“Our indicators tell us, we’re very close to a Lehman-like drawdown,” argues Larry McDonald, a former strategist at Société Générale who now runs The Bear Traps report.

Financial Times, February 20, 2020

*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereIf you’ve never read this classic, the Stan Druckenmiller speech delivered in 2015 at the Lost Tree Club, in Florida – you’re in for a treat. It’s so inspiring – Druck’s passion for markets is like no other. Putting the pieces to the puzzle together means everything to him and everything to us. Above all, today – the words on this page carry a lot more weight. Blow by blow Stan lived and traded through a market much like the 2020 bull run in U.S. equities. Tech stocks in 1998-1999 and 2019-2020 are more like brothers than cousins in our view – we must sit back and embrace the lessons of the past. Make sure you read about the “gun-slingers” (below).

Stan Druckenmiller and Ken Langone

SD:

I thought I would spend a moment just reflecting on

why I believe my record was what it was, and maybe

you can draw something from that. But the first

thing I’d say very clearly, I’m no genius. I was not

in the top 10 percent of my high school class. My

SATs were so mediocre I went to Bowdoin because it

was the only good school that didn‘t require SATs,

and it turned out to be a very fortunate event for

me.

But I’d list a number of reasons why I think I had

the record I did because maybe you can draw on it in

some of your own investing or also maybe in picking a

money manager. Number one, I had an incredible

passion, and still do, for the business. The thought

that every event in the world affects some security

price somewhere I just found incredibly

intellectually fascinating to try and figure out what

the next puzzle was and what was going to move what.

And the fact that I could bet on that interaction,

those who know me, I do like to bet. One of the

great things of this business, I get to gamble for a

living and channel it through the markets instead of

illegal activity. That was just sort of nirvana for

me that I could constantly be making these bets,

watch the market moving, and get my grades in the

newspaper every day.

The second thing I would say is I had two great mentors. One I stumbled upon and one I sought out.

And I see some young people in the audience and

probably some grandparents who have some influence on some young people in the audience, and I would just

say this. If you’re early on in your career and they

give you a choice between a great mentor or higher

pay, take the mentor every time. It’s not even

close. And don‘t even think about leaving that

mentor until your learning curve peaks. There’s just

nothing to me so invaluable in my business, but in

many businesses, as great mentors. And a lot of kids

are just too short-sighted in terms of going for the

short-term money instead of preparing themselves for

the longer term.

—–

“If you’re early on in your career and they give you a choice between a great mentor or higher pay, take the mentor every time.”

Stan Druckenmiller

—-

The third thing I’d say is I developed partly through

dumb luck ~ I’ll get into that — a very unique risk

management system. The first thing I heard when I

got in the business, not from my mentor, was bulls

make money, bears make money, and pigs get

slaughtered. I’m here to tell you I was a pig. And

I strongly believe the only way to make long-term

returns in our business that are superior is by being

a pig. I think diversification and all the stuff

they’re teaching at business school today is probably

the most misguided concept everywhere.

And if you look at all the great investors that are

as different as Warren Buffett, Carl Icahn, Ken

Langone, they tend to be very, very concentrated

bets. They see something, they bet it, and they bet

the ranch on it. And that’s kind of the way my

philosophy evolved, which was if you see – only maybe

one or two times a year do you see something that

really, really excites you. And if you look at what

excites you and then you look down the road, your

record on those particular transactions is far

superior to everything else, but the mistake I’d say

98 percent of money managers and individuals make is

they feel like they got to be playing in a bunch of

stuff. And if you really see it, put all your eggs

in one basket and then watch the basket very

carefully.

Now, I told you it was kind of dumb luck how I fell

into this. Ken Langone knows my first mentor very

well. He’s not a well-known guy, but he was

absolutely brilliant, and I would say a bit of a

maverick. He was at Pittsburgh National bank. I

started there when I was 23 years old. I was in a

research department. There were eight of us. I was

the only one without an MBA, and I was the only one

under 32 years of age. I was 23 years old.

After about a year and a half – I was a banking and a

chemical analyst – this guy calls me into his office

and announces he’s going to make me the director of

research, and these other eight guys and my

52-year-old boss are going to report to me. So, I

started to think I’m pretty good stuff here. But he

instantly said, “Now, do you know why I’m doing

this?” I said no. He says, “Because for the same

reason they send 18-year-olds to war. You’re too

dumb, too young, and too inexperienced not to know to

charge. We around here have been in a bear market

since 1968.” This was 1978. “I think a big secular

bull market’s coming. We’ve all got scars. We’re

not going to be able to pull the trigger. So, I need

a young, inexperienced guy. But I think you‘ve got

the magic to go in there and lead the charge.” So, I

told you he was a maverick, and as you can already

see, he’s a little bit eccentric. After he put me in

there, he was gone in three months. I’ll get to that

in a minute.

But before he left, he taught me two things. A,

never, ever invest in the present. It doesn’t matter

what a company’s earning, what they have earned. He

taught me that you have to visualize the situation 18

months from now, and whatever that is, that’s where

the price will be, not where it is today. And too

many people tend to look at the present, oh this is a

great company, they’ve done this or this central bank

is doing all the right things. But you have to look

to the future. If you invest in the present, you’re

going to get run over!

