Join our Larry McDonald on CNBC’s Trading Nation, this Wednesday at 2:20pm

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereBlog Updated 3/14/17 at 7:50am

Breaking: OPEC UPS NON-OPEC SUPPLY FORECAST BY 160,000 B/D THIS YEAR AS US SHALE RETURNS

Breaking: *SAUDIS TELL OPEC THEY PUMPED 10 MILLION BARRELS A DAY IN FEBRUARY

The Saudi’s told OPEC they “increased” output in February? Yes, back above 10 million barrels a day. This took away about a third of the cuts it made the previous month.

The Kingdom had promised to curb supplies and did so more than it needed in January. In a reversal, the Saudi’s have shown leadership to re-balance world markets, BUT NOW THEY INCREASED production by 264k barrels a day to 10.011 million a day, according to a monthly report from OPEC on Tuesday.

OPEC Monthly Report: raises 2017 global oil demand growth from 1.19M bpd to 1.26M bpd.

Boosts non-OPEC supply growth (shale) forecast from 240K bpd to 400K bpd.

They Did it Again

Excerpt from Our Bear Traps Report from March 7, 2017

We think oil is capped and the balance of risk to price is to the downside. While OPEC is cutting production, shale is back and stronger than ever. Oil per rigs are up and employment necessary for rig operation is down, this all fosters a positive output environment. What has driven this rapid supply response is the insane debt levels these frackers have. To pay the coupons they have to hit the supply hard, and they have in recent months. Now, with oil stuck in this range, we feel the next break is lower. This will be very consequential for markets, Fed policy and the global economy.

Oil Positioning is at Record Longs, Too Many Bulls

Despite U.S. production roaring back, the market is still record long oil contracts. With positioning so one sided in crude oil, it seems that the relative upside is capped. The market has a few catalysts which could drive prices higher as global demand is improving at a time when OPEC is actually cutting their output levels. This does present a positive backdrop for prices but the question is how sustainable is it. Can the Saudi’s continue to shoulder the majority of OPEC cuts with global demand picking up, watching Iraq’s production shift in the coming months will be telling. Iraq is one of the largest OPEC producers and also has constantly been hesitant about production cuts; if they give way, it would be a trickle down to Libya, Kuwait and other GCC (Gulf Coast Countries) members. This is part of the Saudi peg, but if there is a catalyst for this positioning to give way and push the curve out, oil could slide hard.

Despite U.S. production roaring back, the market is still record long oil contracts. With positioning so one sided in crude oil, it seems that the relative upside is capped. The market has a few catalysts which could drive prices higher as global demand is improving at a time when OPEC is actually cutting their output levels. This does present a positive backdrop for prices but the question is how sustainable is it. Can the Saudi’s continue to shoulder the majority of OPEC cuts with global demand picking up, watching Iraq’s production shift in the coming months will be telling. Iraq is one of the largest OPEC producers and also has constantly been hesitant about production cuts; if they give way, it would be a trickle down to Libya, Kuwait and other GCC (Gulf Coast Countries) members. This is part of the Saudi peg, but if there is a catalyst for this positioning to give way and push the curve out, oil could slide hard.

High Debt Load = Lower Oil Prices

The price of eight years of central bank zero interest rate policy is found in oil’s flat line since June. The bottom line net result of an easy money gravy train is playing out in commodity market supply distortions. Without colossal leverage and unprecedented (2010-15) capex ($500B per Wood Mackenzie) in the oil patch, supply would NEVER in a million years come back this violently in U.S. shale. Now, the Trump administration is talking up $50T of untapped U.S. reserves to help fund the infrastructure rival. We

expect deregulation and a contained EPA to only had more juice into U.S. oil production, the supply – demand imbalance.

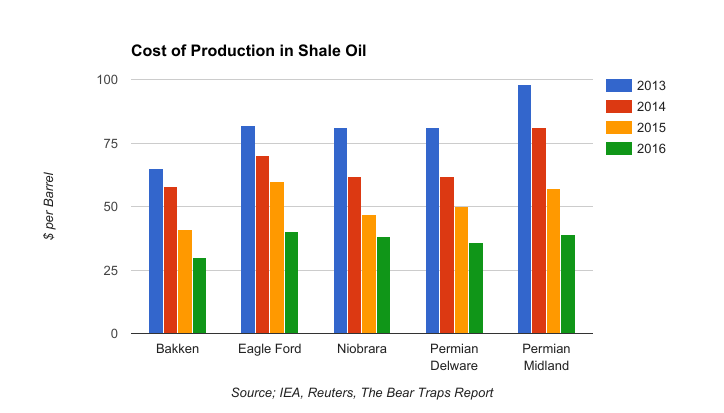

Shale Pain for Crude

Another key element for the shale players is that oil production costs have come way down in recent years. Breakevens for all of the big shale locations are well below current prices. As we have seen in recent earnings reports, margins for production have actually increased dramatically in recent months as breakevens are now near $35-40 a barrel on average. With lower breakevens and heavy debts to pay, shale production is not going anywhere if oil prices remain in range. That is problem for prices in the medium term.

While Speculators are Long, Producers are Short

While speculators are jumping over each other trying to get long oil contracts, the guys who actually produce the commodity are heavily short it. Well it is obvious that shale producers have used this OPEC led rally to lock in prices, it does say that they are not very confident prices can rise meaningfully from current levels. This has contributed to the backwardation beyond the 3-month contract in the curve. There are some cases of levered players that need to hedge prices to lock in financing, but to see so many producers short makes us think they are skeptical of how much higher prices can go.