*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

“Averaging” Inflation Does Not Eliminate The Flaws In The Fed’s Policy Approach; It Compounds Them

Larry McDonald with Joe Carson

Federal Reserve has spent over a year conducting a review of its monetary policy strategy, tools, and communication process. The review was an academic re-assessment of an academic experiment called inflation targeting. The new framework of inflation averaging is an extension of the inflation-targeting regime, with a longer timeline.

This decision on inflation targeting moves monetary policy closer to a rule-based framework. A rule-based framework creates the premise that there are no legitimate objectives besides the item being targeted.

Inflation targeting was never supposed to become a rule-based framework. Proponents of the practice argued it would help increase the “transparency” of conventional monetary policy and emphasize the commitment toward maintaining a low and steady inflation environment.

Inflation targeting has never delivered the macroeconomic results that were promised. That’s because it has no practical foundation, focuses on a narrow set of prices that are not entirely market-determined, and creates an uneven playing field between the economy and finance. Inflation averaging will compound the errors.

First, mandating an inflation rate of 2%has no theoretical justification.

There is no such thing as an “ideal” or steady rate of inflation. Policymakers have never offered any empirical evidence to justify a 2% inflation target because none exists.

Research and actual experiences show that an inflation rate too high or too low for an extended period can create imbalances and bad economic outcomes. But that range is very wide.

In the mid-to-late 1990s, reported core consumer price inflation averaged more than 100 basis points above the inflation rate of the last decade, and the macro performance in terms of growth, job creation, and wage gains was far superior.

Policymakers have the freedom to change their operating framework. But any framework should be grounded with solid research and not made up with “alternative” facts to support its use as a policy tool.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Second,inflation targetingfalsely assumes there is absolute perfection in price measurement.

Subtle changes in the prices and quality of goods and services make price measurement at times a “best guess”. Every year government statisticians face new products, changes in old products, shifts in demand, and company pricing strategies.

One of the most complex issues in price measurement is the pervasiveness of item replacements. Item replacement refers to a process whereby government statisticians must select and price a different product because the one previously included could not be found. Previous studies have found that some items are replaced more than once a year and annual replacement rates could be as high as 30% for products.

But item replacements are uneven year-to-year and therefore so too is the judgment component of reported inflation. As a result, price changes that are down or up a tenth or a quarter of a percent from year to the next should be considered nothing but statistical noise. But a rule-based inflation-targeting framework will compel policymakers to fiddle with the stance of policy to account for the noise in price measurement.

How is it that policymakers nowadays have fallen in the trap of placing so much importance on a single statistic to conduct monetary policy?

Third, the Fed’s inflation-targeting regime mistakes indirect measures of inflation for direct ones.

A critical aspect of the design of price targeting is the selection of the price series. The price series must be timely and a direct measure of inflation.

The consumer price index (CPI) is the only direct measure of consumer prices. But policymakers have opted to use the personal consumption deflator (PCE). The PCE deflator is not a direct measure of prices since 70% of the prices come from the CPI. The other 30% is based on non-market prices.

Four of the past 5 years, the core CPI has exceeded the 2% target. The only year it missed was 2018 when it was 1.8%. That small undershoot from the 2% target is not statistically significant and certainty not large enough to trigger a change in the stance of monetary policy.

Over the same 5-year period, core PCE ran nearly 75 basis points below the core CPI rate. Almost all of that difference can be explained by the “invisible” prices, or prices for items that are in the PCE but not in CPI.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Does it make sense to base policy decisions on “invisible” prices?

Fourth,inflation targeting lacks balance in anchoring consumer inflation expectations with investor expectations.

The announcement of an inflation target is intended to reduce uncertainty over the future course of inflation and anchor people’s inflation expectations. It is hard to prove that the formal announcement of inflation targeting has had any impact on people’s inflation expectations.

According to the University of Michigan’s consumer sentiment survey, people’s one-year inflation expectations have fluctuated between 2.5% and 3% for the past 20 years, moving above or below the range during an economic crisis or oil shocks. Perhaps people are unaware of the Fed’s 2% inflation target or that “experienced” inflation runs consistently higher than reported inflation.

But investors are readily aware of the Fed’s inflation target. Every little tweak in the Fed’s policy statement on inflation and its impact on official rates triggers almost an instant reaction on the part of investors.

One of the inherent weaknesses of inflation targeting is the inability to balance consumer and investor expectations. That is, as policymakers attempt to simultaneously hit an arbitrary price target and anchor inflation expectations they are inadvertently un-anchoring investor expectations as it eliminates the fear of higher interest rates, encouraging extreme speculation and risk-taking in the financial markets.