—-

“Profits are achieved by discounting the obvious, and placing capital in the direction of the unexpected.”

George Soros

—-

The other thing he taught me is earnings don’t move

the overall market; it’s the Federal Reserve Board.

And whatever I do, focus on the central banks and

focus on the movement of liquidity, that most people

in the market are looking for earnings and

conventional measures. It’s liquidity that moves

markets.

Now, I told you he left three months later, and

here’s where the dumb luck came in in terms of my

investment philosophy. So, right after he leaves,

the Shah of Iran goes under. So, oil looks like it’s

going to go up 300 percent. I’m 26 — 25, excuse me.

I don’t have any experience. I don’t know anything

about portfolio managers. So, I go well, this is

easy. Let’s put 70 percent of our money in oil

stocks and let’s put 30 percent in defense stocks and

let’s sell all our bonds. So, and I would have

agreed with him if I had some experience and I was a

little more experienced, but the portfolio managers

that were competing with me for the top job, they, of

course, thought it was crazy. I would have thought

it was crazy too if I’d have had any experience, but

the list I proposed went up 100 percent. The S&P was

flat. And then at 26 years old they made me chief

investment officer of the whole place. So, the

reason I say there was a lot of luck involved is

because as Drelles predicted, it was my youth and it

was my inexperience, and I was ready to charge.

So, the next thing that happened when I started at

Duquesne, Ronald Reagan had become President, and we had a radical man named Paul Volcker running the

Federal Reserve. And inflation was 12 percent. The

whole world thought it was going to go through the

roof, and Paul Volcker had other ideas. And he had

raised interest rates to 18 percent on the short end,

and I could see that there is no way this man was

going to let inflation go. So, I had just started at

Duquesne. I had a small amount of new capital. I

took 50 percent of the capital and put it into

30—year treasury bonds yielding 14 percent, and I

owned nothing else. Sort of like the oil and defense

story, but now we’re on a different gig. And sure

enough, the bonds went up despite a bear market in

equities. Right out of the chute I was able to be up

40 percent. And more importantly, it sort of shaped

my philosophy again of you don’t need like 15 stocks

or this currency or that. If you see it, you got to

go for it because that’s a better bet than 90 percent

of the other stuff you would add onto it.

So, after that happened, my second mentor was George

Soros, and unlike Speros Drelles, I imagine most of

you have heard of George Soros. And had I known

George Soros when I made the bond bet, I probably

would have made a lot more money because I wouldn’t

have put 50 percent in the bonds, I probably would

have put about 150 percent in the bonds. So, how did

I meet George Soros? By the early to mid-‘BOs

commodities were having dramatic moves. currencies

were having big moves, bonds were having big moves,

and I was developing a philosophy that if I can look

at all these different buckets and I‘m going to make

concentrated bets, I’d rather have a menu of assets

to choose from to make my big bets and particularly

since a lot of these assets go up when equities go

down, and that’s how it was moving.

And then I read The Alchemy of Finance because I’d

heard about this guy, Soros. And when I read The

Alchemy of Finance, I understood very quickly that he

was already employing an advanced version of the

philosophy I was developing in my fund. So, when I

went over to work for George, my idea was I was going

to get my PhD in macro portfolio manager and then

leave in a couple of years or get fired like the nine

predecessors had. But it’s funny because I went over

there, I thought what I would learn would be like –

what makes the yen goes up, what makes the deutsche

mark move, what makes this, and to my really big

surprise, I was as proficient as he was, maybe more

so, in predicting trends.

That’s not what I learned from George Soros, but I

learned something incredibly valuable, and that is

when you see it, to bet big. So what I had told you

was already evolving, he totally cemented. I know we

got a bunch of golfers in the room tonight. For those who

follow baseball, I had a higher batting average;

Sores had a much bigger slugging percentage. When I

took over Quantum, I was running Quantum and

Duquesne. He was running his personal account, which

was about the size of an institution back then, by

the way, and he was focusing 90 percent of his time

on philanthropy and not really working day to day.

In fact a lot of the time he wasn’t even around.

And I’d say 90 percent of the ideas he were [ph.]

using came from me, and it was very insightful and

I’m a competitive person, frankly embarrassing, that

in his personal account working about 10 percent of

the time he continued to beat Duquesne and Quantum

while I was managing the money. And again it’s

because he was taking my ideas and he just had more

guts. He was betting more money with my ideas than I

was.

Probably nothing explains our relationship and what

I’ve learned from him more than the British pound.

So, in 1992 in August of that year my housing analyst

in Britain called me up and basically said that

Britain looked like they were going into a recession

because the interest rate increases they were

experiencing were causing a downturn in housing. At

the same time, if you remember, Germany. the wall had

fallen in ’89 and they had reunited with East

Germany, and because they’d had this disastrous

experience with inflation back in the ’30s, they were

obsessed when the Deutsche mark and the [unint.]

combined, that they would not have another

inflationary experience. So, the Bundesbank, which

was getting growth from the [unint.] and had a

history of worrying about inflation was raising

rates like crazy. That all sounds normal except the

deutsche mark and the British pound were linked. And

you cannot have two currencies where one economic

outlook is going like this way and the other outlook

is going that way. So, in August of ’92 there was 7

billion in Quantum.

