2016: Annual Real GDP Growing 1.9%

Q4: 2.5% (says NY Fed)

Q3: 3.2%

Q2: 1.4%

Q1: 0.9%

U.S. Economy, Growth in Decline Since 1981

Nominal GDP growth in the U.S. has been in sharp decline since the early 1980s. Economic growth without inflation adjustments; 14% in 1981, 7% in 2005 to 2.8% in 2016. Market’s hope President elect Trump can change this decay.

Nominal GDP growth in the U.S. has been in sharp decline since the early 1980s. Economic growth without inflation adjustments; 14% in 1981, 7% in 2005 to 2.8% in 2016. Market’s hope President elect Trump can change this decay.

Q3 Real GDP was revised higher to 3.2% q/q with real final sales now 2.7% vs. 2.3% vs. the advance estimate. This points to decently strong momentum. However, given the move in the Dollar and interest rates since Q3, Q4 will likely not be as strong.

To get our reports on where the U.S. Dollar and the U.S. economy is headed, join us.

The increase in GDP was largely due to the increase in consumer spending. Much of this spending was in the household services sector, notably on housing and utilities. The upward revision was heavily weighted by increase in consumer spending.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereExports of goods was pretty strong. However considering the Dollar strength and the EM weakness that has ensued, exports will taper off. Exports have been a large part of the GDP uptick since Q2, a reversion in a later revision or Q4 is likely. This will take the headline number back below 3%.

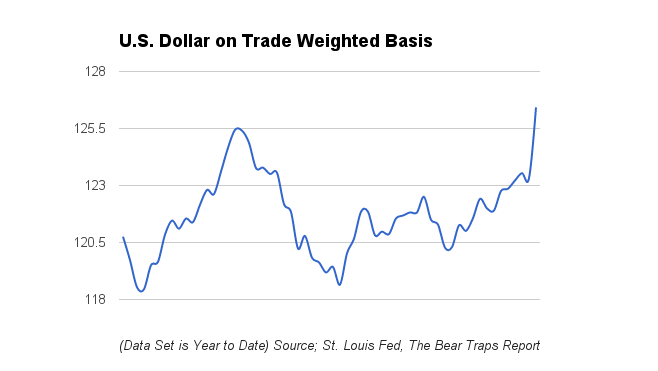

The recent rip in the Dollar since the election will put tremendous pressure on U.S. exports in the coming months. Over 40% of the earnings U.S. companies in the S&P 500 receive, come from overseas.

To get our reports on where the U.S. Dollar and the U.S. economy is headed, join us.

Not all was positive, housing investment and state and local government spending declined.

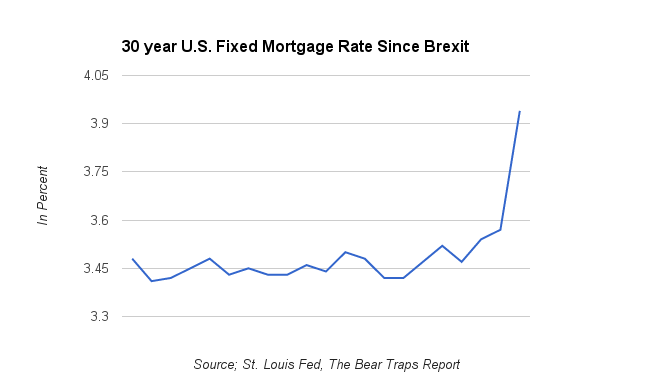

Tighter financial conditions that have developed since the election will certainly weigh on growth in the coming quarters.

Overall we are in a similar state. An acceleration in private inventory investment, exports and federal government spending along with smaller decreases in state/local government spending and a deceleration in nonresidential fixed investment.

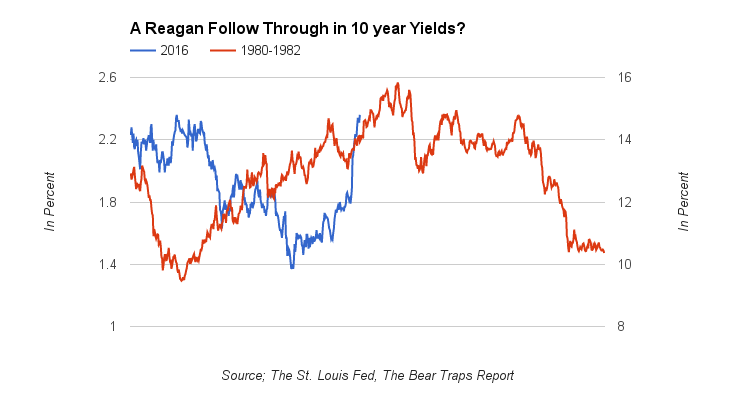

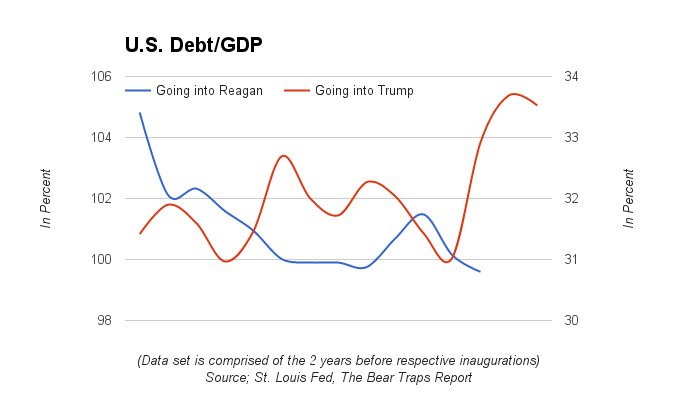

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here It was 1980, the U.S. 10 year Treasury bond yield bottomed out 9.5% in June, by February 1981 yields were 12.7% and nearly 16% by September of that year. The (November 1980) Reagan election brought with it a colossal yield spike, like today inflation was a key concern. However, in the middle of 1981 a recession sent yields much lower to the 10.5% level by November 1982. The paradigm shifted, Reagan’s growth message was halted by a surge in bond yields, the economy reverted back into recession. Ten-year bond yields went down to around 13% by the end of 1981. By the end of 1982, yields had returned to their June lows of 10%.

It was 1980, the U.S. 10 year Treasury bond yield bottomed out 9.5% in June, by February 1981 yields were 12.7% and nearly 16% by September of that year. The (November 1980) Reagan election brought with it a colossal yield spike, like today inflation was a key concern. However, in the middle of 1981 a recession sent yields much lower to the 10.5% level by November 1982. The paradigm shifted, Reagan’s growth message was halted by a surge in bond yields, the economy reverted back into recession. Ten-year bond yields went down to around 13% by the end of 1981. By the end of 1982, yields had returned to their June lows of 10%.

As yields surged 1980 into 1981, U.S. GDP plummeted. This is what we are seeing now, the tightening of the financial conditions is setting the seeds for the next recession.

As yields surged 1980 into 1981, U.S. GDP plummeted. This is what we are seeing now, the tightening of the financial conditions is setting the seeds for the next recession.  Following the financial tightening the economy experienced, a recession ensued. This eventually led to the collapse in rates which saw the 10 year yield lower than it was before Reagan’s election victory.

Following the financial tightening the economy experienced, a recession ensued. This eventually led to the collapse in rates which saw the 10 year yield lower than it was before Reagan’s election victory.