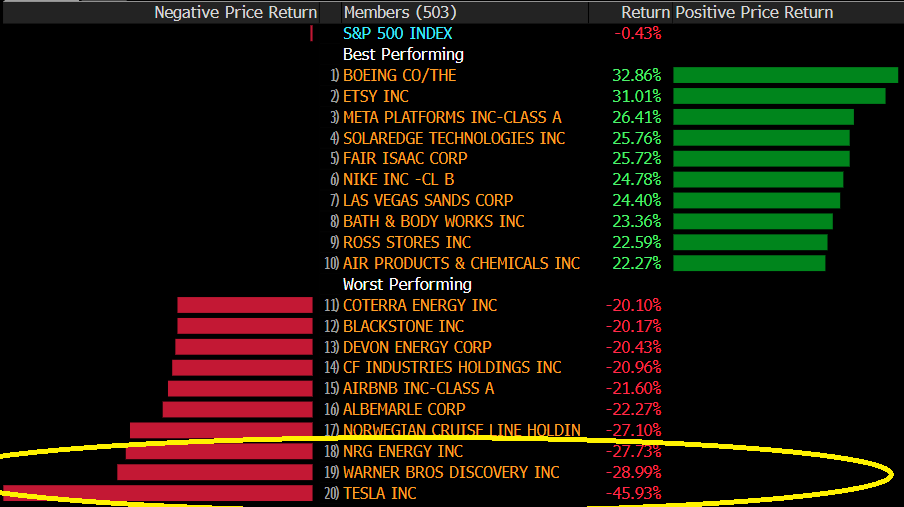

So far in the year, the worst performers in the S&P are the solar stocks, Enphase (ENPH) and SolarEdge (SEDG), lithium miner FMC Corp. (FMC), Covid vaccine makers PFE and MRNA, and some retailers like DG and WBA.

1) Buy Solar: Enphase (ENPH) and Solar Edge (SEDG)

The TAN solar ETF is the cheapest to the QQQs all time.

The TAN solar ETF is the cheapest to the QQQs all time.

What has plagued solar this year? A combination of high interest rates hitting demand, distributors working through high inventory levels, and a policy change reducing incentives in California, has made it a tough year for residential rooftop solar stocks. Higher interest rates make it more expensive to finance solar and it makes it less economical for companies and individuals to adopt solar. In addition, the plunge in prices of natural gas have limited electricity price inflation. This also removed an incentive for homeowners and corporations to adopt solar. Solar stocks have been the worst performers in 2023. Ultimately, ENPH is down 72% from the late 2022 highs and SEDG is down 80% from the all-time high. PMs and individual investors are undoubtedly dumping those stocks in the final weeks of the year as they want them out of the portfolio or to book capital losses. We think these stocks could rebound in January as the selling dries up. Some of these investors will buy back the very same stocks they sold for tax reasons. According to the tax code, an investor needs to wait 30 days before repurchasing the stock they sold. A decline in interest rates, something the rates market is anticipating for 2024, would give a boost to the beleaguered solar stocks. In addition, we should get an update on the solar subsidies from the Inflation Reduction Act, which could help sentiment on these stocks.

2) Buy Fertilizer and Crop Protection

Crop protection companies vs Soft Commodities

FMC Corp (FMC) and Mosaic (MOS) have been among the worst-performing stocks this year, with FMC down 90% from the March ’22 highs. Fertilizer and crop protection stocks have been selling off all year together with crop commodities. We think FMC and MOS have now also become a victim of tax loss selling/window dressing and these stocks should improve once the tax loss selling has subsided.

FMC Corp (FMC) and Mosaic (MOS) have been among the worst-performing stocks this year, with FMC down 90% from the March ’22 highs. Fertilizer and crop protection stocks have been selling off all year together with crop commodities. We think FMC and MOS have now also become a victim of tax loss selling/window dressing and these stocks should improve once the tax loss selling has subsided.

3) Buy the Government Sponsored Enterprises (GSEs)

Fannie Mae (FNMA) soared when Trump was elected in 2016, and clobbered when SCOTUS killed the Sweep Lawsuits.

