Join our Larry McDonald on CNBC’s Trading Nation, Wednesday at 3:05pm ET

Pick up our latest note here:

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click hereIn cooperation with ACG Analytics in Washington: Impact Areas, Oil and European Elections

Tillerson Heading to Moscow on the 12th, for Now

Six months ago, if we told you Donald Trump will be elected President, and the first quarter of his administration would see calmest stock market ever? Would you believe us?

Household and Small Business Sentiment has Surged the Trump Election:

1. University of Michigan’s consumer sentiment index reached a 13-year high.

2. Last week the Conference Board’s index of consumer confidence rose to its highest level in 16 years.

3. The NFIB’s small business optimism index is at a 12-year high after having recorded its largest-ever two-month increase in November and December.

If we look at Q1 U.S. stock market volatility found in the S&P 500, the average VIX level was down at 11.74 That’s the lowest Q1 level on record, smallest quarterly average since Q4 2006. Of course, this all changed in April.

U.S. Missile Strike: Syria Implications

If Assad falls, Syria will look like Libya. ISIS moves in for power grab. Proxy groups fight for power amongst themselves and v ISIS. Meanwhile the US consolidates in neighboring Iraq. In Syria, Russia will either pull or commit, US will likely do the opposite (Russia also likely knew about this as the U.S. warned them to leave, to avoid casualties, they told Assad so his air assets scrambled to avoid the strike. Bottom line: Assad has not fallen yet).

VIX Futures Curve Flattening, Speaks to Geopolitical Risk Surge

The 1 Month v 3 Month VIX futures curve, flattest since (Brexit / Trump election). If hedge funds are paying up for near term protection, typically comes in front of some pain, lower equities. Our model measures the speed of the flattening, it’s accelerating at an alarming rate. Cash is pouring into the front end, meaning market participants want insurance against a possible near term drawdown in stocks. Bottom line: the cost of the April contract is nearly the same for three much insurance on the market. Typically, as in most of this year – the front end is far cheaper than outer months, NOT today.

Oil Futures Spike on U.S. Strike

Lets be Clear, Syria’s Oil Output is Less than 0.65% of Global Production

Syrian production is not the entire story here. We think oil implications are meaningful, it is no secret Turkey would like close oil access. This could give Russia a mandate to take ISIS’ oil fields in the south and then deal with Turkey. Assad regime is also ISIS’s biggest customer in the blackmarket oil trade which is protected by Russian air assets, they still hold the oil fields, Implications here point to the White House. Trump must decide to commit in the region if Russia doesn’t or see where the dust settles and risk the power vacuum. Shifts in refugee flow could impact Europe – depending on Turkey’s reaction, it’s likely U.S. military action in the region will exacerbate anti-Islam nationalist sentiments in Europe as ISIS fragments move north. Bottom line, the migration risk from Syria into Turkey and on to Europe is higher now than ever. This gives populist candidates like Le Pen in France another argument for more aggressive border controls – the influx of refugees into Europe has already created collateral political stress.

Syrian production is not the entire story here. We think oil implications are meaningful, it is no secret Turkey would like close oil access. This could give Russia a mandate to take ISIS’ oil fields in the south and then deal with Turkey. Assad regime is also ISIS’s biggest customer in the blackmarket oil trade which is protected by Russian air assets, they still hold the oil fields, Implications here point to the White House. Trump must decide to commit in the region if Russia doesn’t or see where the dust settles and risk the power vacuum. Shifts in refugee flow could impact Europe – depending on Turkey’s reaction, it’s likely U.S. military action in the region will exacerbate anti-Islam nationalist sentiments in Europe as ISIS fragments move north. Bottom line, the migration risk from Syria into Turkey and on to Europe is higher now than ever. This gives populist candidates like Le Pen in France another argument for more aggressive border controls – the influx of refugees into Europe has already created collateral political stress.

Where’s the Trade?

Pick up our latest note here:

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

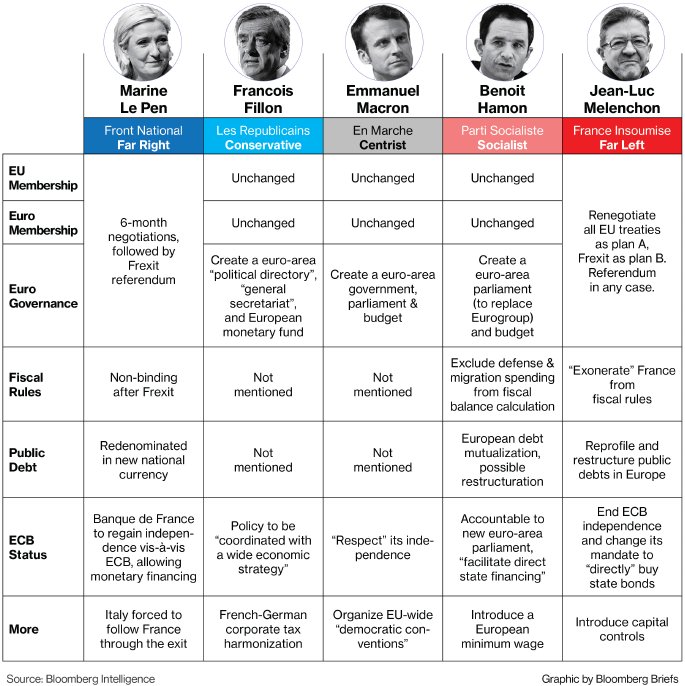

The latest move comes amid signs traders are starting to put election hedges back on as they enter the month of the election, even as polls continue to show euro-skeptic Marine Le Pen will lose in May’s second round. Per Bloomberg, French candidates are due to hold their second debate later today, with the first round of voting scheduled for April 23.

The latest move comes amid signs traders are starting to put election hedges back on as they enter the month of the election, even as polls continue to show euro-skeptic Marine Le Pen will lose in May’s second round. Per Bloomberg, French candidates are due to hold their second debate later today, with the first round of voting scheduled for April 23.

High yield has underperformed investment grade bonds by 25bps over the last 30 days.

High yield has underperformed investment grade bonds by 25bps over the last 30 days.