I put a billion and a half, short the British pound…

…based on the thesis I just gave you. So,

fast-forward September, next month. I wake up one

morning and the head of the Bundesbank, Helmut

Schlesinger, has given an editorial in the Financial

Times, and I’ll skip all the flowers. It basically

said the British pound is crap and we don’t want to

be united with this currency. So, I thought well,

this is my opportunity. So, I decided I’m going to

bet like Soros bets on the British pound against the

deutsche mark.

It just so happens he’s in the office. He’s usually

in Eastern Europe at this time doing his thing. So,

I go in at 4:00 and I said, “George, I’m going to

sell $5.5 billion worth of British pounds tonight and

buy deutsche marks. Here’s why I’m doing it, that

means we‘ll have 100 percent of the fund in this one

trade.” And as I’m talking, he starts wincing like

what is wrong with this kid, and I think he’s about

to blow away my thesis and he says, “That is the most

ridiculous use of money management I ever heard.

What you described is an incredible one-way bet. We

should have 200 percent of our net worth in this

trade, not 100 percent. Do you know how often

something like this comes around? Like one or 20

years. What is wrong with you?” So, we started

shorting the British pound that night. We didn‘t get

the whole 15 billion on, but we got enough that I’m

sure some people in the room have read about it in

the financial press.

—–

Every bet when it’s put on has a risk – reward formula. There are some bets where if you risk x you and make y, and others (one-way) if you risk x, you can make x,y and z. The most attractive wager of all is the “one-way” bet, the supreme-optimal risk vs. reward.

—-

So, that’s probably enough old war stories tonight.

I love telling old war stories because I like to

reminisce when I was a money manager and doing better

returns than I have since I retired, but I do think

it’s important maybe let’s try and move me to the

present here a little bit. So, I told you that one

of the things I learned from Drelles was to focus on

central banks. And Sam was kind enough to point out

some very good returns we had over the years.

One of the things I would say is about 80 percent of

the big, big money we made was in bear markets and

equities because crazy (Dislocations in markets) things were going on in response to what I would call central bank mistakes during that 30-year period. And probably in my mind the poster child for a central bank mistake was actually the U.S. Federal Reserve in 2003 and 2004.

I recall very vividly at the end of the fourth

quarter of 2003 calling my staff in because interest

rates, fed funds were one percent. The nominal

growth in the U.S. that quarter had been nine

percent. All our economic charts were going through

the roof, and not only did they have rates at one

percent, they had this considerable period — sound

familiar? — language that they were going to be there

for a considerable time period (forward guidance).

So, I said I want you guys to try and block out where

fed funds are and just consider this economic data

and let’s play a game. We’ve all come down from

Mars. Where do you think fed funds would be if you

just saw this data and didn’t know where they were?

And I‘d say of the seven people the lowest guess was

3 percent and the highest was 6 percent. So, we had

great conviction that the Federal Reserve was making

a mistake with way too loose monetary policy. We

didn‘t know how it was going to manifest itself, but

we were on alert that this is going to and very

badly.

Sure enough, about a year and a half later an analyst

from Bear Stearns came in and showed me some subprime situation, the whole housing thing, and we were ableto figure out by mid-’05 that this thing was going to end in a spectacular housing bust, which had been engineered – or not engineered but engendered by the

Federal Reserve’s too-loose monetary policy and end

in a deflationary event. And we were lucky enough

that it turned out to be correct. My returns weren‘t

very good in ’06 because I was a little early, but

’07 and ’08 were – they were a lot of fun.

So. that’s why if you look at today — can we get the

charts up please? I’m experiencing a very strong

sense of deja vu. Let’s just play the game I played

with my analysts back in 2003, 2004 and go through a

series of charts. So, this is the United States

households’ net worth per household. And it’s

textbook. You see the big drop in the financial

crisis. It’s textbook when you have consumer balance

sheets torn to pieces by a financial crisis to use

super-loose monetary policy to rebuild those balance

sheets, which the Federal Reserve did beautifully.

What’s interesting though is if you look forward by

2011, we had already exceeded the ’07 levels, which I

think a lot of people would agree was already an

overheated [ph.] period, and since then we’ve gone

straight up for two more years, and household net

worth is certainly in very, very good shape.

Here’s employment. As you can see after another big

problem after the financial crisis, the employment

market has largely healed, and we’re down at 5.6 on

the unemployment rate. Here’s industrial production.

Again, big drop after ’07. Look at this thing. It’s

screaming. Here’s retail sales. Again you see the

damage, but you see where we are now. You’re right

on a 60-year uptrend, which is actually very good.

And then I’m sure for those of you who are

unfortunate enough to watch CNBC and read other

financial statements, you’ll know that the fed is

absolutely obsessed with Japan. They’ve been talking

about this Japan analogy for 10 or 15 years now or

certainly since Bernanke took over. And let me just

show you something. This is the core CPI in the U.S.

I‘m sure you’ve heard the word “deflation” more than

you’d like to hear it in the last three or four

years. We’ve never had deflation. Our CPI has gone

up 40 percent over this time with not one period of

deflation. And at the bottom you see Japan, which is

down 15 percent. I did think there was a case, a

viable case in ’09, ’10 that we may follow Japan.

