Brexit risk looks fully priced in to us. Reminiscent of Y2K, fears have gone viral. The British Pound is back to the lovely days of Princess Diana.

The In / Out referendum on Britain’s future in the EU will be held in just over six weeks, on June 23, 2016. Prime Minister David Cameron is in favour of continued British membership, under the terms he negotiated early in 2016. Cameron has the support of the Chancellor the Exchequer George Osbourne, and the majority – but not all – of his Cabinet. Several cabinet members, including prominent Tories are campaigning for a so called Brexit. Outside of the Cabinet, the popular former Mayor of London Boris Johnston will also campaign in favour of Brexit.

The next three largest parties in the House of Commons – Labour, the SNP, and the Liberal Democrats, are all campaigning for Britain to remain in the EU. The Eurosceptic UKIP has only one seat in parliament but received 12.7% of the vote in the 2015 general election. Unsurprisingly, it is campaigning for Brexit.

AUSTRALIAN 10-YEAR BOND YIELD DROPS TO RECORD LOW AT 2.22%

Most wish it was a growth story, but there’s little faith in the global economy.

Since February, emerging market asset prices have been supported by two factors, both of which will prove fleeting.

Up until May 3rd, Janet Yellen had her foot on the US Dollar’s neck, while the PBOC expanded credit in China at the fastest pace since 2009. The dollar index DXY plunged 6.7% between March 2nd and May 3rd. In a reversal, as the dollar surged emerging-market currencies fell for seven consecutive days through Friday, the longest losing streak since March 2015.

If global investors really trusted China’s recovery, they wouldn’t be piling into Aussie 10s at 2.20%.

Bloomberg’s monthly gross domestic product tracker for China shows growth slowed to 6.88% in April, from 7.11% in March.

Growth is likely far slower, 1-2% at best.

Weak steel and coal output dragged on industrial production, which increased 6% from a year earlier versus economists’ forecasts of 6.5%, while retail and investment readings also disappointed.

The brisk pace of Federal Reserve fueled U.S. corporate debt sales for the second quarter means that 2016 may come close to reaching last year’s record-breaking $1.3 trillion of deals.

Debt is a double edged sword, as net debt relative to the underlying earnings power of the S&P is at froth levels historically.

S&P 500

Net Debt to EBITDA*

2016: 1.5x

2015: 1.4x

2014: 1.25x

2013: 1.1x

2012: 0.83x

2011: 0.9x

2010: 1x

2009: 1.1x

2008: 1.15x

* x financials

Enterprise value (EV below in the chart) takes debt + equity market capitalization into consideration. In the S&P 500, if you think of a pie with 12 pieces, five full of debt the other 5 equity, it’s foolish to just focus on the stock portion of the market’s value, especially after eight year debt binge!

As the Fed has kept rates wrapped around zero going on 8 years, investor’s thirst for yield has companies reaching new dark heights in terms of their debt loads. As the U.S. equity market has raged “risk on” since February, after the Fed agreed not to hike interest rates, stocks have become extremely expensive. SELL Signal.

What keeps us up in the middle of the night is a surge in credit quality deterioration in the face of rising bond sales. That’s NOT the way it’s supposed to work Janet Yellen! S&P Global Ratings expects default rates among junk-rated U.S. cos. to jump from 3.9% in March 2016 to 5.4% in March 2017.

S&P 500 2006-2016

Investors are paying record prices for stocks when the debt portion of value is factored in relative to raw earnings power (EBITDA = earnings before, interest, taxes, depreciation and amortization).

The problem with most Wall St. strategists is they don’t get paid to get you off the dance floor, they want you in there swinging and playing.

The “Lower and Beat Game” is on Full Throttle

A look inside the S&P 500 shows, of the 460 companies that have reported, over 75% beat lowered consensus forecasts.

Keep in mind, if the bar is set so low, anyone can massage the numbers to exceed — and analysts had been aggressively cutting estimates for the quarter in the weeks before it ended. Bottom line, Q2 will come in at -9% on the earnings front and -2.5% on the top line sales decline.

Buy Fear – Sell Complacency

We recommended subscribers buy fear in late January, there was value found in stock prices, today not so much.

“We’ve been putting cash to work as we believe a substantial relief rally is near and the Fed won’t be able to hike rates. Great bull markets don’t end overnight. This bull withstood a violent blow in October 2014 with a 10% plunge and subsequent rally in stocks over 17 days. Last August / September, the bull took another sword, suffering nearly a 13% drop. We believe he has some fight left.. Buy the IWM Russell 2000 ETF.”

A look at earnings year to date is not pretty. We’ve crossed into our third of (year over year) declines, the S&P 500 is now trading at 19x earnings vs. 17x three months ago.

