“Our indicators tell us, we’re very close to a Lehman-like drawdown,” argues Larry McDonald, a former strategist at Société Générale who now runs The Bear Traps report.

Financial Times, February 20, 2020

*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereFollow the Money

So far in 2020, investment-grade bond issuance is approaching $1.3 trillion, that’s more than double the $595 billion IG debt issuance pace at this time last year. In the history of U.S. capital markets, four of the top six best IG new supply months are found in 2020, with April being the mother-load, up close to $300 billion.

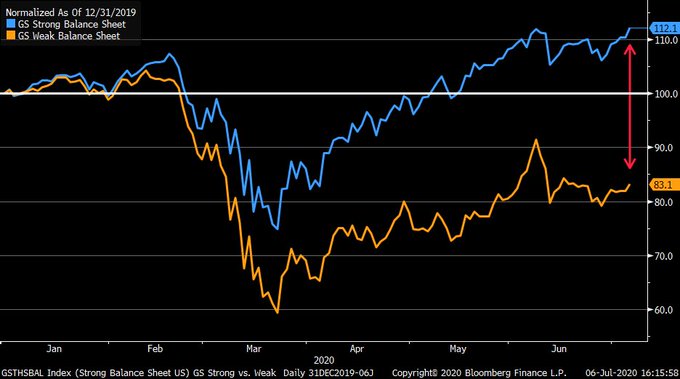

Credit Risk, Who’s Funded?

As you can see above, credit risk is driving equity prices. Well funded sectors (blue Goldman strong balance sheet) have performed well since the market highs of June 10th, while under-funded balance sheets are falling behind. Likewise, the S&P Equal Weight equity index is down almost 10% over the last month. Everyone knows – a few, well-funded companies inside the S&P 500 are running the show with hundreds of other companies left behind.

As you can see above, credit risk is driving equity prices. Well funded sectors (blue Goldman strong balance sheet) have performed well since the market highs of June 10th, while under-funded balance sheets are falling behind. Likewise, the S&P Equal Weight equity index is down almost 10% over the last month. Everyone knows – a few, well-funded companies inside the S&P 500 are running the show with hundreds of other companies left behind.

The Eye-Opener

Here’s an eye-opener. Below we take a look at the BB and higher credit quality new issues – year to date by sector. That’s right, YTD debt sales in 2020 vs the FULL YEAR 2019, the data is telling:

1) Financial $427 billion vs $546 billion (increase in deposits, record money market fund inflows, equal lowered funding needs);

2) Consumer non-cyclical $175 billion vs $228 billion (cash flows steady, COVID19 favors staples)

3) Consumer cyclical $153 billion vs $108 billion (levering up, get it while you can);

4) Communication $117 billion vs $87 billion (deals, 5G expansion funded for now);

5) Energy $116 billion vs $133 billion (companies disappearing, capex (drilling) imploding vs. 2017 levels);

6) Industrials $113 billion vs $98 billion (again, get the money while you can);

7) Technology close to $110 billion vs $68 billion (explosive inequality, monopolistic advantages all funded by the Fed, continue the debt build);

8) Utilities $75 billion vs $100 billion;

9) Basic Materials $36 billion vs $48 billion (There are 10,000 fewer holes (metals and mining) on earth being dug today than a decade ago. From a CAPEX overdose to starvation, NO supply!

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereThe Bloomberg Financial Conditions Index is now at the mid-point of the February 2020 range, yet IG issuance clearly is set for issuance records unforeseen back then. A one-week all-time issuance high was set in April at $110 billion.

The cause is well known: a near-infinite Central Bank bid allows IG companies to raise as much money as they can dream of despite poor economic conditions. Meanwhile, after multiple fiscal stimulus rounds, the White House is pushing for another $1 trillion before the August recess.

Debt markets may have found an equilibrium point. Treasury just had a record 3-year issuance of $46 billion, up-sized by $2 billion, and a full $8 billion above the norm that has held since December 2018. At 0.19%, it is the richest on record. The cover was 2.44, lower than last month’s 2.55, and a touch below the average 2.45 of recent times. So we have now the first sign of some investors on the sidelines.

Second-quarter earnings are soon, with S&P earnings forecasted down 30%. Earnings may not be quite that bad, but cash flow to interest ratios are set to deteriorate markedly. It will be interesting to see if this quarter’s earnings season “puts a lid on it.”

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here