But you know what, I’ve thought a lot of things when

I’m managing money with great, great conviction, and

a lot of times I’m wrong. And when you’re betting

the ranch and the circumstances change, you have to

change, and that’s how I’ve always managed money.

But the feds‘ thesis to me has been proved dead wrong

about three or four years ago, which is okay, but

there was no pivot.

Here’s another one that I like to look at. Has

anybody heard on CNBC in the last week comparisons

with 1937 and the mistake the Federal Reserve made in

1937 because it is a constant thing they’re bringing

up? But again, here’s the net worth chart I showed

in the first slide in dark blue, but look at the

light blue line, which is net worth in 1935 in

the U.S. We’re not even close to the kind of numbers

we had in 1937. And if I showed you all those other

four charts, they wouldn’t have moved during the four

years either.

And finally, one more comparison with Japan. In

light blue is average net worth per household in the

U.S. In dark blue is Japan. If you took apples to

apples the same time period, there’s just no

comparison.

So, my point is this, if I was giving you a quiz and

you looked at these five charts and you hear all this

talk about a deflation and depression and how

horrible things are, let me just say this, the

Federal Reserve was founded in 1913. This is the

first time in 102 years, A, the central bank bought

bonds and, B, that we‘ve had zero interest rates and

we’ve had them for five or six years. So, do you

think this is the worst economic period looking at

these numbers we’ve been in in the last 102 years?

To me it’s incredible.

Now, the fed will say well, you know, if we didn’t

have rates down here and we didn’t increase our

balance sheet, the economy probably wouldn‘t have

done as well as it’s done in the last year or two.

You know what, I think that’s fair, it probably

wouldn’t have. It also wouldn’t have done as well as

it did in 2004 and 2005. But you can’t measure

what’s happening just in the present in the near

term. You got to look at the long term.

And to me it’s quite clear that it was the Federal

Reserve policy. I don’t know whether you remember.

they kept coming up with this term back at the time,

they wanted an insurance policy. This we got to

ensure this economic recovery keeps going. The only

thing they ensured in my mind was the financial

crisis. So, to me you’re getting the same language

again out of policymakers. On a risk-reward basis

why not let this thing a little hot? You know, we

got to ensure that it gets out. But the problem with

this is when you have zero money for so long, the

marginal benefits you get through consumption greatly

diminish, but there’s one thing that doesn’t

diminish, which is unintended consequences.

People like me, others, when they get zero money –

and I know a lot of people in this room are probably

experiencing this, you are forced into other assets

and risk assets and behavior that you really don’t

want to do, and it’s not those concentrated bet kind

of stuff I met [ph.] earlier. It’s like gees, these

zero rates are killing me. I got to do this. And

the problem is the longer rates stay at zero and the

longer assets respond to that, the more egregious

behavior comes up.

Now. people will say well the PE is not that hard.

Where’s the beef? Again, I feel more like it was in

’04 where every bone in my body said this is a bad

risk reward, but I can’t figure out how it’s going to

end. I just know it’s going to end badly, and a year

and a half later we figure out it was housing and

Subprime. I feel the same way now. There are early

signs. If you look at IPOs, 80 percent of them are

unprofitable when they come. The only other time

we’ve been at 80 percent or higher was 1999.

The other thing I would look at is credit. There are

some really weird things going on in the credit

market that maybe Kenny and I can talk about later.

But there are already early signs starting to emerge.

And to me if I had a message out here, I know you’re

frustrated about zero rates, I know that it’s so

tempting to go ahead and make investments and it

looks good for today, but when this thing ends,

because we’ve had speculation, we’ve had money

building up for four to six years in terms of a risk

pattern, I think it could end very badly. Kenny, do

you want to come up? [applause]

SD:

Okay. I mentioned credit. I mentioned credit.

Let’s talk about that for a minute. In 2006 and

2007, which I think most of us would agree was not a

down period in terms of speculation, corporations

issued $700 billion in debt over that two-year

period. In 2013 and 2014 they’ve already issued $1.1

trillion in debt, 50 percent more than they did in

the ’06. ’07 period over the same time period. But

more disturbing to me if you look at the debt that is

being issued, Kenny, back in ’06, ’07, 28 percent of

that debt was B rated. Today 71 percent of the debt

that’s been issued in the last two years is B rated.

So, not only have we issued a lot more debt, we’re

doing so at much less standards. Another way to

look…

SD: …at that is if those in the audience who know what

covenant-light loans are, which is loans without a

lot of stuff tied around you, back in ’06, ’07 less

than 20 percent of the debt was issued coy-light.

Now that number is over 60 percent. So, that’s one

sign. The other sign I would say is in corporate

behavior, just behavior itself. So, let’s look at

the current earnings of corporate America. Last year

they earned $1.1 trillion; 1.4 trillion in

depreciation. Now, that’s about $2.5 trillion in

operating cash flow. They spent 1.? trillion on

business and capital equipment and another 700

billion on dividends. So, virtually all of their

operating cash flow has gone to business spending and

dividends, which is okay. I’m enboard with that.

But then they increase their debt 600 billion. How

did that happen if they didn’t have negative cash

flow? Because they went out and bought $567 billion

worth of stock back with debt, by issuing debt. So,

what’s happening is their book value is staying

virtually the same, but their debt is going like

this. From 1987 when Greenspan took over for

Volcker, our economy went from 150 percent debt to

GDP to 390 percent as we had these easy money

policies moving people more and more out the risk

curve. Interestingly, in the financial crisis that

went down from about 390 to 365. But now because of

corporate behavior, government behavior, and

everything else, those ratios are starting to go back

up again.

