“For the rest of the year, we think global credit risk will veto the Fed’s policy path (no hikes) and therefore, gold and the gold miners are going to do very, very well in that environment in 2016.”

Bear Traps Report’s Larry McDonald, January 2016 on CNBC

Aspen Institute in Aspen, Colorado on Sunday

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereToday, Federal Reserve Vice Chairman Stanley Fischer said the U.S. economy moving ever so near to the central bank’s objectives and he expects growth to pick up in the future.

As a key member of Janet Yellen’s inner circle Stan Fischer’s words carry 10x the weight of non voting, regional Fed bank presidents.

Air Pocket

Considering over 3000 current Dow (Dow Jones Industrial Average) points are supported by the easy money Fed gravy train, we recommend keeping yours eyes and ears on him.

The Bloomberg dollar index is off 3% over the last 20 days while gold has been stuck in a trading range.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here“We are close to our targets.. Looking ahead, I expect GDP growth to pick up in coming quarters, as investment recovers from a surprisingly weak patch and the drag from past dollar appreciation diminishes.”

Stanley Fischer

Over 547,000 new jobs have been created in June and July, so why is the Fed so cautious on the 2016 rate hike?

Fed’s Fischer

U.S. Job Market: “remarkably resilient”

U.S. GDP Growth: “mediocre at best.”

Fischer trying to balance out is speech here.

December Rate Hike vs Bloomberg Dollar Index*

Today: 52% vs 1166

Month Ago: 43% vs 1198

*weaker dollar with higher rate hike probability

Bloomberg data

We’re witnessing a remarkable divergence between the U.S. dollar and Fed Fund Futures. The dollar has plunged 3% over the last 20 days while the futures market is pricing in a much higher chance of a December Fed rate hike.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereFischer Balancing Hawkish Comments with Dovish Concern

“A 1.25 percentage point slowdown in productivity growth is a massive change, one that, if it were to persist, would have wide-ranging consequences for employment, wage growth, and economic policy more broadly,”

Stan Fischer

Fed Fund Futures vs Fed Dots*

Effective Fed Funds

Today: 0.40%

2017: 0.65% v 1.60%

2018: 0.78% v 2.36%

*Fed’s projections on rates

Bloomberg data

The futures market is giving the Fed the Rodney Danderfield, “no respect”. Traders are pricing in just one rate hike between now and the end of 2018. On the other hand, the Fed dots are pointing to seven rate hikes over the same time frame. This disconnect cannot stay this wide, it’s unsustainable.

Fed officials next meet Sept. 20-21. We will listen closely for additional clues on timing when Fed Chair Janet Yellen speaks Aug. 26 at an annual in Jackson Hole, Wyoming.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Years ago, back in our Morgan Stanley days Barton Biggs warned us of the “GE – Transports non-confirmation omen.” It’s a classic sign that unsustainable factors are holding up stock prices, not solid fundamentals. We have an equity market positioned on a loose clay foundation with NO sign of bedrock.

Years ago, back in our Morgan Stanley days Barton Biggs warned us of the “GE – Transports non-confirmation omen.” It’s a classic sign that unsustainable factors are holding up stock prices, not solid fundamentals. We have an equity market positioned on a loose clay foundation with NO sign of bedrock.

