Join our Larry McDonald on CNBC’s Trading Nation, Wednesday at 2pm.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Where are bond yields going with risk of a euro breakup on the rise? Click here (above) for our latest report.

Jobs Recap

Reflation Trade Hype so far Trumped by Secular Dynamics

Since mid December, Utilities (DPG ETF) are up 10%, with a flat S&P 500. The much hyped reflation trade has been put on hold.

Net net, the today’s jobs number was a disaster. In recent years we’ve been lectured about the 15 million jobs created since the financial crisis, but wages are not growing.

The inequality explosion continues, hello Michigan, Pennsylvania and Wisconsin. Middle class America lives on average hourly wages times hours worked. *U6 unemployment is still growing, 9.2% To 9.4%. This begs the question, how much worse would the numbers have been without the unemployment wage increase in 19 states in January?

*This measure of unemployment includes the total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force. Persons marginally attached to the labor force are those who currently are neither working nor looking for work, but indicate that they want and are available for a job and have looked for work sometime in the past 12 months. Persons employed part time for economic reasons are those who want and are available for full-time work but have had to settle for a part-time schedule.

The Missing 4 Million Young People from the Labor Force

We don’t believe Trump wants his legacy wearing a 4.7% start in unemployment, he’s likely to shake up the bureau of labor statistics. There are approximately 4 million people 18-54 years old that are not in the U.S. labor force. On the other hand, at 250k new jobs a month, we’ll chop through that number in 16 months, about the same time the tax cuts and infrastructure spending are actually oozing through the U.S. economy.

– As we expected, the Jan jobs number was topside at 227k vs consensus estimates of 180k but the market is more focused on something else. The real story as was in the soft wages number. AHE only rose by 3 cents of 0.1% month over month, below estimates. We also saw the strong December wage growth number revised lower, with two-tenths downward revision to Dec earnings (now +0.2%). This sums up the reaction in bonds, across the curve there is strength as YoY AHE is is now 2.5% from 2.9% after the Dec report. Chances of a March hike are pretty much gone with this weaker wage number and more dovish statement from the Fed on Wednesday. March hike odds are now around 15%. We think this number puts pressures on the massive short position in bonds.

– The headline number did have strength, but much of it was priced following the ADP number on Wednesday. The market was looking for wages to continue along the lines of the December report, that is where the bonds move is. This was amplified by the fact that minimum wage rose in 19 states during January, which should have lead to a meaningful increase in AHE. But we expected it to be overshadowed by other factors.

– To us, the headline number coupled with slack in wages points to an employment picture that will still confuse the Fed. Wages should have taken the baton from headline NFP by now, if we are really at full employment. We also some of this slack in the massive plunge in “not in the labor force” which dropped 736,000. There were population adjustments in this release, but that is still a big number. The “slack” did not end there, Janet’s favored reading, U6, actually rose 0.2% to 9.4 from 9.2 in December. This jobs picture points to the fact the labor market is not so obviously at full employment. A growing 3 month moving average of 183k a month and slack in wages will push the doves to give the economy more time.

– There were some sectors that offered positives. Retail trade added 45.9k, Service Providing was strong again and manufacturing actually added jobs for the third straight month, a big pull on the headline number seems to be gone.

Join our Larry McDonald on CNBC’s Trading Nation, Wednesday at 2pm.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Where are bond yields going with risk of a euro breakup on the rise? Click here (above) for our latest report.

After all the Brexit horror headlines, UK stocks are up 23% from the June lows.

After all the Brexit horror headlines, UK stocks are up 23% from the June lows.

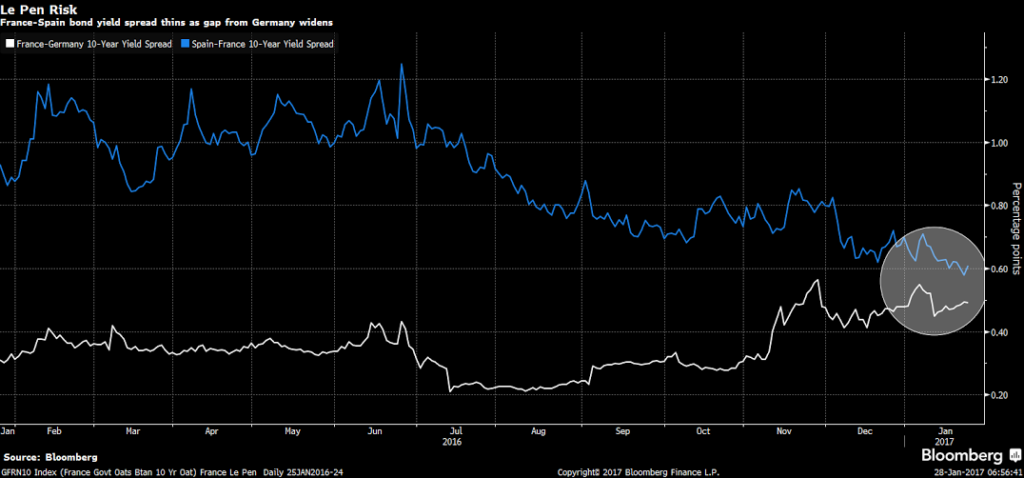

France’s bonds are underperforming peers across the euro area as investors brace for presidential elections, with National Front leader and open euro critic Marine Le Pen leading a major opinion poll for the first round of the vote. The yield on 10-year French securities is the highest relative to Spanish debt since April 2010, while the spread between French and German yields is close to the widest in more than two years. – Bloomberg

France’s bonds are underperforming peers across the euro area as investors brace for presidential elections, with National Front leader and open euro critic Marine Le Pen leading a major opinion poll for the first round of the vote. The yield on 10-year French securities is the highest relative to Spanish debt since April 2010, while the spread between French and German yields is close to the widest in more than two years. – Bloomberg

The index also has a pretty strong correlation with 10 year U.S. treasury yields. We believe, there was a specific section that the market was taken a back by, the “prices received” section. This showed that companies expected to be able to pass on any increase in prices to the consumer, an inflationary sign. This puts a lot pressure on bond prices, has created an opportunity. We’ve rarely seen a trade this crowded, sentiment so one sided.

The index also has a pretty strong correlation with 10 year U.S. treasury yields. We believe, there was a specific section that the market was taken a back by, the “prices received” section. This showed that companies expected to be able to pass on any increase in prices to the consumer, an inflationary sign. This puts a lot pressure on bond prices, has created an opportunity. We’ve rarely seen a trade this crowded, sentiment so one sided.