Look, if you think we can have zero interest rates

forever, maybe it won’t matter, but in my view one of

two things is going to happen with all that debt. A,

if interest rates go up, they’re screwed and, B, if

the economy is as bad as all the bears say it is,

which I don’t believe, some industries will get into

trouble where they can’t even cover the debt at this

level.

And just one example might be 18 percent of the

high-yield debt issued in the last year is energy.

And I don’t mean to offend any Texans in the room,

but if you ever met anybody from Texas, those guys

know how to gamble, and if you let them stick a hole

in the ground with your money, they’re going to do

it. So, I don’t exactly know what’s going to happen.

I don’t know when it’s going to happen. I just have

the same horrific sense I had back in ’04. And by

the way, it lasted another two years. So. you don‘t

need to run out and sell whatever tonight.

KL:

Will this unprecedented global money printing ever

stop? And what is your intermediate and long-term

view on inflation?

SD:

Well, the global money printing is interesting

because the United States is the world‘s central

bank. And Japan had this guy named Shirakawa running

the central bank, and he didn’t believe in this

stuff. So, what happened when he didn’t print the

money but the U.S. was printing the money and we’re

[inaud.], the Japanese yen started to appreciate and

it stayed appreciating, and it basically hollowed out

the country. And they were eventually forced, as you

know, two years ago into flooding their system with

money.

You have a very, very similar situation going on in

Europe now. I know Mario Draghi and Angela Merkel

don’t like QE. They don’t like anything about it,

but again, the chump – I have this partner. I don’t

know if he’s in the room, Kevin Warsh who’s on the

Federal Reserve Board. He said Japan used to be the

new chump because they had the overvalued currency.

Now it’s Europe. So, their currency went from 82 say

back in 2000 all the way up to 160, and it was 140

last summer, and they’re absolutely getting murdered.

And now they’re apparently caving in and they’re

going to print money.

I don’t know when it’s going to stop. And on

inflation this could end up being inflationary. It

could also end up being deflationary because if you

print money and save banks, the yield curve goes

negative and they can’t earn any money or let’s say

the price of oil goes to $30, you could get a

deflationary event. If you had asked me this

question in late ’03, I’d have said well, this

probably ends with inflation, but by the time we

needed to, we figured out no, this is going to end in

deflation. So, the fed keeps talking about

deflation, but there is nothing more deflationary

than creating a phony asset bubble, having a bunch of

investors plow into it and then having it pop. That

is deflationary.

KL:

You mentioned some of your biggest winners in your

career. What is the biggest mistake you made and

what did you learn from it?

SD:

Well, I made a lot of mistakes, but I made one real

doozy. So, this is kind of a funny story, at least

it is 15 years later because the pain has subsided a little.

But in 1999 after Yahoo and America Online

had already gone up like tenfold, I got the bright

idea at Soros to short internet stocks. And I put

200 million in them in about February and by

mid-march the 200 million short I had lost $600

million on, gotten completely beat up and was down

like 15 percent on the year. And I was very proud of

the fact that I never had a down year, and I thought

well, I’m finished.

The Gun Slingers

So, the next thing that happens is I can’t remember

whether I went to Silicon Valley or I talked to some

22-year-old with Asperger’s. But whoever it was,

they convinced me about this new tech boom that was

going to take place. So I went and hired a couple of

gun slingers because we only knew about IBM and

Hewlett-Packard. I needed Veritas and Verisign. I

wanted the six. So, we hired this guy and we end up

on the Year — we had been down 15 and we ended up

like 35 percent on the year. And the Nasdaq’s gone

up 400 percent.

—-

There’s nothing in this world, which will so violently distort a man’s judgment more than the sight of his neighbor getting rich.

JP Morgan, 1907

—-

So, I’ll never forget it. January of 2000 I go into

Soros’s office and I say I’m selling all the tech

stocks, selling everything. This is crazy. [unint.]

at 104 times earnings. This is nuts. Just kind of

as I explained earlier, we’re going to step aside,

wait for the net fat pitch. I didn’t fire the two

gun slingers. They didn’t have enough money to

really hurt the fund, but they started making 3

percent a day and I’m out. It is driving me nuts. I

mean their little account is like up 50 percent on

the year. I think Quantum was up seven. It’s just

sitting there.

So like around March I could feel it coming. I just

– I had to play. I couldn’t help myself. And three

times during the same week I pick up a – don’t do it.

Don’t do it. Anyway, I pick up the phone finally. I

think I missed the top by an hour. I bought

$6 billion worth of tech stocks. and in six weeks I

had left Soros and I had lost $3 billion in that one

play. You asked me what I learned. I didn’t learn

anything. I already knew that I wasn’t supposed to

do that. I was just an emotional basket case and

couldn’t help myself. So, maybe I learned not to do

it again. but I already knew that.

KL:

Here’s one you may not be able to answer. Why are

the regulators so intent on penalizing our best

banks?

