Join our Larry McDonald on CNBC’s Trading Nation, Wednesday June 8, at 2pm.

Pick up our latest Bear Traps Report menu here.

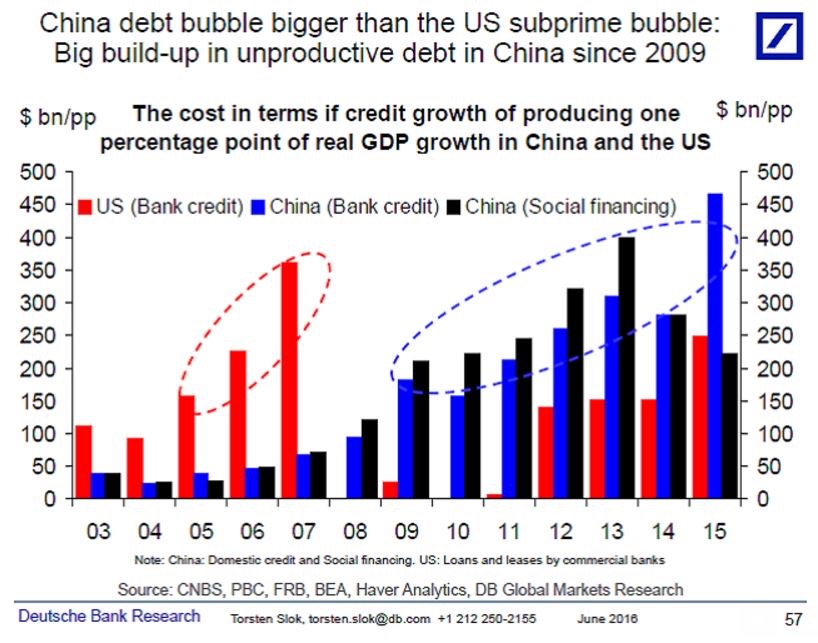

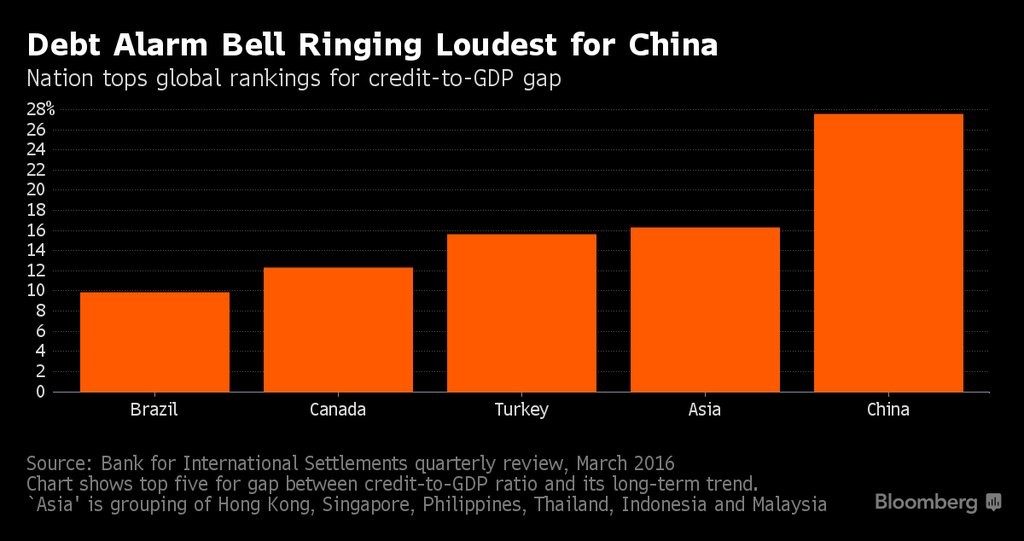

The explosion of off balance sheet financing in China is creating Lehman like risk across Asia’s financial system.

U.S. equity investors must keep an eye on China. The last two elevator shaft drops in the S&P 500, 12% last August – September and 14% in January – February, both had there genesis in China.

“The regions face high levels of contingent liabilities.” Moody’s

“Off balance sheet financing increases uncertainties.” S&P

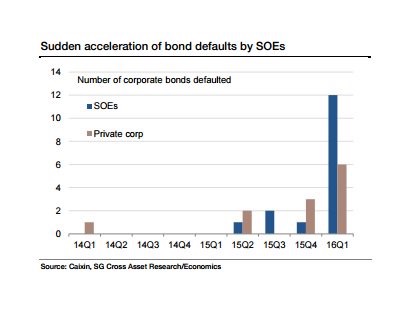

Year-to-date, there have already been 71 downgrades by S&P Global Ratings and 150 by Moody’s.

