Join our Larry McDonald on CNBC’s Trading Nation, Wednesday at 3:05pm ET

Pick up our latest report here:

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

*BRAZIL GOVT ALLIES SAID TO SEEK TEMER RESIGNATION: GLOBO

*TEMER UNLIKELY TO FINISH HIS TERM IF ALLEGATIONS TRUE

*TEMER LOST CONDITIONS TO NEGOTIATE PENSION REFORM

*BRAZIL ’21 EUROBONDS SLUMP MOST ON RECORD AMID POLITICAL CRISIS

We spoke to our analysts in Washington overnight – we’re in contact with our relationships on the ground in Brazil. Setting up client calls today:

Brazil Erupts as Tapes Could Ruin Temer Presidency

In Cooperation with Analysts at ACG Analytics

Globo news, an internationally respected Brazilian network and news franchise, is reporting that the Chairman of JBS, the world’s largest meat company, has taped weeks of conversations with President Temer involving pay-offs to prevent imprisoned house speaker Eduardo Cunha from testifying in the Operation Car Wash scandal.

Brazilian equities have surged over the past year as Temer’s administration forged on an ambitious reform program that cheered investors. Brazilians, however, are overwhelmingly opposed to his austerity measures and the president’s approval rating hovers at around 11%.

Equities in Brazil

Up 132% from the January 2016 bottom, stocks in Brazil have priced in a ton of political goodwill. The EWZ is set to open at the $34.20 – $34.50 level, below the two year trend line above in red.

Up 132% from the January 2016 bottom, stocks in Brazil have priced in a ton of political goodwill. The EWZ is set to open at the $34.20 – $34.50 level, below the two year trend line above in red.

We believe the administration’s economic team is highly concerned the crisis will impact their reform agenda. The government has been positioning their long awaited, and very controversial pension reform proposal to the lower house of Congress. Equity prices / valuations are very dependent on completion / passage of these reforms.

Credit Risk Rising

In our view, credit risk will surge focused on Brazil’s government bonds if the reforms collapse.

In our view, credit risk will surge focused on Brazil’s government bonds if the reforms collapse.

Pick up our latest report here:

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereThe JBS CEO Josely Batista reportedly taped Termer ordering the executive to “keep up” the payments in one of the recordings, which are said to be damning throughout.

Several weeks of recordings have reportedly been delivered to the

Attorney General’s office while opposition lawmakers are calling for the president to resign immediately. If this occurs, the Brazilian Constitution requires that elections be held within ninety days.

Dollar – Real Heading North

Technically, the real is moving to far weaker ground – a print above 3.21 shifts the currency into a new bear market.

Per our friends at ACG Analytics, if Temer resigns or otherwise leaves office the Brazilian Constitution requires elections within ninety days. Brazil had been emergencing from it’s worst recession and consensus had been slowly but appreciably growing for Temer’s market based economic reform agenda.

From ACG Analytics in Washington

The corruption crisis in Brazil has left scorched earth where there

were political parties. Initial thoughts include increased attention toward Mariana Silva, a candidate of the left who surged in the 2014 elections but ultimately missed the second round vote. If she is not tainted by scandal, her stock certainly goes up. Brazil’s small but vocal hard right will receive attention as its calls for “cleansing” Brazilian politics through the instatement of military rule could resonate in some quarters.

Pick up our latest report here:

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here This image was produced on May 3rd and included in our Bear Traps Report, 95 target highlighted above with the DXY at 99.08 then.

This image was produced on May 3rd and included in our Bear Traps Report, 95 target highlighted above with the DXY at 99.08 then. The dollar closed at 97.14, breaking a key technical level this week.

The dollar closed at 97.14, breaking a key technical level this week. The Nasdaq 100 is up 18% on the year while the Russell 2000 is only 2% higher. Forget about the noisy headlines, the truth is MORE and more stocks are being left behind in this bull market.

The Nasdaq 100 is up 18% on the year while the Russell 2000 is only 2% higher. Forget about the noisy headlines, the truth is MORE and more stocks are being left behind in this bull market.

Moody’s downgrade of Canada’s biggest banks beat down assets in a market already rattled by woes of mortgage lender Home Capital Group Inc. Yet, very similar to 2007 – most analysts say this isn’t evidence of an impending crisis. Investors are concerned that Home Capital’s troubles can lead to broader financial contagion, tipping Canada’s economy into the kind of crisis it averted in 2008.

Moody’s downgrade of Canada’s biggest banks beat down assets in a market already rattled by woes of mortgage lender Home Capital Group Inc. Yet, very similar to 2007 – most analysts say this isn’t evidence of an impending crisis. Investors are concerned that Home Capital’s troubles can lead to broader financial contagion, tipping Canada’s economy into the kind of crisis it averted in 2008.

This is the beginning of a colossal commodity driven credit collapse. Central bank funded moral hazard gone rogue! May 15th, Noble Group Limited Cut To Caa1 From B2 By Moody’s: “Downgrade reflects heightened concern over Noble’s liquidity stemming from its weak operating cash flow and large debt maturities over the next 12 months, Moody’s says. Moody’s also cites significant uncertainties over an operational turnaround and the high likelihood of debt leverage remaining elevated after company reported 1q loss. Outlook remains negative.”

