Join our Larry McDonald on CNBC’s Trading Nation, Wednesday at 2pm.

“I was born at night, just NOT last night.”

George Carlin

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereWhere are bond yields going with debt on the rise in China? Click here (above) for our latest report.

Sunday Night, January 8, 2017

- China Weakens Yuan Fixing by 0.9%, Most Since June 2016

- PBOC set yuan fixing at 6.9262 vs USD, 0.87% weaker than Friday

- China’s currency is 15% overvalued in our view

- Damage Control: The People’s Bank of China will inject 10b yuan into the banking system using 7-day reverse repurchase agreements today

- The central bank will also inject 100b yuan using 28-day reverse repos

Breaking News: China’s foreign currency holdings remained above $3 trillion in December even as the yuan capped its steepest annual decline in more than two decades.

Better fiction than Harry Potter, China’s foreign exchange reserves fell $41.08 billion to $3.01 trillion, the People’s Bank of China (PBOC) said in a statement Saturday. That matched a $3.01 trillion estimate in a Bloomberg survey of economists.

The PBOC is running out of options with FX reserves getting quite low. Of course, as a headline number their FX reserves are high, but as we have stressed to clients, as percentage of the money supply (M2) they are quite low.

“This week, we do not believe the PBOC will let reserves drop below the psychologically important level of $3 trillion.”

The Bear Traps Report, January 4, 2017

In an effort to prevent a global panic within the investment community, China is using emergency measures to keep its foreign-currency stockpile from slipping too far below the key $3 trillion.

We believe as even more confidence is lost, further declines in the yuan will follow. Policy makers in China have recently rolled out extra requirements for citizens converting yuan into other currencies after the annual $50,000 quota for individuals reset Jan. 1, more emergency currency controls to come.

China wants the upside of capitalism without the downside of dealing with a loss of investor confidence, but you can’t be a little bit pregnant.

The Hemorrhage Continues

Capital is running, NOT walking out of China. As was the case in Q1 2016, China is the big story to watch. As the Yuan gets closer to 7 against the U.S. Dollar, we believe the Chinese are at an inflection point. The PBOC (Peoples Bank of China) tried to get the currency under control by aggressively selling ($200B) U.S. Treasuries in the back half of 2016. However, this led yields higher and made the Dollar stronger and ended up hurting China’s FX position. In our view, there’s over $1T of losses in China’s highly levered, Lehman like black box, yes their banking system. Bottom line: $3T of currency reserves doesn’t go as far as it used to with a Swiss cheese banking system bleeding cash.

China’s recent policy of opening its markets to foreigners is expected to continue this year, but there are questions about how meaningful the change will be amid a clampdown on money leaving the country.

Damage

As China loosened controls on its interbank bond market and relaxed rules for offshore investors trading stocks. It also saw nearly $800B head overseas in the first 11 months of last year, according to Bloomberg estimates. Investors sought safety in foreign assets pushing the yuan down 6.6% against the dollar in 2016, the most since 1994.

2006-2016 China Leverage

Credit Growth: 1175%

GDP Growth: 470%

The Bear Traps Report data

Get our full report here:

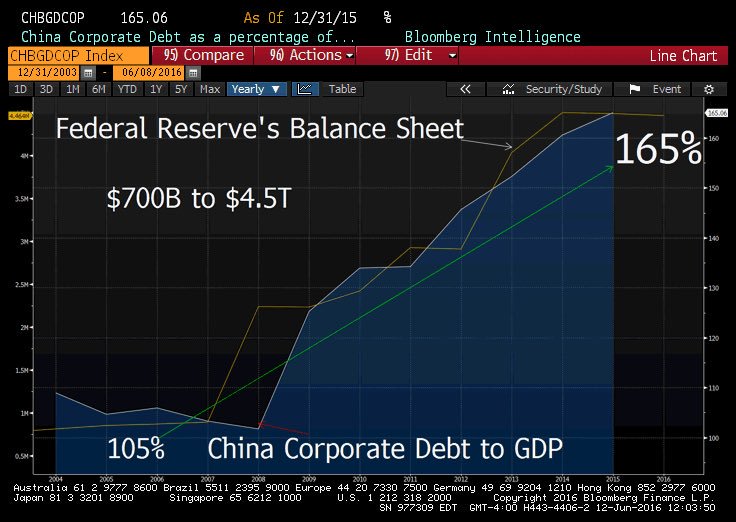

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereChina Corporate Debt to GDP vs Federal Reserve’s Balance Sheet

2016: 165% vs $4.5T

2008: 105% vs $700b

Bloomberg, the Bear Traps Report

The Fed’s been the Great Enabler

Has the Fed’s easy money gravy train found in zero interest rate policy been China’s great enabler? You bet it has.

China Debt Issuers

% with Negative Credit Rating Outlook

2016: 70%

2015: 29%

2014: 15%

2013: 14%

Moody’s

The Great Shell Game

Again, Chinese devaluation risk will be back at the forefront in 2017.

Another important theme; Chinese capital flows are having a

massive impact on asset classes around the world. As cash pours out of the country the spread between the off shore yuan (CNH) and on shore (CNY) widens. In an effort to control the beast in the market, China from time to time steps in and strengthens their currency, as you can see above they made a substantial “panic” move last week in an effort to stop the bleeding.

Where are bond yields going with debt on the rise? Click here for our latest report.