Institutional investors can join our live chat on Bloomberg, a groundbreaking venue since 2010 – now with clients in 20+ countries, just email tatiana@thebeartrapsreport.com – Thank you.

Author Lawrence McDonald is the New York Times Bestselling Author of “A Colossal Failure of Common Sense” – The Lehman Brothers Inside Story – one of the best-selling business books in the world, now published in 12 languages – ranked a top 20 all-time at the CFA Institute.

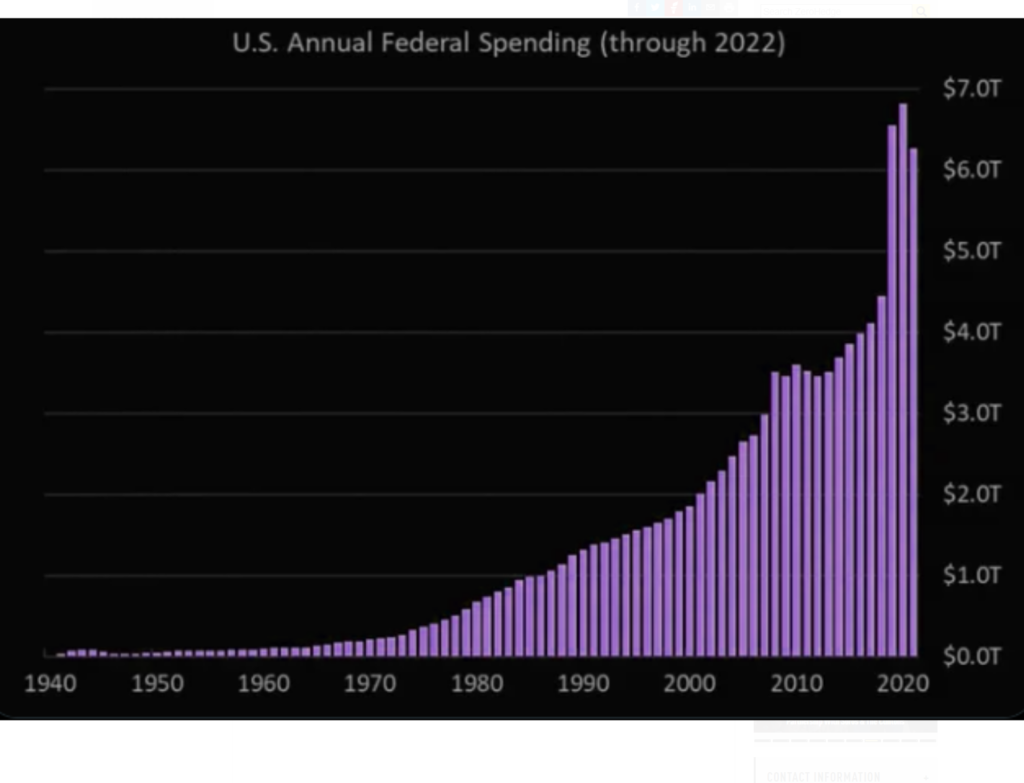

The Mind-Blowing Hole

After dinner drinks, a friend said these blood-curdling words;

“The US government has already spent $5.3 TRILLION this year. We are on track for the 4th consecutive year with $6 trillion or more in government spending. Since 2020, the US government has spent a jaw-dropping $25 TRILLION. To put this in perspective, the market cap of the S&P 500 is $37 trillion. Spending since 2020 is equivalent to 68% of the entire S&P 500 market cap.”

“The US government has already spent $5.3 TRILLION this year. We are on track for the 4th consecutive year with $6 trillion or more in government spending. Since 2020, the US government has spent a jaw-dropping $25 TRILLION. To put this in perspective, the market cap of the S&P 500 is $37 trillion. Spending since 2020 is equivalent to 68% of the entire S&P 500 market cap.”

Walking away from ultra-low rates and Quantitative Easing isn’t so easy given the massive public debts from the governments Central Banks work for. It is universally agreed that debt levels are too high. The question is: How can those debt levels be reduced?