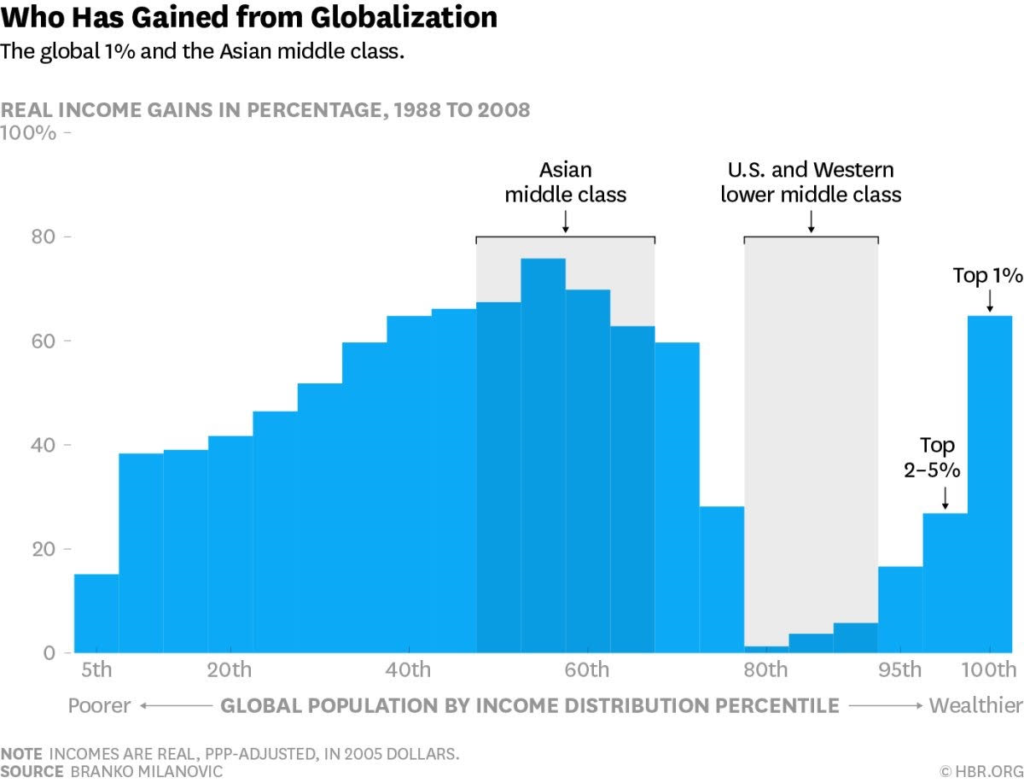

Instead of listening to 2000 journalists lecture us on how the 2016 election is all over, lets manage risk. Where’s the most attractive risk – reward in this year’s election cycle? What’s priced in and Not priced in? Should the VIX (the CBOE stock market volatility index) really be under 12 one hundred days before this election? All you need to know is up in this chart above. We call it the “revenge of Joe lunch pail.” Just like middle-class families in the countryside of England in June (Brexit vote), there are so many working class Americans who have had it with globalization, political correctness and elitist media telling them how to vote. They are tired of living in fear. All they know is their incomes and jobs have moved to Asia, terror and U.S. racial tensions are on the rise. It’s pure common sense. Whether right or wrong, Donald Trump has tapped into a powerful political vein running across America. It DOES NOT MATTER whether Mr. Trump has an effective plan that will work, Joe Lunch Pail is just VERY HAPPY someone is finally listening to him.

Instead of listening to 2000 journalists lecture us on how the 2016 election is all over, lets manage risk. Where’s the most attractive risk – reward in this year’s election cycle? What’s priced in and Not priced in? Should the VIX (the CBOE stock market volatility index) really be under 12 one hundred days before this election? All you need to know is up in this chart above. We call it the “revenge of Joe lunch pail.” Just like middle-class families in the countryside of England in June (Brexit vote), there are so many working class Americans who have had it with globalization, political correctness and elitist media telling them how to vote. They are tired of living in fear. All they know is their incomes and jobs have moved to Asia, terror and U.S. racial tensions are on the rise. It’s pure common sense. Whether right or wrong, Donald Trump has tapped into a powerful political vein running across America. It DOES NOT MATTER whether Mr. Trump has an effective plan that will work, Joe Lunch Pail is just VERY HAPPY someone is finally listening to him. Joe Lunch Pail is hurting, his family has been dealing with flat to declining income going on 6 years. As much as the U.S. media wants to get off this topic and focus on their perception of Trump’s flaws, they are ignoring the elephant in the room. The U.S. media regime is making the same mistake the BBC made in London during the pre-Brexit risk analysis. Far too many people priced the risk of Brexit at unrealistically low levels, we know what happened next. There are eight million people in London, 50m outside the city. London votes 8-1 to remain, but people across the countryside voted 3-1 to leave. The only problem, no one listened to the butcher, the baker, the candlestick maker. Lets NOT make the same mistake they did, we MUST learn from history, not repeat it.