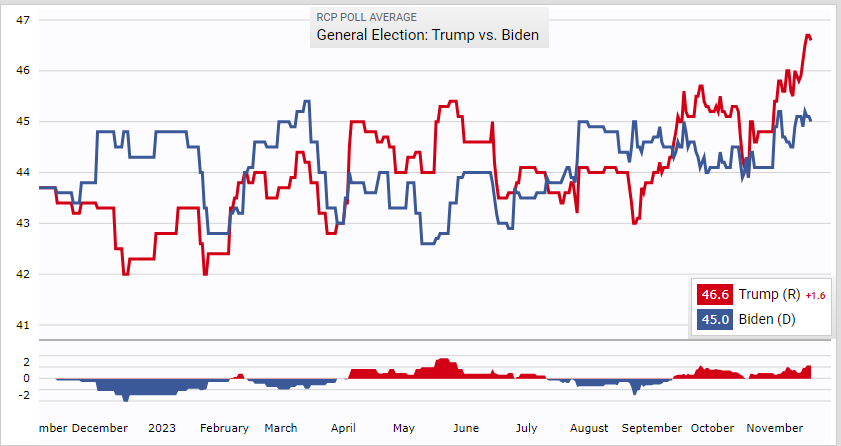

One of our favorite tax loss trades is Fannie Mae (FNMA) and Freddy Mac (FMCC) . These stocks were decimated in 2021 after the court rejected claims that the Federal Housing Finance Agency exceeded its authority in collecting more than $100 billion in profits from the Government Sponsored Enterprises (GSE). Hedge funds had crowded into this trade and sued the FHFA for this sweep, hoping the courts would decide in their favor. When they didn’t, hedge funds fled the stock and it collapsed. Surely there are still plenty of people who hold the stock at a loss, and we could see some selling pressure on the stock (and the preferreds) into New Year. However, the presidential elections are in November of 2024. While it is extremely hard to forecast who will win these elections, the polls currently favor Trump slightly, while the betting sites attach even odds to Biden and Trump (~40%). After the 2016 election, FNMA and FMCC common stock soared to $4.5 and $4.3 per share respectively on the hopes that the GSEs would be privatized. If we believe that a Trump victory could once again trigger speculation over a privatization, then the fair value of FNMA and FMCC is worth $1.8 and 1.72 per share and not 70 cents (40% odds of a $4.5 stock price after the election).

One of our favorite tax loss trades is Fannie Mae (FNMA) and Freddy Mac (FMCC) . These stocks were decimated in 2021 after the court rejected claims that the Federal Housing Finance Agency exceeded its authority in collecting more than $100 billion in profits from the Government Sponsored Enterprises (GSE). Hedge funds had crowded into this trade and sued the FHFA for this sweep, hoping the courts would decide in their favor. When they didn’t, hedge funds fled the stock and it collapsed. Surely there are still plenty of people who hold the stock at a loss, and we could see some selling pressure on the stock (and the preferreds) into New Year. However, the presidential elections are in November of 2024. While it is extremely hard to forecast who will win these elections, the polls currently favor Trump slightly, while the betting sites attach even odds to Biden and Trump (~40%). After the 2016 election, FNMA and FMCC common stock soared to $4.5 and $4.3 per share respectively on the hopes that the GSEs would be privatized. If we believe that a Trump victory could once again trigger speculation over a privatization, then the fair value of FNMA and FMCC is worth $1.8 and 1.72 per share and not 70 cents (40% odds of a $4.5 stock price after the election).

Polling Average for 2024 Election

Polling averages for the 2024 election shows Trump now with a slight lead over Biden.

4) Buy Disney (DIS)

DIS – Down 53% since February 2021 Top

There are a number of upcoming catalysts for the stock, including the Comcast/Hulu deal, NBA renewal, ESPN partnership announcement and potential asset sales. DIS in now in the process of controlling costs, and its booking progress. The next step for DIS will be to return to revenue growth. ESPN+ streaming and repositioning Disney + /Hulu are part of this growth strategy. A recent deal with Charter allows for Ad supported Disney + to be available to all 10ml Charter subscribers. For ESPN there is a catalyst to tie it to its newly forged $2bl sports betting alliance with PENN. The challenges for DIS are to halt or at least slow down the decline in linear media. Also, DIS will continue to have to invest in things like Disney + and NBA etc to return to growth. These FCF headwinds will continue to weigh on the stock in 2024. We like DIS especially because we believe it is a tax loss selling candidate and it is likely to enjoy a rebound in January as the tax loss selling subsides. The stock is no longer expensive, at 12x fwd EV/EBITDA.