SD:

Because the regulators are appointed by politicians

and the banks make a perfect punching bag for what’s

going on. And I will say this, I think there were

very, very bad actors in ’06, ‘07. Let’s not kid

ourselves in the banking industries.

KL:

I agree.

SD:

But the point I was making earlier is there was a

great enabler, and that was the Federal Reserve…

KL:

Yeah.

SD:

…pushing people out the risk curve. And what I

just can’t understand for the life of me, we’ve done

Dodd-Frank, we got 5,000 people watching Jamie Dimon

when he goes to the bathroom. I mean all this stuff

going on to supposedly prevent the next financial

crisis. And if you look to me at the real root cause

behind the financial crisis, we’re doubling down.

Our monetary policy is so much more reckless and so

much more aggressively pushing the people in this

room and everybody else out the risk curve that we’re

doubling down on the same policy that really put us

there and enabled those bad actors [ph.] to do what

they do. Now, no matter what you want to say about

them, if we had had five or six percent interest

rates, it would have never happened because they

couldn’t have gotten the money to do it.

KL:

What’s the future of the euro?

SD:

The currency or the union?

KL:

The currency

SD:

I think the euro needs to continue to go down because

eight of those countries have such a cost

disadvantage versus Germany right now. It’s about 40

percent because they haven’t been behaving themselves

since the euro was put together that you have severe

outright deflation not like pretend deflation like we

talk about on the board. It’s real deflation. And

they’ve got sclerosis. I can’t see Europe surviving

without the euro going down to somewhere in the

mid-80s. And if you think that’s a ridiculous

forecast, when I restarted Duquesne in 2000, the euro

was 82. Now, that was extreme. But let me ask you

this, think of the Europe and United States back in

2000 and think of them today. Do you think Europe

has made incremental gains versus the United States

or declines? So, to me it’s not unreasonable to see

the euro continue to go down.

The other thing I‘ll say, I do analyze currencies,

and it would be almost unprecedented to have a

10-month currency trend. Because all the

dislocations happen when your currency is overvalued

and it’s up long enough, it takes years to unwind

those dislocations. And it’s hard to argue the euro

is not in a trend. It’s down from 140 to 117. And

using the rule of time, I don’t think it’s

unreasonable to expect it to break 100 sometime in

the next year or two.

In terms of the euro region itself, there’s still a

lot of questions. That was put together for

political reasons really to create political unity.

And as most people in this room know, it’s doing just

the opposite. It’s creating political disunity. So,

I don’t think it’s even a given that that thing stays

together.

KL:

Okay. You put money out with other managers. What

qualities and characteristics do you look for in

those people that you place money with?

SD:

Number one, passion. I mentioned earlier I was

passionate about the business. The problem with this

business if you’re not passionate, it is so

invigorating to certain individuals, they’re going to

work 24/7, and you’re competing against them. So,

every time you buy something, one of them is selling

it. So, if you‘re with one of the lazy people or one

of the people that are just doing it for the money,

you’re going to get run over by those people.

The other characteristic I like to look for in a

money manager is when I look at their record, I

immediately go to the bear markets and see how they

did. Particularly given sort of the five-year

outlook I’ve given, I want to make sure I’ve got a

money manager who knows how to make money and manage

money in turbulent times, not just in bull markets.

The other thing I look for, Kenny, is open-mindedness

and humility. I have never interviewed a money

manager who told you he’d never made a mistake, and a

lot of them do, who didn‘t stink. Every great money manager I’ve ever met, all they want to talk about is

their mistakes. There’s a great humility there. But

and then obviously integrity because passion without

integrity leads to jail. So, if you want someone

who’s absolutely obsessed with the business and

obsessed with winning, they’re not in it for the

money, they’re in it for winning, you better have

somebody with integrity.

KL:

You’ve expressed concerns about entitlement. What’s

the solution? You got a loaded crowd here now. Be

careful.

SD:

That’s a rough one. So, if you go back to 1965, the

senior poverty rate in this country was 30 percent,

and it’s 9 percent now. I think everybody can

applaud that’s a great achievement. The problem is

you go back to 1965, your child poverty was 21

percent, and now it’s 25 percent. So, all the gains we’ve made in terms of poverty the last 40 years have accrued to the

elderly. If you look at the average per capita

income in this country, we’re spending 56 percent of

every worker’s dollars on the elderly, and we’re

spending 7 percent on children.

So, how would I solve it? Well, I couldn’t because

if I wanted to do it, nobody would ever vote me in

office. But I would just say that some solutions are

a combination of tax reform dealing specifically with

the problem because the longer this goes on, the more

you’re either going to have to raise taxes or cut

spending down the road because of compounding. I

would freeze — forget COLAs. I would freeze all the

entitlement payments right now because they’ve

already taken such a tremendous share away from the

rest of our population.

You know, it’s funny. if you go back to as late as

1970, entitlements were 28 percent of all federal

outlays. Now they’re 72 percent. And when you start

talking about oh my God, we can’t freeze this stuff,

why not? You just picked up 50 points of share on

everybody. Why not freeze it? And, you know, Ken

and I have talked. I mean it’s ridiculous that our

Social Security is not means tested. It’s

ridiculous. I mean the fact that he’s getting – what

is your monthly check?

KL:

Twenty-five hundred dollars a month.

SD:

It’s ridiculous.