China Off Balance Sheet Financing*

Q22016: $300B

Q12016: $160B

Q42015: $230B

Q32015: $230B

Q22015: $140B

Q12015: $0

*local government bond issuance surges to a fresh record high

Shadow Banking 2.0

An Evil Thirst for Yield

Lets not forget, from December 2001 through November 2004, the Federal Reserve kept rates between 1% and 1.75%, down from 6.5% in 2000.

The net result? Trillions of dollars flowed into shadow banks in the USA as investors sought higher yields.

The same thing is playing out today in China.

Cost of Default Protection on China

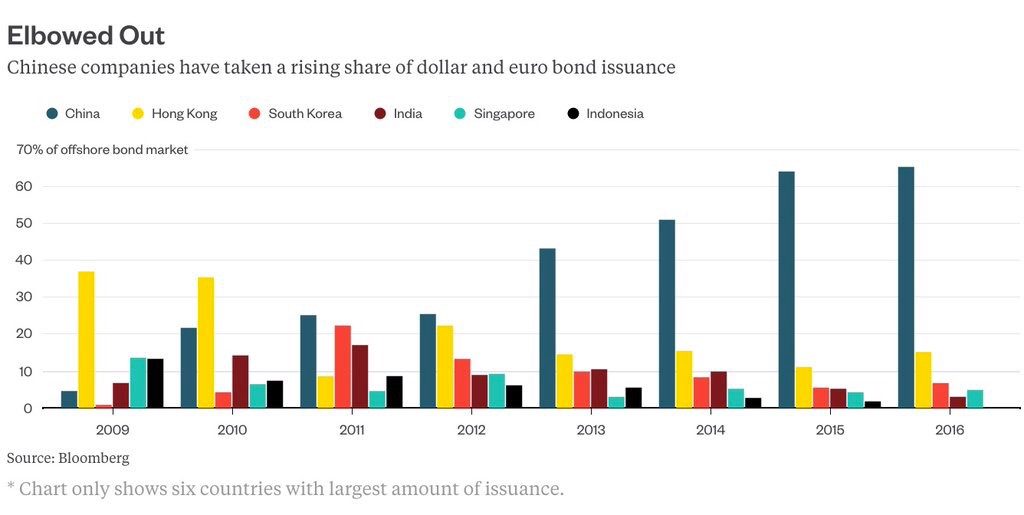

Direct sales of local government bonds have surged to a record 2 trillion yuan ($304 billion) since March 31, up from 906 billion yuan in the first quarter, fueled by a program to swap expensive debt for cheaper municipal securities. Moody’s Investors Service and S&P Global Ratings say that while municipal notes are a more transparent way of raising money than the previous practice of using private financing vehicles, the concern is that authorities are still resorting to off-balance-sheet funding methods.

Bloomberg

The Global Epicenter of Risk

2015-16: China / Asia

2010-12: Europe

2006-8: USA

One of our classic systemic risk indicators is found in global banks positioned near the epicenter of risk. Standard Chartered is a leveraged bank with a high concentration of risk focused on Asia.

“Our negative outlook on the Chinese sovereign ratings reflect both slow economic rebalancing and growing financial risks,”

“Non-government debt is still growing relatively quickly and off-balance-sheet financing increases uncertainties in the financial system that could worsen the impact of any potential economic or financial shock on China,”

S&P Global Ratings

Cost of Default Protection on Indonesia and Malaysia

Our trade ideas focused here include….

Pick up our latest Bear Traps Report menu here.

The U.S. dollar has been acting like a biotech stock in and around incoming jobs data. Central bankers have far too many asset managers trying to create alpha (returns) around their speeches and incoming data. The result? Capital destroying volatility in and around news flow. Each time we see far to many people on once side of the boat, listing her closer to capsizing.

The U.S. dollar has been acting like a biotech stock in and around incoming jobs data. Central bankers have far too many asset managers trying to create alpha (returns) around their speeches and incoming data. The result? Capital destroying volatility in and around news flow. Each time we see far to many people on once side of the boat, listing her closer to capsizing.

Over the last year, the global wrecking ball that is the U.S. dollar index has ripped apart the global economy. The pull back from February – April in the greenback was a breath of fresh air for markets. Last year, U.S. ISM Manufacturing was hammered by the dollar’s surge, today it surprised to the upside.

Over the last year, the global wrecking ball that is the U.S. dollar index has ripped apart the global economy. The pull back from February – April in the greenback was a breath of fresh air for markets. Last year, U.S. ISM Manufacturing was hammered by the dollar’s surge, today it surprised to the upside.