There are a number of upcoming catalysts for the stock, including the Comcast/Hulu deal, NBA renewal, ESPN partnership announcement and potential asset sales. DIS in now in the process of controlling costs, and its booking progress. The next step for DIS will be to return to revenue growth. ESPN+ streaming and repositioning Disney + /Hulu are part of this growth strategy. A recent deal with Charter allows for Ad supported Disney + to be available to all 10ml Charter subscribers. For ESPN there is a catalyst to tie it to its newly forged $2bl sports betting alliance with PENN. The challenges for DIS are to halt or at least slow down the decline in linear media. Also, DIS will continue to have to invest in things like Disney + and NBA etc to return to growth. These FCF headwinds will continue to weigh on the stock in 2024. We like DIS especially because we believe it is a tax loss selling candidate and it is likely to enjoy a rebound in January as the tax loss selling subsides. The stock is no longer expensive, at 12x fwd EV/EBITDA.

5) Buy beaten-down Retailers and Apparel

Retail: NKE, TGT and VSCO

Many retailers and apparel companies have sold off hard throughout 2022 and 2023. One notable apparel bellwether that has fallen on hard times has been NKE. TGT is another retailer that has suffered from declining purchasing power among its customers and bloated inventories. VSCO spun off Bed & Bodyworks several years ago and has been challenged by consumer trends away from their core product (intimates) as well as a negative sentiment. We believe that these stocks should rebound in January, on more favorable comps (NKE, TGT) and an end to tax loss selling. Note that Dicks (DKS) reported robust Q3 results, which suggests athletic sales are improving.

Many retailers and apparel companies have sold off hard throughout 2022 and 2023. One notable apparel bellwether that has fallen on hard times has been NKE. TGT is another retailer that has suffered from declining purchasing power among its customers and bloated inventories. VSCO spun off Bed & Bodyworks several years ago and has been challenged by consumer trends away from their core product (intimates) as well as a negative sentiment. We believe that these stocks should rebound in January, on more favorable comps (NKE, TGT) and an end to tax loss selling. Note that Dicks (DKS) reported robust Q3 results, which suggests athletic sales are improving.

6) Buy lithium

Albemarle (ALB) and Quimica (SQM)

ALB and SQM have been among the worst performing stocks this year, with FMC down 90% from the March ’22 highs and SQM 56% from the September ’22 high. We think FMC ad SQM have also become a victim of tax loss selling/window dressing. There is an excess inventory of lithium in the channel, and as a result lithium prices have weakened a lot, which explained their plunge this year. But China EV sales for October, the largest market in the world, were extremely strong. Rising EV sales will eventually translate into more lithium demand or inventory depletion. We think the selling in these stocks has been overdone and we should see a rebound in January.

ALB and SQM have been among the worst performing stocks this year, with FMC down 90% from the March ’22 highs and SQM 56% from the September ’22 high. We think FMC ad SQM have also become a victim of tax loss selling/window dressing. There is an excess inventory of lithium in the channel, and as a result lithium prices have weakened a lot, which explained their plunge this year. But China EV sales for October, the largest market in the world, were extremely strong. Rising EV sales will eventually translate into more lithium demand or inventory depletion. We think the selling in these stocks has been overdone and we should see a rebound in January.

7) Buy Cannabis MSOS

Strong Evidence – Seller Exhaustion

Our seven factor capitulation model is picking up on a few attractive developments. a) The MSOS ETF made a new low in Q3 2023, WITHOUT a confirmation from the weekly RSI. In other words, there is a positive divergence, the RSI has improved over the last 6-months. This is a sign of seller exhaustion, something you want to see in Q4, heading into the new year. b) Meaningful up volume arrived in recent months. Most of the weak hands that owned the shares much higher have been taken out, while a new class of MSOS share ownership, now owns the shares at a MUCH lower price. This is just what you want to see heading into the new year and speaks to potentially attractive returns in 1H 2024.