KL:

And Elaine gets another thousand.

SD:

While we have 24 percent of the kids in this country

in poverty and probably, you know, the elephant in

the room is obviously the health care system. You’ve

got to get the market into the equation so people see

the cost and they have to make an economic decision.

A lot of this goes into end-of-life payments. You

wonder if you had to pay 30 to 40 percent of the bill

instead of not even knowing what the bill is, whether

different choices would be made.

But you talk about entitlement. The federal debt

right now is $17 trillion. The reason it‘s

$17 trillion and not higher is because all those

payments that are promised to Kenny, a lot of the

people in this room, myself not too far in the

future, they’re not on the government balance sheet.

Any company in America if you owe payments of that

certainty, it would be a debt. In the U.S.

government accounting it’s revenue.

If you present valued what we have promised to

seniors in Medicare and Social Security and Medicaid

payments, the federal debt right now under gap

accounting would be $205 trillion, not 17 because we

have a demographic boom, which is the other side of

the baby boom. As everybody knows in this room, it’s

the grey boom. We are creating 11,000 seniors in

this country every day. Every day we’re creating

11,000 new seniors, and we’re only creating about 18

percent of youth employed to support those payments

to them. So, we’ve got a big problem, and it really

doesn’t start until 2024, 2025, but if you wait ’til

2024, it’s too late. It’s not unlike climate change.

It’s probably not a problem for 30 years, but if you

wait 30 years, you can’t fix it. So, you got to

start now.

KL:

This is my question, is there any way possible you

think that we could have a soft landing from all the

excesses we’ve had in the last 10 or 15 Years?

SD:

Anything’s possible. I sure hope so.

And I haven’t committed. I’m not net short equities. I mean the

stock market right now as a percentage of GDP is

higher than – with the exception of nine months from

’99 to — it’s the highest it’s been in the last

hundred years of any other period except for those

nine months. But you know what, when you look at the

monetary policy we’re running, it should be – it

should be about where it is. This is crazy stuff

we’re doing. So, I would say you have to be on alert

to that ending badly. Is it for sure going to end

badly? Not necessarily. I don’t quite know how we

get out of this, but it’s possible.

KL: Okay. Stanley, fabulous. Thank you so much.

SD:

Thanks, Ken.

KL:

Great, great night.

As central bankers distort the true cost of capital, the side effects are mathematically incalculable. We’ll never know how many Bernie Madoffs maybe sipping mint juleps on the Hamptons this summer? If Lehman didn’t fail, would Bernie have ever been caught? Failure is a good thing, a cleansing thing and so is a “true cost of capital” which the free-market used to forge each day, but NO more. Many people think Keynes was a lower interest rates kind of guy, using the cost of capital – monetary policy – to stimulate an economy. That part is true, but it just might be the most significant half-truth coming out of the last 100 years of modern economics. Above all, he was a believer in the natural rate of interest. When you juice fiscal policy in a short period of time by $5T and hit the monetary policy accelerator at the same time by $3T, the spread between the true cost of capital and the artificial, or the central bank suppression rate – is COLOSSAL.

As central bankers distort the true cost of capital, the side effects are mathematically incalculable. We’ll never know how many Bernie Madoffs maybe sipping mint juleps on the Hamptons this summer? If Lehman didn’t fail, would Bernie have ever been caught? Failure is a good thing, a cleansing thing and so is a “true cost of capital” which the free-market used to forge each day, but NO more. Many people think Keynes was a lower interest rates kind of guy, using the cost of capital – monetary policy – to stimulate an economy. That part is true, but it just might be the most significant half-truth coming out of the last 100 years of modern economics. Above all, he was a believer in the natural rate of interest. When you juice fiscal policy in a short period of time by $5T and hit the monetary policy accelerator at the same time by $3T, the spread between the true cost of capital and the artificial, or the central bank suppression rate – is COLOSSAL.  Many people forget, from 1971 to 1974, gold was 325% higher, while everyone remembers the 475% surge from 1977 to 1980. The U.S., stagflation commenced after an egregious expansion of the money supply was initiated to counter the precipitous increase in oil prices caused by the October 1973 oil embargo announced by the Organization of Arab Petroleum Exporting Companies to punish those countries that had supported Israel in the Yom Kippur war which lasted from October 6th to October 25th, 1973, led by Egypt and Syria against Israel. Oil prices initially increased by 17%, but at its peak, prices shot up 400%.

Many people forget, from 1971 to 1974, gold was 325% higher, while everyone remembers the 475% surge from 1977 to 1980. The U.S., stagflation commenced after an egregious expansion of the money supply was initiated to counter the precipitous increase in oil prices caused by the October 1973 oil embargo announced by the Organization of Arab Petroleum Exporting Companies to punish those countries that had supported Israel in the Yom Kippur war which lasted from October 6th to October 25th, 1973, led by Egypt and Syria against Israel. Oil prices initially increased by 17%, but at its peak, prices shot up 400%. Dollar bulls have run for the hills at the second most fierce pace in the last seven years.