Over the last 40 years, 19x earnings multiples in the S&P 500 have been associated with 4-6% U.S. GDP growth, not 1.8% as we wear today.

S&P 500 PE

In early February the S&P 500 was trading at 17x earnings, today 19x

After the first two quarters, the S&P 500 is on track to make $107.70 this year vs expectations of $121.70. We think the S&P will finish 2016 at $111.50 in earnings.

Street economists have blindly been focused on economic data in their effort to figure out what the Fed is going to do. We’ve made the point, you’re far better off keeping a close eye on credit markets.

2s -10s

Over the last 70 years, the spread between the 2 year Treasury and the ten year has been a reliable economic forecaster. If the economy is truly growing, creating sustainable wage pressure inflation, the spread between 2s – 10s will widen. In other words, investors will demand a higher yield on long term bonds relative to what they’re receiving on short term paper.

The spread between 2-10s hit a fresh 8 year low last week (see below).

One of the Biggest Victims?

Years ago, banks made upwards of 30% of their bottom line profits “playing the NIM.” Net Interest Margins are vital to a banks long term sustainable profitability. Simply put, banks borrow short and lend long term. A flat yield curve is no friend of the banks, not to mention rising risks of recession.

Back in February, near the market lows on CNBC we recommended clients get long the banks to take advantage of fear and capitulation (the banks surged 21% from our buy call ). Today we are sellers.

As you can see below, Mr. Market has been pricing in NIM pain in the US financials.

Retail stocks are now in a correction, off 11.7% from their April highs vs only -3.1% for the S&P 500. The real warning sign is that in retail we’re seeing leadership in defensive names (recession proof stocks), while at the same time strong US Treasury demand.

Last year on CNBC, I was lectured by other guests that lower oil prices would be good for the U.S. consumer. The problem, they ignored the multiplier effect of all those high paying jobs lost in the oil and mining space. Association of American Railroads weekly rail traffic report for week ending May 7th: 492.9K carloads and intermodal units, -10.6% y/y.

How about that rock solid US consumer that was going to spend frivolously all these windfall dollars from lower gasoline prices. At least they don’t spend it at Disney, Aropostale, Fossil or Macy’s and JC Penney.

Divergence between the S&P 500 and the XRT Retail ETF

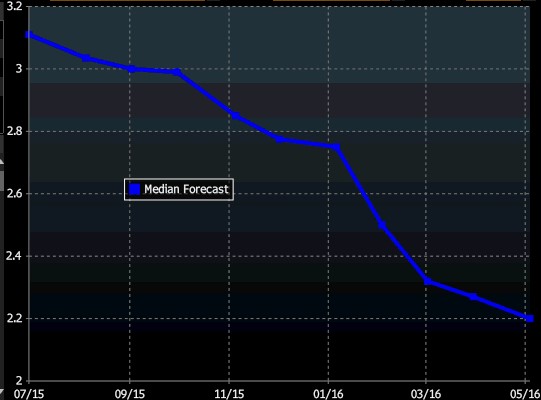

Wall St. and the U.S. 10 Year, Pure Comedy

Meanwhile, the gang that cant shoot straight has had another tough year trying to forecast the U.S. 10 year Treasury yield. They’ve gone from 3.15% to 2.20%,. The only problem is the ten year closed Friday at 1.70%.

“Beware of the banker who says he’s not in need of your capital, for those very spoken words are a loud cry for help.”

Bernard Baruch

Join our Larry McDonald on CNBC’s Fast Money, Wednesday May 18, at 5pm.

Our 21 Lehman Systemic Risk Indicators are Screaming Sell

In the face of bold threats of destruction from the PBOC (People’s Bank Of China), some brave souls are paying up for CNH vol (Currency Volatility) today (see the chart below), betting on further yuan depreciation.

The Fed did China a huge favor in shooting the March and June rate hikes between the eyes, thus talking the dollar lower (98.5 to 91.9 from March 2 to May 2). But the dollar’s surge since has the PBOC flustered. Their punch back to the Fed for not further containing the greenback will be found in some stressful financial conditions.

Over the last year, surges in CNH vol have been followed by a plunging S&P 500.

One important component of our 21 systemic risk indicators is found in the VIX 2 month vs 8 month spread. Deep backwardation (front month trading rich to the outer months) comes with strong equity buy signals, as we noted in our Bear Traps report on February 9th. Rich contango (front month trading cheap to the outer months) comes as a sell signal. The recent high in the S&P coincided with the steepest VIX futures curve in the last year. Think of a car moving from 30 to 90mph, the speed of the curves flattening process, the stronger the equity sell signal.