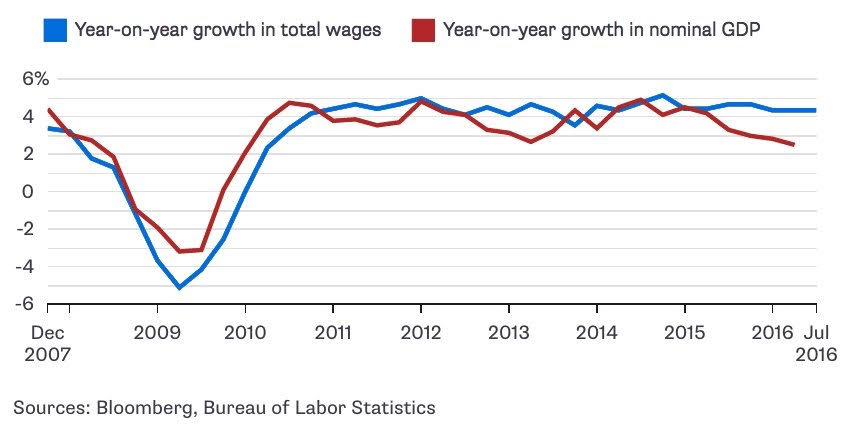

Joe Lunch Pail is hurting, his family has been dealing with flat to declining income going on 6 years. As much as the U.S. media wants to get off this topic and focus on their perception of Trump’s flaws, they are ignoring the elephant in the room. The U.S. media regime is making the same mistake the BBC made in London during the pre-Brexit risk analysis. Far too many people priced the risk of Brexit at unrealistically low levels, we know what happened next. There are eight million people in London, 50m outside the city. London votes 8-1 to remain, but people across the countryside voted 3-1 to leave. The only problem, no one listened to the butcher, the baker, the candlestick maker. Lets NOT make the same mistake they did, we MUST learn from history, not repeat it. You wont find this chart in the main stream media, but unemployment is sharply on the rise in the Rust Belt, especially in Ohio and Pennsylvania.

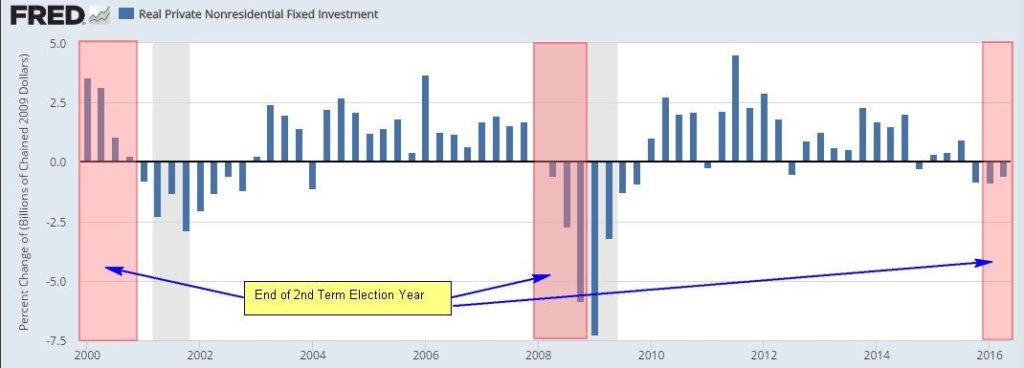

You wont find this chart in the main stream media, but unemployment is sharply on the rise in the Rust Belt, especially in Ohio and Pennsylvania.  Two term Presidential elections and recessions have a lot in common.

Two term Presidential elections and recessions have a lot in common. Oil in blue, junk bonds in white are singing a classic warning sign for us all. The disconnect is eerie. As long as desperate insurance companies in Tokyo and Frankfurt have an unending thirst for yield, U.S. junk will be mispriced. Short Junk Now.

Oil in blue, junk bonds in white are singing a classic warning sign for us all. The disconnect is eerie. As long as desperate insurance companies in Tokyo and Frankfurt have an unending thirst for yield, U.S. junk will be mispriced. Short Junk Now. German and Japan 10 year bonds, married at -0.08%, a true global growth story.

German and Japan 10 year bonds, married at -0.08%, a true global growth story.