Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Institutional investors can join our live chat on Bloomberg, a groundbreaking venue, just email tatiana@thebeartrapsreport.com – Thank you. LGM

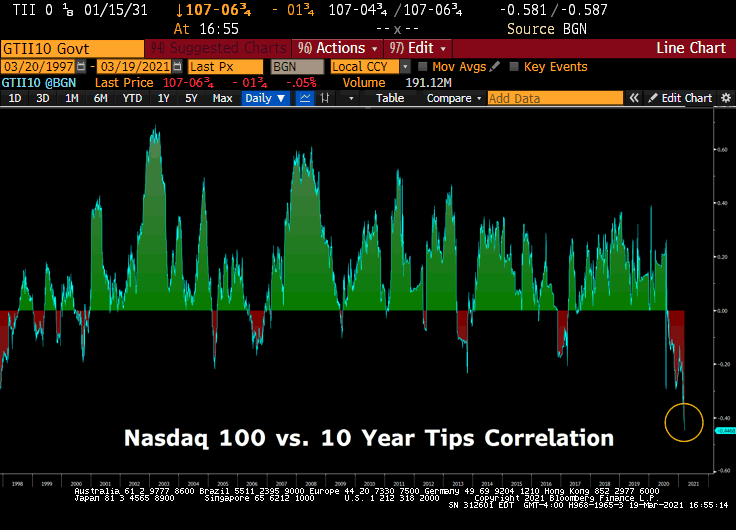

The bond market is blowing up, what are we going to do about it?

Why should you care? Bonds are Driving Stock Prices

A colossal portion of “growth” stocks have their true worth embedded in the “net present value” of FUTURE cash flows. Thus, as bond yields and inflation expectations rise – tech stocks are worth a lot less.

A colossal portion of “growth” stocks have their true worth embedded in the “net present value” of FUTURE cash flows. Thus, as bond yields and inflation expectations rise – tech stocks are worth a lot less.

Stock prices have been HIGHLY driven by bond prices in recent weeks, we MUST pay attention to the fixed income markets.

We noted yesterday in the Bear Traps Report – “The question is, does this latest Fed move pave the way for no more SLR exemptions? Yes.”

Supplementary Leverage Ratio (SLR)

What is the SLR? The SLR is a measure of capital adequacy, in the years since Lehman Brothers, this is on everyone’s mind. Essentially, it measures in percentage terms a bank’s ability to take losses on its assets. The formula is SLR = (tier 1 capital)/(total leverage exposure).

What happened this week? It’s NOT Fed Chair Powell blinking under pressure from Senator Elizabeth Warren. This is a negotiated deal.

Pop quiz: What is the legal mechanism under which the Fed is independent? Its shares are owned by the member banks. Yep. That’s right. JP Morgan, Citibank, Bank of America, Wells Fargo, et al literally own the Fed. Anyone who thinks the RRP cap raise and the subsequent non-extension of the SLR exemption is wholly unrelated phenomena don’t know half of it. This was heavily negotiated. The Central Bank, believe it or not, talks to Jamie (money center banks), daily.

So it went down like this starting two weeks ago:

Fed on call to Jamie Dimon, CEO of JP Morgan: So folks, what’s cookin’?

Jamie: Eh. Not much. Kind of annoyed by this whole SLR thing.

Fed: Oh that Basel III thing that says Jamie has to raise capital against cash? That is just so stupid.

Jamie: No kidding. This is why we really appreciate having that exemption.

Fed: Yeah well, as you know, that was because of a pandemic. If Covid goes away, the exemption goes away. You all know this.

Jamie: Oh! For sure for sure but…

Fed: But you’re about to get tons of cash deposits from Treasury from fiscal stimulus. What’s the big deal? That money will all be spent soon enough. The problem will go away quickly.

Jamie: True, but before the money is spent we’ll be in non-compliance (new deposits are liabilities for banks). Can’t you just extend it?

Fed: Nah. Not in the mood. But just avail yourself of our RRP facility. Your cash will become reverse repos and you don’t have to raise capital.

Jamie: We thought of that.

Fed: I’m sure you did. (after a strained silence) But…?

Jamie: But the $30 billion cap just isn’t working for us.

Fed: Ahhh! I knew you wanted something!

Jamie: We always do!

(General laughter)

Jamie: Well, how about no cap?

Fed: Forget it! That doesn’t look right. Besides…

Jamie: Besides you need to keep your chokehold on our necks in case we get out of line on something else.

Fed: Precisely!

(General laughter)

Fed: So how much you think you need?

Jamie: Worst case $100 billion.

Fed: $100 billion. Are you crazy? Way too much. Do you think money grows on trees?

Jamie: Yes.

Fed: Oh yeah, you’re right about that.

(General laughter)

Fed: Gimme a number less than a hundo. That extra digit gives me the willies.

Jamie: $90 billion?

Fed: Too close. Make it $80 billion and we’ll throw in some language that if that’s not enough we can always raise the cap more.

Jamie: Done.

Federal Reserve Bank of New York to conduct overnight reverse repurchase agreement (ON RRP) operations with a per- counterparty limit of $80 billion per day, effective March 18, 2021.

Fed: Not quite.

Jamie: Oh God what now?

Fed: Lighten up on your treasury book.

Jamie: Say what? We thought treasuries were risk-free!

(General laughter)

Fed: Look. We don’t want to turn around and raise the RRP cap two weeks after the SLR exemption expires. That’s stupid.

Jamie: But…

Fed: But nothing. Reduce your treasury holdings. We’ll tell everyone on the planet we’re not concerned that rates are backing up, that we want inflation and full employment blah blah blah. You just do what you got to do and we’ll put a nice face on it.

Jamie: Ok. Fair.

Fed: And one last thing…

Jamie: One of you guys has to raise capital now.

Jamie: C’mon! That’s not fair! We already have to deal with the SLR exemption expiring and doing all these RRPs and selling down our treasury book and now we have to raise capital and lower our shareholders’ returns? The whole point of this convo is to avoid just that!

Fed: Brilliant, eh?( Jamie grumbling amongst themselves)

Fed: Calm down calm down. It doesn’t have to be all of you. Just one of you. You know, as a signal that you are willing and able to raise capital if need be.

Jamie: So if one of us raises capital preemptively, that signals to the markets that all of can…

Fed: Exactly. So Jamie…

Jamie Dimon: Oh no…

Fed: About this share buyback of yours that actually reduces capital…

Jamie Dimon: Oh no…

Fed: Not a good look just before the SLR exemption expires.

Jamie: Ok. I’ll take a bullet for the team I guess. Kinda sucks though.

Fed: You’ll live. Besides, once all the excess deposits are spent, you can use that cash to buy your stock.

Jamie: Oh yeah! I feel better already.

(General laughter)

Fed: $4 billion.

Jamie: $2 billion.

Fed: $3 billion and we are done with everything.

(Pause)

Jamie: Ok

Jamie: Sounds good to us!

Fed: Great. So the SLR exemption expires, the RRP cap is raised to $80 billion with flex above, you sell your treasuries and we talk nice, JPM raises $3 billion in prefs and everybody’s happy. Right?

Jamie: Right, the World is Saved for another day.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here