Why do policymakers only focus on people’s inflation expectations and not people’s/investor’s asset price expectations as well since both have become unstable at times resulting in bad economic outcomes?

Informal and formal price targeting has been in the Fed’s tool kit for the past 25 years or so. The effects on income and portfolio flows are not similar to conventional monetary policy. At the end of 2019, the market value of equities in people’s portfolios’ stood 3X times workers income, up from 1X times in the mid-1990s.

The shift to inflation averaging compounds the unevenness. That’s because inflation averaging will extend the period of low-interest rates, encouraging more speculation and risk, increasing gains in finance over the economy.

A critical review of the pros and con’s inflation targeting will have to wait for the next crisis. It usually takes three crises before policymakers realize something is fundamentally wrong with their framework.

By then there will be several new academic papers that will highlight the flaws of inflation targeting/averaging, expanding on those that are listed in this article while adding others as well.

After over 40 years researching in the field of economics, with experience on the buy and sell-side of Wall Street, government, and private industry and mostly focusing on financial markets and policy analysis, our long-time friend Joe Carson decided to share his research and opinion on The Carson Report. Please feel free to contact Joe if you have any questions or want to discuss any of his research or opinions.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

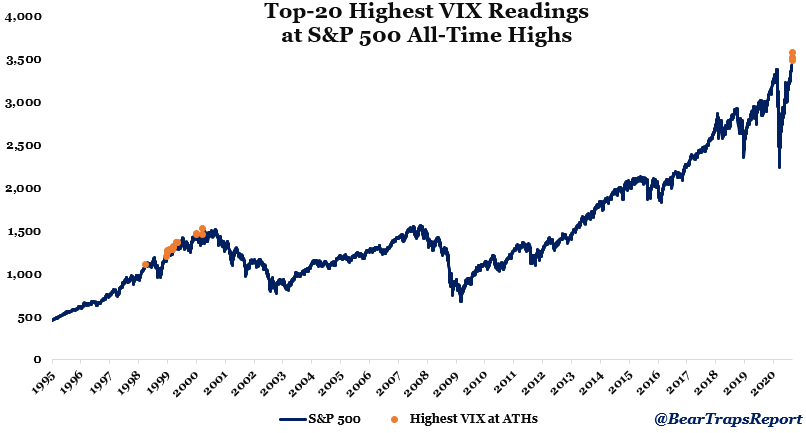

Call it extremely unusual activity. We have a higher stock price in Apple AAPL with a much higher cost of equity upside. Equity vol usually explodes higher in market crashes, NOT bull markets. As you can see above, in normal Apple equity bull markets – see all of 2019 – AAPL implied vol has been CHEAP, NOT RICH (expensive) like today! In March and April, near the market bottom – the price for puts was more than 4x the price for calls, today we have done a 180, extreme fear to extreme greed.

Call it extremely unusual activity. We have a higher stock price in Apple AAPL with a much higher cost of equity upside. Equity vol usually explodes higher in market crashes, NOT bull markets. As you can see above, in normal Apple equity bull markets – see all of 2019 – AAPL implied vol has been CHEAP, NOT RICH (expensive) like today! In March and April, near the market bottom – the price for puts was more than 4x the price for calls, today we have done a 180, extreme fear to extreme greed.  Apple $AAPL is near $140 pre-market on September 2nd. In July, the Street’s 12-month price target was $85, now $116. In March, the price target commanded an $18 PREMIUM to the Apple stock price,

Apple $AAPL is near $140 pre-market on September 2nd. In July, the Street’s 12-month price target was $85, now $116. In March, the price target commanded an $18 PREMIUM to the Apple stock price,  There are a handful of quant funds pushing around a few stocks (with high impact on QQQ, NDX, SPY) in the options markets. The dealers are getting very nervous. Last 15 days – Imaging being a large market maker in Apple and Tesla equity options. You make a market, bid – offer, you get lifted and lifted over and over again by buyers to the point where you have raised the price of calls vs puts to multi-year extremes. How short is the Street gamma? VERY.

There are a handful of quant funds pushing around a few stocks (with high impact on QQQ, NDX, SPY) in the options markets. The dealers are getting very nervous. Last 15 days – Imaging being a large market maker in Apple and Tesla equity options. You make a market, bid – offer, you get lifted and lifted over and over again by buyers to the point where you have raised the price of calls vs puts to multi-year extremes. How short is the Street gamma? VERY.