*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Sept 6: What Just Happened over the last Nasdaq 14 days?

1. A Colossal buyer (SoftBank) distorted the price of upside calls on eight stocks.

2. Quants and Robinhood piled on, further distorting markets.

3. Dealers who have been destroyed in recent years (selling vol) holding a small deck, they had to get long more and more stock to hedge upside market risk.

4. As stocks surged, dealers who sold upside calls – must hedge even more as – out of the money options they sold – pick up more delta. Banks buy more stock. Call-put skew reaches record territory on several big-name tech stocks, meaning the cost differential to buy upside vs. protect the downside, reaches all-time wide levels.

5. Nasdaq is nearly 60% 12 stocks, this “three-card monte” game above has a large impact on passive index funds.

6. The original, colossal upside call buyer exits some of their position.

7. Dealers / banks MUST sell stock in size, take off their hedges, sell Mortimer, SELL.

8. Selling brings out more selling, banks take off more hedges as the options lose delta, MORE selling.

9. The little guy / gal gets left holding the bag.

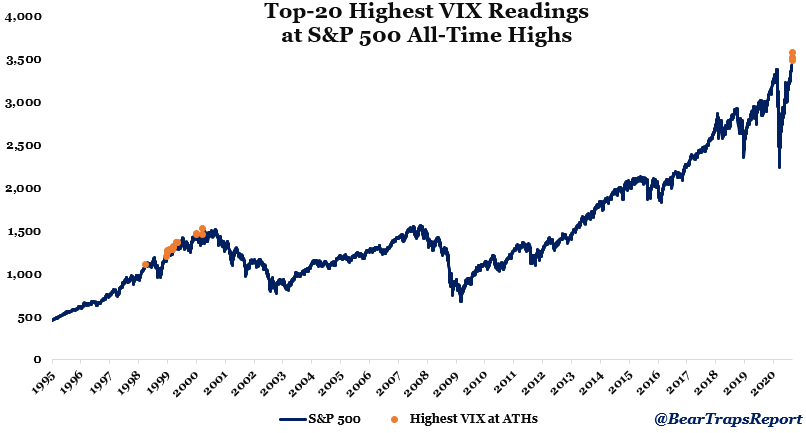

Alert: High and High Closes September 2, 2020

Wednesday, an All-time highest VIX reading on a day with the S&P 500 touching the highest level ever. Of the top 20 occurrences, there were 17 in the 1999-2000 period, and three over the last 7 days. When option traders receive colossal size orders to buy upside calls they have two choices. a) Have your sales force get on the phone to the largest holders of the stock (say Apple and Buffett) and convince them to sell upside calls. b) If they cannot find enough sellers of upside calls, they must buy stock in size to hedge the calls they are selling to the client. This is taking the street short gamma – likely the largest way all time. As we learned with Lehman, greed breaks things. It’s “high-noon” – the only character missing is Gary Cooper. We are witnessing a battle of wills, high speculation where colossal call buyers are forcing the street to get long more and more stock to hedge their upside risk. It’s the March capitulation selling in reverse. Just the way the street had to BUY downside protection in late March (because put buyers outnumbered call buyers 10-1). Today, they are being forced to BUY upside protection in SIZE (call buyers outnumbered put buyers 10-1). It’s going to break!

Wednesday, an All-time highest VIX reading on a day with the S&P 500 touching the highest level ever. Of the top 20 occurrences, there were 17 in the 1999-2000 period, and three over the last 7 days. When option traders receive colossal size orders to buy upside calls they have two choices. a) Have your sales force get on the phone to the largest holders of the stock (say Apple and Buffett) and convince them to sell upside calls. b) If they cannot find enough sellers of upside calls, they must buy stock in size to hedge the calls they are selling to the client. This is taking the street short gamma – likely the largest way all time. As we learned with Lehman, greed breaks things. It’s “high-noon” – the only character missing is Gary Cooper. We are witnessing a battle of wills, high speculation where colossal call buyers are forcing the street to get long more and more stock to hedge their upside risk. It’s the March capitulation selling in reverse. Just the way the street had to BUY downside protection in late March (because put buyers outnumbered call buyers 10-1). Today, they are being forced to BUY upside protection in SIZE (call buyers outnumbered put buyers 10-1). It’s going to break!

Insanity in Options

This post is Part II of New Vol Regime

“As my first boss told me at Merrill Lynch in 1990, ´In options Larry, they show it to you (lush $$ green premium), and then they take it away.´”

LGM

The convexity skew picture on big-name equities like Apple $AAPL has gone parabolically stupid. Let’s keep this simple and draw a conclusion.

“Over the past few weeks, there has been a massive buyer in the market of Technology upside calls and call spreads across a basket of names including ADBE, AMZN, FB, CRM, MSFT, GOOGL, and NFLX. Our friends at Citadel calculate, over $1 BILLION of premium spent and upwards of $20B in notional through strike – this is arguably some of the largest single stock-flow we’ve seen in years, they noted. We agree someone is playing with House Money, and they’re rolling large.”

Bear Traps Report, August 24, 2020

Apple $AAPL Stock near $130

Jan $180 Strike Calls costs $4

Jan $80 Strike Puts costs $1

*Both options are $50 out of the money, approx data, BUT it is nearly 3x more expensive to buy upside risk in AAPL equity. Downside protection normally costs more than upside risk participation, NOT today. What does this mean?