As most know, China lost $800B last year in capital outflows. As the dollar weakened in March, capital outflows in China took a well needed breather. The Chinese yuan is pegged to the US dollar, thus a strong US currency makes China’s goods sold around the world much more expensive. After the dollar’s pull back (March – April), China posted their two best export months in the last year.

If you’re a billionaire in China and you know your currency is dramatically over-valued, you’re going to do everything you can to get cash out of the country and into dollars. This explains the record amount of US acquisitions by companies in China, it’s the great cash run out of the country.

In January, the Fed wanted to hike rates four times this year, they misjudged the negative impact a strong dollar has on the global economy. Hence, after they woke up and brought their rate hike forecast to 2, global markets stabilized.

Here we sit, halfway through the month of May and the Federal Reserve has promised to hike rates two more times in the next 6 months.

Much Smaller Part of the Global Economy

Global GDP Outside the USA: $61T

USA GDP: $18T

There are only two ways out for China, a substantial currency or credit devaluation. We think they’ll choose the former. With NPLs (non-performing loans) at 17% of outstanding credit vs what the PBOC tells us (less than 2%), it’s a mess. Bad loans are 8x to 10x than the bogus official numbers lead us to believe. Ultimately, we believe there are likely $700B to $1T of losses.

Transports are Flashing Sell Signals

Classic market top price action is found in the divergence between the Dow Jones Industrial Average (heading north) and the Dow Jones Transports (heading south).

In the post Lehman era, central banks either huddled together or off on their own, have carried a heavy policy cross with the goal of giving their underlying governments time to heal from the financial crisis.

It’s a game of central bankers using monetary policy in an effort to take time off the clock. Their ultimate hope? A prayer that the burned out engines of fiscal policy would finally ignite to save the day. That day has never come, so far central banks have only become the great enabler.

Today, global leverage is found in chains wrapped around the feet of former powerhouse economies. Total debt (corporate, household, government), laying in advanced economies is now 259% of GDP vs 175% in emerging markets, and 246% in the US and China.

The year 2016 will mark a turning point. The serpent inside global markets has been contained by central bankers, but this beast is about to have his revenge. We witnessed opening acts last September and again in January, but the show has just begun.

Over the last 10 years central banks have thrown a lot of firepower, trying to contain Mr. Market’s natural laws. The experimental drugs are wearing off, the patient now needs stronger and more intense doses to achieve the same desired effect.

This fight is so long in the tooth, we must prepare for what’s next. When common sense becomes harder and harder to find, you’re far closer to the end than the beginning. The last act will not end in laughs, there won’t be a dry seat left in the house.

The key to Yellen’s deceptive banter yesterday was found in just two words, “appreciably lower.” This overly dovish tone leads us down a few different paths for equities.

1. US equities drift higher with more central bank accommodation

2. The market realizes the US economy (and earnings) aren’t as strong as investors are hoping, and stocks pull back.

We think it’s the latter.

One year chart of the SPY Index – In our opinion, the upside is limited to a few percent vs the downside of 20% over the next few months.

Over the last two years, as the VIX curve has gone into deep contango (as represented by the front month and the 8th month – White line well below the Green line), this has been a sell signal for US equities.

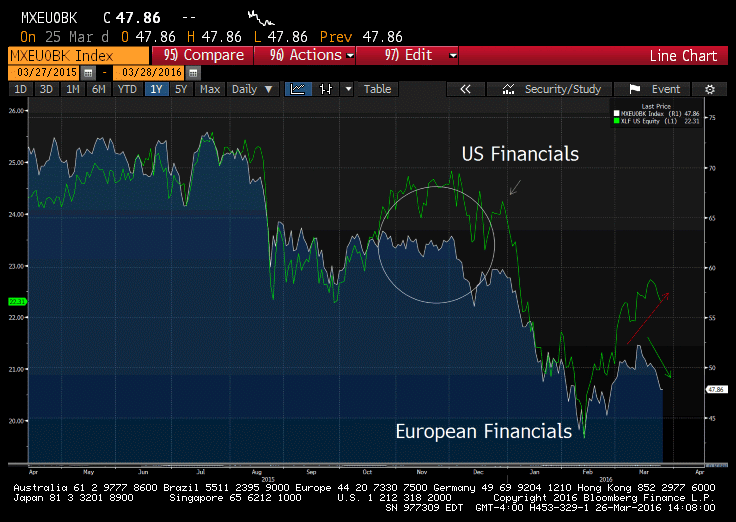

European financials started to rollover last fall, before US banks followed suit. We are seeing the same pattern today (chart below). Strong sell signals in the Eurozone financials have us on alert, our Lehman systemic risk indicators are on the rise.

1 Year Chart of US Financials vs European Financials