Our Best Ideas await you, Get on the Bear Traps Report Today, click here

Monday at 8;10am ET: *DIJSSELBLOEM SAYS BANKS ASKING FOR PUBLIC FUNDS ARE PROBLEMATIC

Defaults on the Rise into Lower Yields??

Moody’s Global High Yield Default Rate Takes Out it’s Long Term Average surpasses long-term average in May.

Breaking News: Deutsche Bank Economist Calls for Bailout

Cost of Deutsche Bank Credit Default Protection

There are rising public cries: The banking crisis is in such urgent need that Germany / Europe should violate the current bail-in rules inside the new Banking Directive. Existing bail-in rules are NOT realistic Deutsche Bank maintained publicly this weekend, customer deposits would be at risk and a bank run would be likely. Changing the rules in the middle of the game is the way to go says Deutsche Bank.

Eight years post-Lehman this is so pathetic, when will the establishment ever learn?

(to be continued below at the bottom of this blog)

Thanks to Central Banks, Bonds are Crushing Stocks in 2016

Junk vs S&P 500

Junk Bond ETF $JNK: +6.4% (w 6.1% yield)

S&P 500 $SPY: +4.2% (w 2.1% yield)

Moody’s trailing 12-month global speculative-grade default rate closed at 4.5% in May, surpassing its long-term average of 4.2% for the first time since August 2010, according to its latest global default monitor. Moody’s expects the rate to finish 2016 at 4.9%, and thereafter for upward default rate pressure to ease off.

Our Best Ideas await you, Get on the Bear Traps Report Today, click here

As we stated last year to subscribers, we believe the speculative grade default rate to hit 7% by the end of 2016, with materials and commodity sector bankruptcies leading the way.

Pure Financial Evil

Traditionally insurance companies in Japan and Europe would buy government and investment grade bonds, but today’s $12T of negative yielding government bonds are forcing them to reach for yield in junk bonds.

This week we heard from several sell side trading desks, we’re told negative interest rate torn insurance companies in Europe and Japan now piling into U.S. high yield paper.

After you implement the change in capital standards yields are basically at record lows. This has become an evil, or perverse incentive for insurers to chase yield at the lower end of the rating spectrum.

Our Best Ideas await you, Get on the Bear Traps Report Today, click here

Cost of Credit Default Protection

The cost of credit default protection on some European banks is certainly on the rise. Above CDS on subordinated financials, Deutsche Bank and UniCredit are shouting, WARNING.

Our Best Ideas await you, Get on the Bear Traps Report Today, click here

Credit vs Equities, What are they Telling Us?

When you look at equity prices of Intesa Sanpaolo, Deutsche Bank and UniCredit, we’re talking lows we have not seen since 2012.

Next, contrast with the relationship of subordinated credit default swaps on these banks vs the subordinated financials credit index.

Back in 2012, subordinated cds traded 310bps wide of subordinated financials index, while today only 230ish wide. We believe the new bailout regime is a game changer, it speaks to evaporation risk to subordinated debt.

Stock Prices of European Banks

Taking a look at a banks capital structure is even more important in today’s bail-in regime world.

Breaking News: Deutsche Bank Economist Calls for Bailout

“In Europe, the bailout does not need to be so large. A €150 billion program should be enough to help European banks recapitalize,”

“Europe is seriously ill and needs to address very quickly the existing problems, or face an accident,”

David Folkerts-Landau, Deutsche Bank Chief Economist, July 10, 2016

Banks in Europe should get the money for recapitalization following a similar bail out in the U.S., Deutsche Bank Chief Economist David Folkerts-Landau, tells Welt am Sonntag in interview.

Deutsche Bank pointed to the plunge in bank stocks is only the symptom of a larger problem, negative interest rates impact on bank’s profitability, slow growth and “dangerous” deflation.

- U.S. helped its banks with $475 billion, and such a program needed in Europe, especially for Italian lenders

- Est. EU40b money needed by Italian banks “conservative”

- Bail-in using private money currently not doable, would hit people’s savings, may cause bank run

- Decline in bank stocks symptom of weak growth, high govt debt and close to “dangerous” deflation

- Europe “extremely sick” and must solve its problems quickly

Bloomberg

Folkerts- Landau is very concerned about Italy and the condition of local banks, the $45B number floated about if far too “conservative.”

A look at our best trading ideas for the second half of 2016, click here below:

Our Best Ideas await you, Get on the Bear Traps Report Today, click here

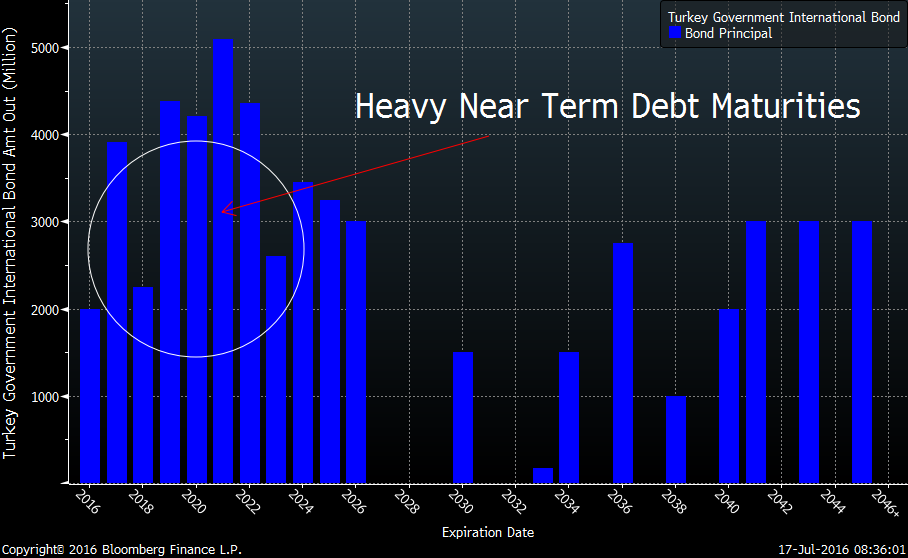

Turkey is quickly moving from a rates story to a credit story. Investors are no longer betting on rate cuts, they’re far more worried about credit risk. Pick up our latest trade ideas and report on geopolitical risk management here:

Turkey is quickly moving from a rates story to a credit story. Investors are no longer betting on rate cuts, they’re far more worried about credit risk. Pick up our latest trade ideas and report on geopolitical risk management here:

Nearly $60B of total government debt, but near term maturities are on the heavy side for Turkey.

Nearly $60B of total government debt, but near term maturities are on the heavy side for Turkey.

Turkey’s 5 Year CDS made a strange reversal this morning, then closed for the day.

Turkey’s 5 Year CDS made a strange reversal this morning, then closed for the day.