Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

This morning WeWork junk bonds touched a 13% yield, earlier this year the brain trusts on Wall St. talked up a possible $60B valuation. Then, SoftBank purchased private shares, completed in connection with a $5B primary investment into WeWork that valued the company at $47B, more than double its previous valuation, according to Pitchbook. Today, the equity is near worthless, oh how quickly sentiment can change. That’s the problem with leverage – when equity stands behind a colossal pile of debt, it can evaporate far faster than most realize. SoftBank better pull-out the checkbook, $10B of fresh cash is needed. In our view, WeWork has the capacity to issue a little more than $1B in secured debt and $2.56B of unsecured debt. This is substantially less than some of the estimates floating out there regarding potential loan commitments., working with Xtract Research on the numbers. Above all, we must think about the follow-on side effects in today’s equity market. These events are harbingers of things to come in our view. A meaningful re-pricing is in the works.

“If the company is unable to raise new financing before the end of November, the people said it could face something that executives within WeWork never thought was an option just weeks ago: bankruptcy.” – FT

Central Banks Funding Fraud?

We must ask ourselves. After wide-open capital markets, an endless gravy train of nearly free cash, are the side effects in venture capital playing out? How can WeWork eviscerate $50B of equity value in less than six months? What are the follow-on implications? Postmates, Lyft, DoorDash, WeWork, Peloton, Uber, and Casper will lose nearly $15B this year. A near-endless supply of cash is needed to fund many of these businesses. The financial media’s story of the year is WeWork’s implosion. The larger narrative will be found in SoftBank’s Vision Funds impairment – if the market isn’t there for them, they will have to fill the capital hole.

A Wave of Sellers

The restricted shares from the respective IPOs of Zoom Communications (ZM) and Pinterest (PINS) were ‘unlocked’ on Tuesday. Both stocks are lower despite over a 1% rally in the S&P 500. ZM is down -2.6% while PINS is down -4.4%, both are on-track for their largest volume days in months. In our view, this shows across the IPO space, there is a herd of restricted-shares just waiting to sell. See below for the restricted share expiration schedule…

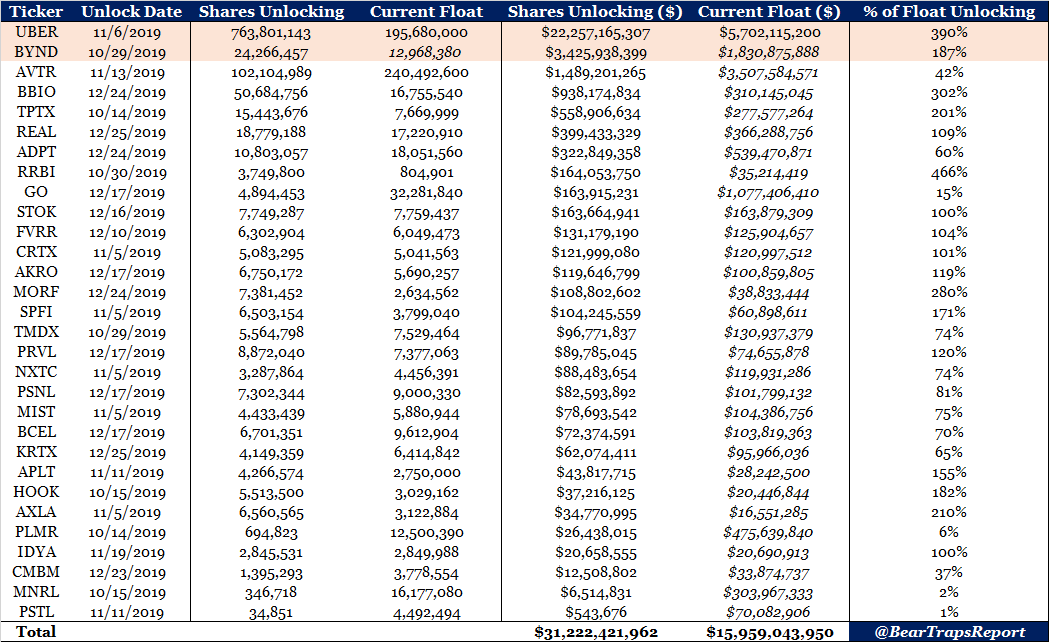

The IPO Unlock Graph

Out of the $31.2B of restricted IPO shares becoming unlocked from now until the end of the year UBER is 71% of the total. ($22B vs. $31B). However, what is very interesting is the amount unlocking relative to the current float…While most unlock packages are smaller than the current float or near a 1:1 ratio, UBER’s is 4x the size! UBER float is currently 195M shares and worth $7.4B. Meanwhile, 764M shares worth $22.3B of UBER are unlocking on November 6th… That means up to 424% of the current float could be for sale.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

WeWork Contagion and a Lyft Benefit:

Given what just happened to WeWork and the performance of LYFT and UBER IPOs, you have to think a large portion of the $22B unlocking wants out… Meanwhile, some clients are thinking this will be a positive for Lyft, as the company was used as a hedge for restricted shareholders…

UBER Currently has a $49B Valuation

The series G funding round was at a $68B valuation in 2016, (FortRoss Ventures, Saudi Arabia’s Public Investment Fund). In August 2018, Toyota Motor Company came in with a $500M investment at a $76B valuation… Last man on the deal team?

Lyft Restricted-Shares Unlock

Notably, Lyft is down -42% since they announced the early unlocking of their restricted shares. Although the increase in float does not directly influence the valuation, it does bring a herd of likely-sellers.

Since August 15th

LYFT -26%

UBER -5%

*IPO Lock-Up Impact… Bloomberg data

Zero Sum Game

Ridesharing companies LYFT, and UBER don’t have a moat in our view. It’s like “Chinese capitalism” (that funnels lots of profits to consumers, thus poor performance in the company’s stock prices). It’s a subsidy of consumers (Uber riders) at the expense of Uber shareholders and Uber Drivers.

Ridesharing companies LYFT, and UBER don’t have a moat in our view. It’s like “Chinese capitalism” (that funnels lots of profits to consumers, thus poor performance in the company’s stock prices). It’s a subsidy of consumers (Uber riders) at the expense of Uber shareholders and Uber Drivers.

IPOs Shelved

Endeavor Group Holdings

Poshmark

WeWork*

In Limbo

Palantir Technologies

Postmates

McAfee

Drawdowns from IPO

Lift -53%

Slack -49%

Smile Direct -43%

Uber -36%

Peloton -18%

*Equity valuation drawdown near 80%.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here