This problem has become particularly acute after the pandemic lockdowns. At 2020-year end, the US had a debt to GDP of 127% which looks conservative next to Japan’s 256% but certainly more aggressive than the EU’s 100%. Given various fiscal measures, these ratios don’t look to be improving any time soon. In this environment, higher interest rates threaten financial stability. High government debt limits Fed options. Volcker was aggressive in part because debt levels were relatively muted compared to today. Debt to GDP in 1979 was a mere 34%. Volcker raised rates sharply and increased reserve requirements for banks, causing a recession stabilizing the dollar, and reducing inflation. It should be noted that deregulation led the way out of recession. Since then, various crises have been met with aggressive lowering of rates, as we all know. The consensus view among Central Banks has been that they cannot identify bubbles, but they can fix markets once those bubbles pop.

One way to reduce debt is through austerity. As an example, after WWI Italy was burdened with a debt to GDP ratio of 180%. In response, government spending was severely cut back and consumption on expenditures increased. As a result of continuous surpluses, the Italian lira stabilized as debt to GDP declined to 76%. Another example was Germany after unification. Public spending fell, future social benefits were cut. Growth declined but the current account balance went into surplus. It took nearly 20 years, but growth came back. As the economy finally grew, so did tax revenues. There followed investment in Southern and Eastern Europe. Another example was the EU after the Great Financial Crisis. Since EU membership precluded countries from individually depreciating their currencies, government expenditures were reduced. Nominal wages declined in many countries. However, debt to GDP levels didn’t improve, so the ECB loosened credit conditions. For Germany, this caused a real estate and export boom. As a result, debt to GDP levels declined.

Another way to improve debt to GDP ratios is through hidden debt reduction i.e. inflation. It is an old truism that inflation is a tax, and that raising taxes outright is considered an unpalatable risk politically. Higher inflation does reduce the real value of tax revenues. Financial repression means to keep the return to savers below the inflation rate. This is what the US and the UK did after WWII. The UK public debt to GDP was 250% after WWII. In the US, it was 120%. Not only were low interest rates pursued but interest on savings were capped. Various regulations were put in place the effect of which was to direct credit to government. The forced low-interest rate on government bonds reduced debt in two ways. With low-interest rates, compounding was held at least somewhat in check. Additionally, low to negative interest rates devalued the debt that already existed. However, when these techniques were used in emerging economies to protect non-competitive industries, debt to GDP ratios did not improve. Recent history in the US, UK and EU suggests that financial repression has been used with increasing similarity to emerging economies.

Another example of hidden debt reduction is hyperinflation as in Germany after WWI. While a slow-but-steady financial repression gradually transfers wealth from creditors to debtors, hyperinflation does the same thing but very quickly. Workers respond by demanding higher wages, and the increase in money demand is met with an increase in money supply. Germany’s hyperinflation of 1923 was caused by excessive money growth to fund the prior war’s expenses. The transfer of gold from Germany to its enemies didn’t help matters. To offset the negative economic and monetary consequences of the Treaty of Versailles, the Reichsbank extended credit to the German government. Eventually, the German government stopped paying reparations in 1923 causing France and Belgium to occupy Germany’s industrial heartland. That didn’t help matters. The German economy collapsed. The government asked workers to go on strike and compensated them with their normal wages by printing money. Hyperinflation ensued.

Argentina, a country people like lending to at par in order to lose money in the most predictable way possible, followed a not dissimilar path in the 1970s. The twist was that much of the capital used to finance its inflation came from overseas and was denominated in a foreign currency: the US dollar. Local debt is not indexed to inflation, and so is devalued through inflation. The central bank would accumulated government bonds, financed by monetary expansion, which fuels inflation. As inflation rose, so too did nominal GDP thereby reducing the debt to GDP ratio. However, when most of your debt is in USD and the dollar appreciates against the peso, default ensues. Eventually, by 2020 over three-quarters of Argentina’s debt was in foreign denominations, roughly $250 billion of it. Argentina has defaulted five times since the 1980s. The government usually expands the money supply in order to buy bonds: financial repression. This causes inflation and lowers the value of public debt. Furthermore, by lowering the currency exchange rate, prices for imported goods increase. Eventually, the market demanded bonds indexed to inflation if they were in local currency. Another Argentinian government tactic was to exchange its foreign reserve holdings with non-transferable dollar-denominated Argentinian Government obligations. However, instead of paying them off at maturity, the government just rolled it over into new debt. In other words, one method of financial repression was theft. The stolen lucre was spent and that exacerbated inflation. Interest rates were held artificially low, and defaults were delayed a year or two. Capital controls and monetary sterilization techniques are employed as well, with inflationary consequences. Ultimately, however, the easiest way to lower debt to GDP is to default, restructure/exchange liabilities for lower nominal amounts, and thus lower debt. Argentina defaults on a regular basis because it is basic to its debt management practice. Ultimately, then, hidden debt reduction becomes unveiled debt reduction.