Dollar bulls have run for the hills at the second most fierce pace in the last seven years.  In the US, fiscal stimulus was supposed to struggle to cap the revenue drop caused by the unprecedented nature of this crisis. To an extent, it has, but what this narrative missed in a distributional sense is, the policy response to deflationary shocks has changed. The government sends out money and the central bank does open-ended QE. Does this mean future growth is promised, no, but it does change the recession landscape in terms of size and duration? Long-drawn out deflationary episodes have to be repriced as we seem to have a better recipe for dealing with them as opposed to 2008.

In the US, fiscal stimulus was supposed to struggle to cap the revenue drop caused by the unprecedented nature of this crisis. To an extent, it has, but what this narrative missed in a distributional sense is, the policy response to deflationary shocks has changed. The government sends out money and the central bank does open-ended QE. Does this mean future growth is promised, no, but it does change the recession landscape in terms of size and duration? Long-drawn out deflationary episodes have to be repriced as we seem to have a better recipe for dealing with them as opposed to 2008. A clear down parallelogram was formed as a result of March high into the June low. Subsequently, it broke through the bottom line of the parallelogram, which sets up an early resolution, i.e. it sets up an early test of the apex price point. If that fails, it is in free fall.

A clear down parallelogram was formed as a result of March high into the June low. Subsequently, it broke through the bottom line of the parallelogram, which sets up an early resolution, i.e. it sets up an early test of the apex price point. If that fails, it is in free fall. Has the Japanese yen become the world’s risk-off currency? Hard to process a $4 to $5 trillion federal deficit under a Republican Administration without concluding that either inflation is around the corner of the dollar is going to substantially weaken or most likely both. Some feel a blue-wave will lead to even more MMT experiments (modern monetary theory)?

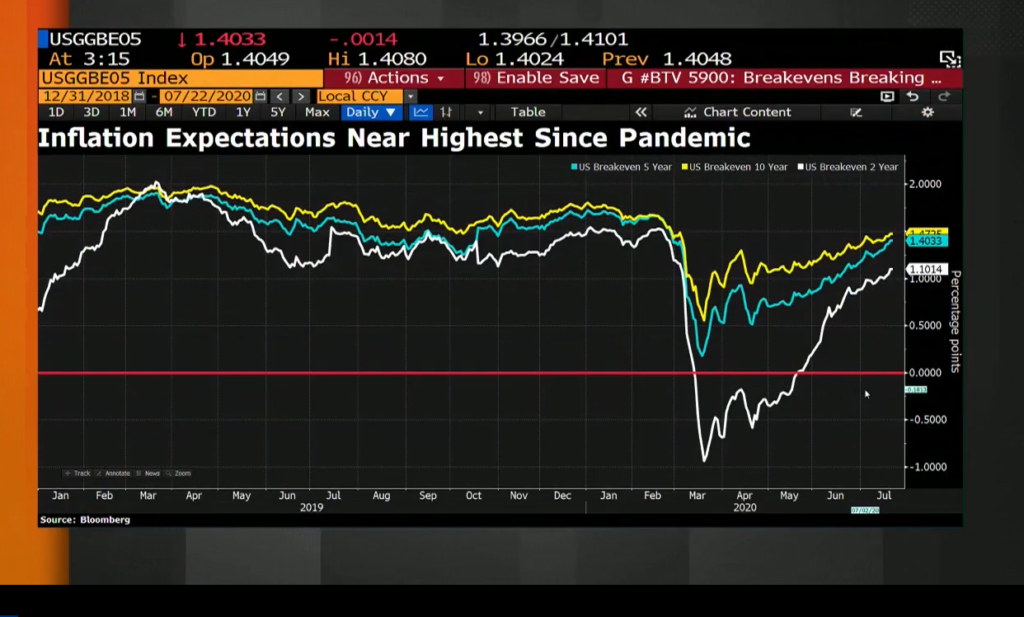

Has the Japanese yen become the world’s risk-off currency? Hard to process a $4 to $5 trillion federal deficit under a Republican Administration without concluding that either inflation is around the corner of the dollar is going to substantially weaken or most likely both. Some feel a blue-wave will lead to even more MMT experiments (modern monetary theory)? Real bond yields are plunging. Say you’re a billionaire in the middle-east with loads of short-term treasuries. Your return on investment, after inflation expectations, is paltry. What can you do?

Real bond yields are plunging. Say you’re a billionaire in the middle-east with loads of short-term treasuries. Your return on investment, after inflation expectations, is paltry. What can you do?  The gold bugs have been lost for decades, precious metals have always been a game played on the fixed income field.

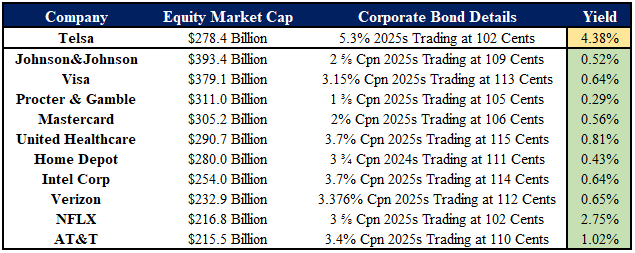

The gold bugs have been lost for decades, precious metals have always been a game played on the fixed income field.  This is remarkable data, Tesla’s five-year bonds are yielding nearly 400bps more than their possible market capitalization neighbors in the S&P 500.

This is remarkable data, Tesla’s five-year bonds are yielding nearly 400bps more than their possible market capitalization neighbors in the S&P 500. See

See