“The public is trapped long and institutions are trapped long and the snowball that was pushed very quickly up the hill and got big is now at risk of becoming an avalanche.”

Julian Emanuel, chief equity and derivatives strategist at BTIG, Bloomberg

Nasdaq Whale Makes a Splash

One large buyer has made a colossal splash in the market and the scent of greed has drawn thousands of other market participants into the dangerous game. Several clients in our institutional chat on Bloomberg have cited SoftBank as the original size buyer. We have NO IDEA if this is true, just that highly credible clients have made this reference several times over the last week. It’s a high-stakes game of musical chairs, the ultimate greater fool theory moment. The colossal call buyer has thrown meat in the water and drawn in the sharks, but unfortunately thousands of Robinhood minnows at the same time. When the large players’ exit, the little guy and gal will be left holding the bag.

Apple closed near $130, while the cost of speculative upside calls is weighted heavily against the buyer. Someone must have reached out to Buffett today because he can make a fortune in selling $AAPL upside calls. Let us explain.

Very Expensive Upside

Call it extremely unusual activity. We have a higher stock price in Apple AAPL with a much higher cost of equity upside. Equity vol usually explodes higher in market crashes, NOT bull markets. As you can see above, in normal Apple equity bull markets – see all of 2019 – AAPL implied vol has been CHEAP, NOT RICH (expensive) like today! In March and April, near the market bottom – the price for puts was more than 4x the price for calls, today we have done a 180, extreme fear to extreme greed.

Call it extremely unusual activity. We have a higher stock price in Apple AAPL with a much higher cost of equity upside. Equity vol usually explodes higher in market crashes, NOT bull markets. As you can see above, in normal Apple equity bull markets – see all of 2019 – AAPL implied vol has been CHEAP, NOT RICH (expensive) like today! In March and April, near the market bottom – the price for puts was more than 4x the price for calls, today we have done a 180, extreme fear to extreme greed.

In our institutional client chat on Bloomberg, a hedge fund put on this trade and we are sharing it with permission.

With Apple stock near $130, think of the January 2021 expiration. The client bought the $200 call and sold the $250 call, 1 x 4, and got paid $3.50 to put the trade on. What does this mean? See below.

Extreme Premium to Extreme Discount

Apple $AAPL is near $140 pre-market on September 2nd. In July, the Street’s 12-month price target was $85, now $116. In March, the price target commanded an $18 PREMIUM to the Apple stock price, NOW it’s close to a $24 discount. In classic 1990s fashion, the mad mob of Wall St. analysts cannot raise their stock price targets fast enough to keep up with the equity price appreciation. That is from 44 analysts, Bloomberg data.

Apple $AAPL is near $140 pre-market on September 2nd. In July, the Street’s 12-month price target was $85, now $116. In March, the price target commanded an $18 PREMIUM to the Apple stock price, NOW it’s close to a $24 discount. In classic 1990s fashion, the mad mob of Wall St. analysts cannot raise their stock price targets fast enough to keep up with the equity price appreciation. That is from 44 analysts, Bloomberg data.

The Trade

Apple was worth $1.5T at the end of July and today she stands tall at $2.2T. In order for the client to lose money* at January expiration, the stock has to breach $270 ($130-$136 this week), which would put the company’s market capitalization very close to $5T, by January 2021, that is a little over four months away.

*The mark to market in the short run can be extremely painful though – if Apple equity soars another 10-20% (Apple is up 50% since late July), that is indeed the catch. AAPL is trading nearly 65% above its 200-day moving average vs. 42% in February’s great bull run.

Cost of Upside is Insanely Expensive

There are a handful of quant funds pushing around a few stocks (with high impact on QQQ, NDX, SPY) in the options markets. The dealers are getting very nervous. Last 15 days – Imaging being a large market maker in Apple and Tesla equity options. You make a market, bid – offer, you get lifted and lifted over and over again by buyers to the point where you have raised the price of calls vs puts to multi-year extremes. How short is the Street gamma? VERY.

There are a handful of quant funds pushing around a few stocks (with high impact on QQQ, NDX, SPY) in the options markets. The dealers are getting very nervous. Last 15 days – Imaging being a large market maker in Apple and Tesla equity options. You make a market, bid – offer, you get lifted and lifted over and over again by buyers to the point where you have raised the price of calls vs puts to multi-year extremes. How short is the Street gamma? VERY.

The Ultimate Lesson From Stan

“So, I’ll never forget it. January of 2000 I go into Soros’s office and I say I’m selling all the tech stocks, selling everything. This is crazy at 104 times earnings. This is nuts. Just kind of as I explained earlier, we’re going to step aside, wait for the net fat pitch. I didn’t fire the two gunslingers. They didn’t have enough money to really hurt the fund, but they started making 3 percent a day and I’m out. It is driving me nuts. I mean their little account is like up 50 percent on the year. I think Quantum was up seven. It’s just sitting there… So like around March I could feel it coming. I just – I had to play. I couldn’t help myself. And three times during the same week I pick up a – don’t do it. Don’t do it. Anyway, I pick up the phone finally. I think I missed the top by an hour. I bought $6 billion worth of tech stocks. and in six weeks I had left Soros and I had lost $3 billion in that one play. You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to that. I was just an emotional basket case and couldn’t help myself. So, maybe I learned not to do it again. but I already knew that ”

Stan Druckenmiller

When call vs. put skew gets this extreme it can be a solid leading risk indicator. Join our live chat here, tatiana@thebeartrapsreport.com.