Besides austerity and severe inflation, there is a third route to improving debt to GDP ratios: extreme economic and currency reform. The classic example was Germany after WWII. No one worked for money, it was worthless. Barter was common. Since debt to GDP was almost 250% of GDP, the fork in the road to lower debt to GDP and thus to bring value to money and a return of money exchange purchase transactions couldn’t be the hyperinflation of the Weimar Republic, which, after all, was an experience that all Germans remembered. Hence currency reform was implemented. Excess liquidity was drained by a reduction in the money supply. Because Germany was occupied militarily, that perforce led to a change in the country’s economic structure. A currency reform combined with a reduction in money is effectively at least a partial default. Once a new currency is introduced at some ratio vs the old currency, the entire economy is changed. To make the velocity of money return to normal, the supply of money had to be reduced by 90%. The architects of reform had all liabilities to the former government and the Nazi party annulled for political reasons. Deutsche Mark debts were reduced by 90%. Those who benefited from the currency and debt reform were taxed at 100%, payable in installments. The remaining assets were taxed at 50%, paid in installments. This redistributed wealth. A liberal market economy was introduced, replacing the planned economy. The path forward resulted in Germany becoming a major global economic powerhouse.

Going forward, one may imagine a fourth way of reducing debt to GDP via inflation would be a digital currency, which might be particularly appealing for the ECB since there is no common fisc backing the currency. Euro money supply would be increased by the ECB purchasing ECB bonds. The money supply would be nominally guided by the expected growth of the Euro area. Money supply would be increased by government purchases of debt, not by loan origination from the banks. The banks themselves would be reduced to interest rate arbitrageurs, effectively. The system would take bond out of the system since they would be owned by the ECB. The ECB could double its inventory of bonds, to EUR 6 trillion and could even suspend payments to its own inventory and/or coupons could be changed to zero. Any kind of large-scale reform, where the more conservative northern countries would take a hit for the benefit for the heavily indebted southern countries in exchange for promises that the southern countries would behave going forward. In other words: digitization of the Euro currency could be accompanied by increased influence of the ECB, decreased influence of the traditional banking system, and realignment of debt levels punishing the well-behaved in exchange for a verbal promise from the perpetually profligate. It would fail ultimately, of course, but not immediately. Bottom line: a EUR digital currency will be more camouflage than substance.

From the above one may easily conclude that the long period of super low rates in developed economies have created excesses and fragilities that cannot rebalance debt to GDP without measures that would be felt as catastrophic to its citizens in its immediate effects. Central banks are driven by events. Central banks don’t pre-empt events. Therefore, we find it hard to believe that financial repression will be avoided until a crisis leaves them no choice. Between now and then there is one clear path: inflation.

“The Federal Reserve may not be that bright, but they are not so stupid as to replicate the Weimar Republic’s hyperinflationary monetary policy. They want to slow-walk financial repression, keeping government interest expense below the rate of inflation by a modest yet significant degree which means keeping what savers can earn lending to the US government below the rate of inflation. This isn’t being done as in some emerging economies as part of a plan to protect inefficient industries. It is being done by the largest economy and greatest military power the world has ever seen, by the country that has the dominant and deepest financial markets, that can be chipped away a bit but not rejected out of hand. You can’t pretend the USA doesn’t exist. What the US does ends up being copied by the rest of the planet. The US government’s financial repression is a back door way of lowering government debt thereby improving the debt-to-GDP ratio to a sustainable level. Politicians are loath to outright raise taxes on the middle class, so they tax everybody via inflation. The Fed doesn’t want inflation to go away. It wants inflation to stay above the US government’s average interest rate expense. The secondary, but vital concern, is to do that without causing hyperinflation. Hence the slow walk. It’s a 15-year program, not a 15-month program. It is no accident the Fed pauses with Fed Funds matching the inflation rate. The Fed spends more time looking at Treasury’s blended average interest rate vs the inflation rate than at the inflation rate itself in isolation.”