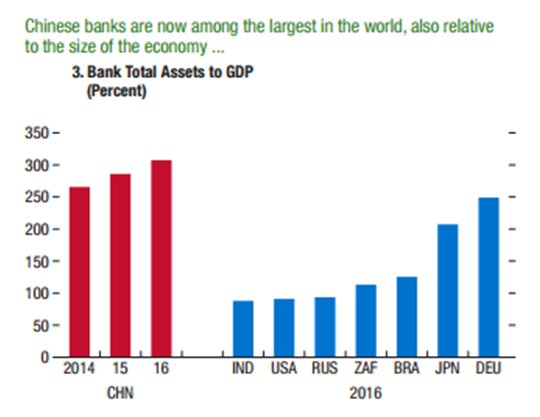

This is the beginning of a colossal commodity driven credit collapse. Central bank funded moral hazard gone rogue! May 15th, Noble Group Limited Cut To Caa1 From B2 By Moody’s: “Downgrade reflects heightened concern over Noble’s liquidity stemming from its weak operating cash flow and large debt maturities over the next 12 months, Moody’s says. Moody’s also cites significant uncertainties over an operational turnaround and the high likelihood of debt leverage remaining elevated after company reported 1q loss. Outlook remains negative.” China’s banking system and underlying economy is far more leveraged than her global peers.

China’s banking system and underlying economy is far more leveraged than her global peers. The insanity of the current global credit profile is on display right here. If you want to buy default protection on the MOST levered economy on the planet earth, its very cheap. This reminds us of Citigroup in 2007, default protection was extremely cheap relative to the underlying credit risk, investors didn’t care. History is repeating itself RIGHT before our very eyes.

The insanity of the current global credit profile is on display right here. If you want to buy default protection on the MOST levered economy on the planet earth, its very cheap. This reminds us of Citigroup in 2007, default protection was extremely cheap relative to the underlying credit risk, investors didn’t care. History is repeating itself RIGHT before our very eyes.

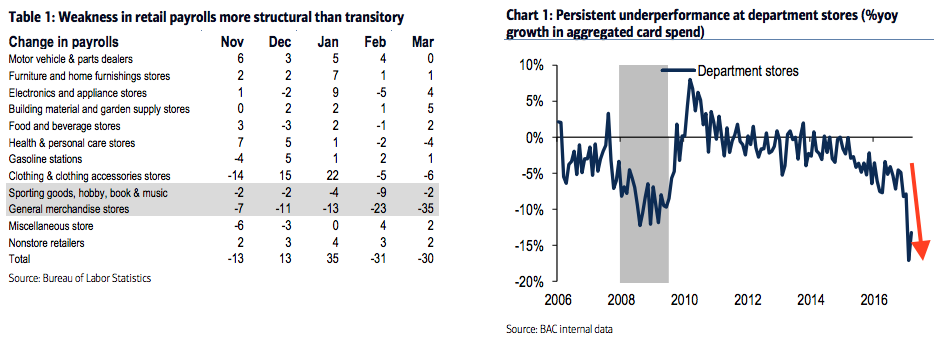

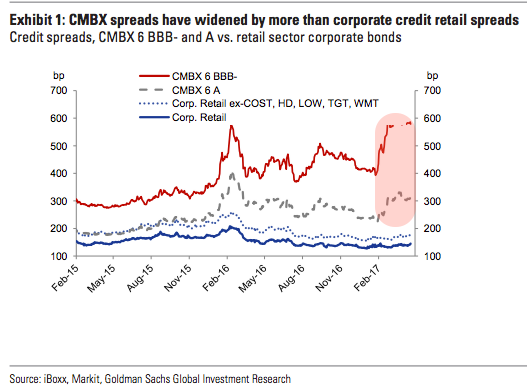

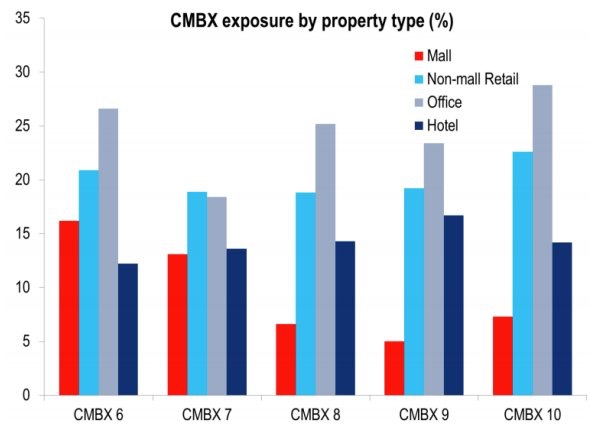

With the U.S. economy at “full employment” and the Federal Reserve hiking interest rates – credit risk is surging. We believe 2017 will be a watershed moment, an acceleration of retail store closures and rent reductions – leading to credit risk contagion. Structured leverage creates asymmetric credit risk as the cycle turns. Retail assets make up over 40% of the debt load inside the CMBX 6 indexes, but only 10% are in the riskiest slices, the regional mall category

With the U.S. economy at “full employment” and the Federal Reserve hiking interest rates – credit risk is surging. We believe 2017 will be a watershed moment, an acceleration of retail store closures and rent reductions – leading to credit risk contagion. Structured leverage creates asymmetric credit risk as the cycle turns. Retail assets make up over 40% of the debt load inside the CMBX 6 indexes, but only 10% are in the riskiest slices, the regional mall category

Shorts have been focused on CMBX6, focused in HIGH mall exposure. In CMBX6 there are sub-indices, each referencing 25 bonds from a portfolio of 25 CMBS offerings issued in 2012. Deals were be selected using rules-based criteria, such as deal size, pricing date, and the applicable rating and credit enhancement of the offered bonds.

Shorts have been focused on CMBX6, focused in HIGH mall exposure. In CMBX6 there are sub-indices, each referencing 25 bonds from a portfolio of 25 CMBS offerings issued in 2012. Deals were be selected using rules-based criteria, such as deal size, pricing date, and the applicable rating and credit enhancement of the offered bonds.