Our seven factor capitulation model is picking up on a few attractive developments. a) The MSOS ETF made a new low in Q3 2023, WITHOUT a confirmation from the weekly RSI. In other words, there is a positive divergence, the RSI has improved over the last 6-months. This is a sign of seller exhaustion, something you want to see in Q4, heading into the new year. b) Meaningful up volume arrived in recent months. Most of the weak hands that owned the shares much higher have been taken out, while a new class of MSOS share ownership, now owns the shares at a MUCH lower price. This is just what you want to see heading into the new year and speaks to potentially attractive returns in 1H 2024.

Special Thanks for ACG Analytics in Washington

And in the Senate now, despite passing a key committee vote and Senator Schumer “vowing” to hold a follow on vote, Steve Daines (lead R supporter) is saying he doesn’t want to hold a vote until he is sure that the House will pass it too… Which means there is a significant chance that this thing just sits in the Senate. Sets us an great year end buying opportunity as tax loss stress climax probably comes in mid November, most of the bear case is well prices in, shares are likely much higher by Q2 next year as the legislative cycle opens up a more attractive risk-reward. In a Presidential election year, we may see decent GOP support for a play for social justice reforms.

Reschedule developments and processes is MSOS Bullish, 1-3 from dangerous narcotic to lower class. Gets rid of the 280E biz deduction ban (a HUGE positive for MSOS companies), large corporate – this is a non-legislative best case. We thought this action would happen closer to the election, Biden admin sees real political upside. SAFE Banking, the latest developments decrease the urgency near term, but to us – SAFE is a near certainty, just timing. There is now more pressure on the GOP to fall in line, support SAFE in 2024. See below.

* In a letter to the Drug Enforcement Agency (DEA), the Department of Health and Human Services (HHS) has recommended that marijuana be reclassified from a Schedule I to Schedule III substance based on a study conducted by the Food & Drug Administration (FDA). The National Institute on Drug Abuse supported the FDA’s findings. This means that the HHS no longer believes that marijuana has “no currently accepted medical use in the United States, a lack of accepted safety for use under medical supervision, and a high potential for abuse,” as described in the Schedule I Definition of Controlled Substance Schedules.

8) Buy Biotechs

XBI Extremely Cheap to the QQQs

In recent weeks, the XBI biotech ETF reached 10-year extremes vs. the Nasdaq 100. A weekly RSI of 18.75 is extremely rare vs. the QQQs. The year 2023, has been another challenging one for biotech stocks. The XBI is 14% off multi-year lows. The ETF has a historically high percentage of companies trading at or below their cash value, making the sector ripe for M&A support. The biotech industry is well-positioned for AI upside, attractive growth potential, and well known rapid advancements in drug developments. Growing demand to treat chronic diseases is always an upside catalyst, but AI innovations should give the sector a meaningful boost in the coming years.

In recent weeks, the XBI biotech ETF reached 10-year extremes vs. the Nasdaq 100. A weekly RSI of 18.75 is extremely rare vs. the QQQs. The year 2023, has been another challenging one for biotech stocks. The XBI is 14% off multi-year lows. The ETF has a historically high percentage of companies trading at or below their cash value, making the sector ripe for M&A support. The biotech industry is well-positioned for AI upside, attractive growth potential, and well known rapid advancements in drug developments. Growing demand to treat chronic diseases is always an upside catalyst, but AI innovations should give the sector a meaningful boost in the coming years.

One Year

XBI: -9%

QQQ: +37%

Two Years

XBI: -39%

QQQ: -1%

Three Years

XBI: -42%

QQQ: +34%

Five Years

XBI: -5%

QQQ: +153%

Bloomberg terminal data.

What is Different Looking Forward?

Generative AI is transforming the biotech industry by accelerating drug development and lowering expenses. It is used in virtual compound libraries, protein engineering, and customized medicine development. Deep learning algorithms and computational capacity fuel generative AI applications, expediting drug discovery and improving personalized medicine therapy.

In biotech, generative AI technologies such as generative models are being utilized to expedite drug discovery, protein engineering, and customized medicine. The AI in biotechnology market share is expected to grow at a 29.7% CAGR until 2032. With Rashmi Kumari.